PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063593

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063593

Passover Humidifiers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

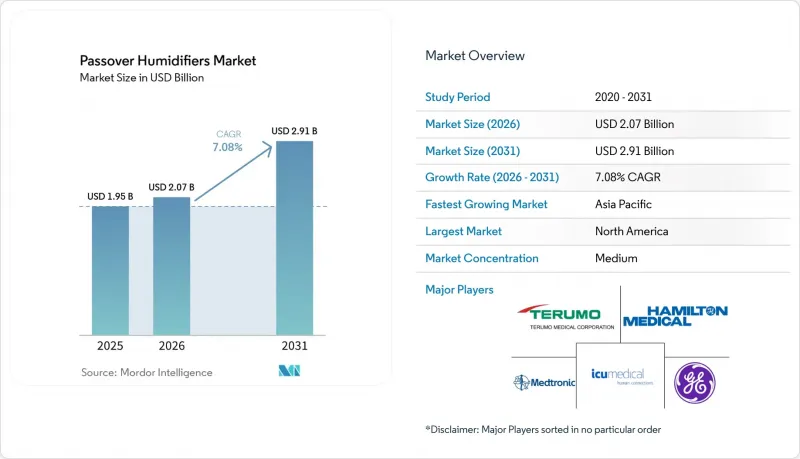

According to Mordor Intelligence, the passover humidifiers market size was valued at USD 1.95 billion in 2025 and is estimated to grow from USD 2.07 billion in 2026 to reach USD 2.91 billion by 2031, at a CAGR of 7.08% during the forecast period (2026-2031).

This report is Segmented by Product Type (Dry Disposable, Pre-Filled Disposable, Reusable), Application (CPAP Therapy, Mechanical Ventilation, High-Flow Nasal Cannula & Oxygen Therapy), End-User (Hospitals & Clinics, Homecare Settings, Sleep Centres & Others), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Passover Humidifiers Market Trends and Insights

Rising Prevalence of Sleep Apnea & CPAP Adoption

Nearly 936 million adults worldwide live with obstructive sleep apnea, and U.S. diagnoses are forecast to reach 77 million by 2050, expanding the patient pool that relies on CPAP therapy and add-on humidifiers. Adherence, however, falters when nasal dryness emerges; studies show 30-60% of patients quit within a year, but smart pass-through humidification raises five-year adherence to as high as 87%. CMS's National Coverage Determination 240.4 enforces a 12-week trial with documented compliance, nudging suppliers toward disposable, pre-filled chambers that lower misuse risk. Sleep-test reimbursement is likewise shifting: CPT 95800 is under valuation scrutiny because disposable sensors are replacing reusable gear, which could further tilt procurement toward single-use consumables.

Growing Home Healthcare & Tele-Medicine Penetration

Home-health orders already account for 55% of durable respiratory equipment, and U.S. home-health aide employment is projected to grow 22% through 2034. New remote-patient-monitoring (RPM) codes 99XX4 and 99XX5 proposed for 2026 will reimburse device data capture and clinical interactions, complementing existing CPT 99453, 99454, and 99457. The MonitAir trial reported an 18-percentage-point reduction in CPAP discontinuation when real-time humidity alerts were deployed. Yet pandemic-era telehealth flexibilities may expire, restricting virtual care to rural zones and dampening RPM uptake in urban markets. Suppliers are therefore bundling humidifier analytics with adherence dashboards to safeguard reimbursement even if broader telehealth rules tighten.

Stringent Device Approval & Post-Market Surveillance Requirements

Passover humidifiers fall under FDA Class II (21 CFR 868.5450) and demand 510(k) clearance, ISO 13485 quality systems, IEC 60601 electrical safety, and a periodic safety report compliance package that can add USD 0.5-1 million and 12-18 months to launch timelines. CMS's RAC Topic 0066 audits medical necessity for PAP devices, and an improper-payment rate of 12.5%-71.2% linked to documentation gaps-forces suppliers to invest in EHR integrations. Although February 2024 DME MAC guidance loosened wording on orders ("CPAP Mask" acceptable), the underlying evidence burden persists and deters smaller entrants.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advances in Disposable Water-Chamber Materials

- Aging Population with Higher Respiratory Comorbidities

- High Total Cost of Advanced CPAP Systems in Low-Income Regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dry disposable units held 43.81% of passover humidifiers market share in 2025, anchored in ICU and sleep-center protocols that demand daily water changes. The passover humidifiers market size for dry disposable products is forecast to grow at a steady clip, albeit slower than premium alternatives. Reusable designs continue to serve budget-sensitive home users, but infection alerts from FDA against ozone and UV cleaners have tempered enthusiasm.

