PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063595

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063595

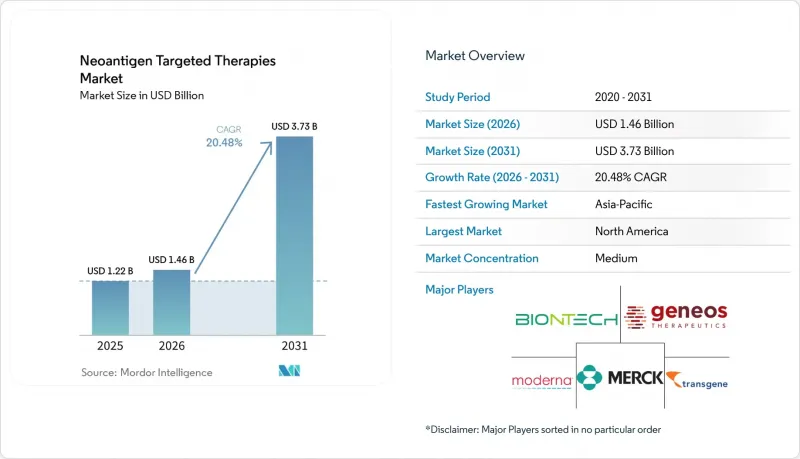

Neoantigen Targeted Therapies - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the neoantigen targeted therapies market size is projected to be USD 1.22 billion in 2025, USD 1.46 billion in 2026, and reach USD 3.73 billion by 2031, growing at a CAGR of 20.48% from 2026 to 2031.

This report is Segmented by Therapy Type (Monotherapy and Combination Therapy), Cancer Indication (Melanoma, Non-Small Cell Lung Cancer, and More), Delivery Platform (mRNA-Based Vaccines, Peptide-Based Vaccines, and More), End User (Academic & Research Institutes, and More), Route of Administration (Intramuscular, Subcutaneous, and More), and Geography. The Market and Forecasted in Terms of Value (USD).

Global Neoantigen Targeted Therapies Market Trends and Insights

Rising Global Cancer Incidence

Global cancer incidence continues to grow, with Asia bearing a majority of cases and a large share of mortality, which elevates the urgency for new modalities that deliver lasting control. Lung, breast, and colorectal cancers accounted for the largest portions of new diagnoses in 2022, and lung and liver cancers have remained leading contributors to cancer mortality, which continues to pull demand toward new adjuvant and maintenance options. Low-dose CT programs are increasing early-stage detection in eligible populations, which widens the clinical window for adjuvant vaccination that targets minimal residual disease rather than bulky tumors. Tumors with high mutational burdens like melanoma and smoking-related NSCLC offer richer pools of actionable neoantigens and remain focal points for first-wave commercialization. Pediatric cancers and low-mutational-burden sarcomas yield fewer targets, so current investment is concentrated in adult epithelial malignancies where target density and immune visibility support durable T-cell responses.

Advances in High-Throughput Sequencing and Bioinformatics

Validation of HLA-peptide binding predictions is improving, with modern tools demonstrating high concordance against experimental assays and enabling higher-confidence epitope selection. RNA sequencing corroborates the expression of a large share of predicted neoantigens, which reduces false positives and improves manufacturing utilization by filtering out low-transcript targets. Quality management in bioinformatics has become a regulatory focal point, with U.S. and European guidance pushing for audit trails, version control, and robust validation of machine-learning-based pipelines.

The shift from research-grade pipelines to submission-ready, auditable engines favors sponsors that combine sequencing scale with validated in silico prediction and transcript confirmation to streamline IND dossiers. As platform validation strengthens, the neoantigen targeted therapies market benefits from shortened design-to-clinic cycles and a higher probability that manufactured batches induce the intended immune response. neoantigen-targeted

Manufacturing Complexity, Turnaround Time, and Cost per Patient

Personalized vaccine production requires a series of interdependent steps that include biopsy procurement, tumor-normal sequencing, epitope selection, and GMP manufacturing, which creates schedule pressure and cost sensitivity. Decentralized GMP capacity remains uneven across regions, which slows scale-up and complicates equitable access where courier chains or cold storage infrastructure are limited. Batch-by-batch variability and individualized quality control add layers of testing that do not amortize across large uniform lots, which is unlike conventional vaccine economics. As sponsors streamline bioinformatics selection and standardize release testing, throughput is expected to improve, yet capacity distribution remains a gating factor in near-term regional rollouts. These operational constraints temper near-term adoption curves in the neoantigen targeted therapies market until more hubs, trained personnel, and harmonized protocols expand consistent, timely delivery.

Other drivers and restraints analyzed in the detailed report include:

- Positive Late-Stage Clinical Readouts in Personalized Neoantigen Immunotherapies

- Regulatory and Investor Support for Individualized Oncology

- Clinical and Logistical Challenges Across Biopsy-Sequencing-Manufacturing Chain

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Combination therapy accounted for 58.42% of 2025 revenue as clinicians layered neoantigen vaccines with PD-1 or PD-L1 inhibitors to push beyond the response ceilings of checkpoint monotherapy in many solid tumors. Monotherapy is projected to grow fastest at a 22.56% CAGR through 2031, helped by adjuvant use where limited tumor burden and validated biomarkers favor vaccine-led control. The neoantigen targeted therapies market is using combination backbones to lock in clinical benefit while platforms refine payload design and dosing schedules that aim for long-lived memory responses. In resected melanoma, a personalized mRNA vaccine plus PD-1 therapy reduced the risk of recurrence or death over checkpoint monotherapy, which validated the combination thesis and increased trial activity across other high-risk settings. As datasets accrue, sponsors are evaluating sequence and timing to balance efficacy with immune