Pre-filled disposable chambers, expanding at 9.09% CAGR, leverage sterile water fills to remove patient-side maintenance and slash Pseudomonas contamination risk documented in January 2025 case reports. Fisher & Paykel's F&P my820 couples adaptive humidity with cloud titration, evidencing how IoT features accelerate uptake. As advanced polymers narrow cost gaps, pre-filled units are poised to contribute the majority of incremental passover humidifiers market revenue by 2031.

Geography Analysis

North America preserved 39.83% of passover humidifiers market revenue in 2025, buoyed by Medicare's 13-month capped rental model and a documented OSA population expected to more than double by 2050. The region faces a 12.5% improper-payment rate for CPAP claims, which cost USD 146.1 million in 2024 and spurred investments in automated compliance tracking. Tariff-induced reshoring is increasing lead times for subcomponents, yet USMCA incentives are attracting final assembly to Mexico, sidestepping a universal 10% tariff on non-US goods.

Asia-Pacific is the fastest-growing arena at 10.17% CAGR. In India, a basic CPAP retails for INR 18,000-22,000 (USD 215-263), whereas the CGHS cap leaves a yawning reimbursement gap, steering consumers toward low-cost dry disposable chambers. Japan's super-aged society and South Korea's digital-health policies are catalyzing early adoption of IoT-enabled humidifiers. The Philippines trial validating reprocessed bCPAP safety may inspire circular-economy supply chains if regulators set clear reuse standards.

Europe ranks second in global share, anchored by NHS reimbursement, German DRGs, and France's Securite Sociale. EU MDR tightens post-market surveillance, inflating compliance overheads that favor established players. Fisher & Paykel's pan-European launch of the F&P my820 in August 2024 showcases the region's appetite for premium, connected humidifiers. The Middle East & Africa and South America remain nascent, yet affluent urban pockets in the GCC and Brazil are showing uptake for high-end pre-filled designs.

- Apex Medical

- Armstrong Medical

- BMC Medical

- Breas Medical

- Condair Group

- Drive DeVilbiss Healthcare

- Dragerwerk

- Fisher & Paykel Healthcare

- Flexicare

- GE Healthcare

- Hamilton Medical

- ICU Medical

- Intersurgical

- Medtronic

- Micomme Medical

- Philips Respironics

- Resmed

- Teleflex

- Vapotherm

- Vyaire Medical

- Terumo

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Sleep Apnea & CPAP Adoption

- 4.2.2 Growing Home Healthcare & Tele-Medicine Penetration

- 4.2.3 Technological Advances in Disposable Water-Chamber Materials

- 4.2.4 Aging Population with Higher Respiratory Comorbidities

- 4.2.5 Smart IoT-Enabled Passover Units Unlocking Value-Based Reimbursement

- 4.2.6 Tariff-Driven Reshoring of Humidifier Manufacturing

- 4.3 Market Restraints

- 4.3.1 Stringent Device Approval & Post-Market Surveillance Requirements

- 4.3.2 High Total Cost of Advanced CPAP Systems in Low-Income Regions

- 4.3.3 Infection Risk & Cleaning Non-Compliance Reducing Patient Uptake

- 4.3.4 Substitution Threat From Fully-Integrated Heated Humidifier CPAPs

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Dry Disposable Passover Humidifiers

- 5.1.2 Pre-filled Disposable Passover Humidifiers

- 5.1.3 Reusable Passover Humidifiers

- 5.2 By Application

- 5.2.1 CPAP Therapy

- 5.2.2 Mechanical Ventilation (ICU & Critical Care)

- 5.2.3 High-Flow Nasal Cannula & Oxygen Therapy

- 5.3 By End-User

- 5.3.1 Hospitals & Clinics

- 5.3.2 Homecare Settings

- 5.3.3 Sleep Centres & Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Apex Medical

- 6.3.2 Armstrong Medical

- 6.3.3 BMC Medical

- 6.3.4 Breas Medical

- 6.3.5 Condair Group

- 6.3.6 Drive DeVilbiss Healthcare

- 6.3.7 Dragerwerk

- 6.3.8 Fisher & Paykel Healthcare

- 6.3.9 Flexicare

- 6.3.10 GE Healthcare

- 6.3.11 Hamilton Medical

- 6.3.12 ICU Medical (Smiths Medical)

- 6.3.13 Intersurgical

- 6.3.14 Medtronic

- 6.3.15 Micomme Medical

- 6.3.16 Philips Respironics

- 6.3.17 ResMed

- 6.3.18 Teleflex

- 6.3.19 Vapotherm

- 6.3.20 Vyaire Medical

- 6.3.21 Terumo Medical Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment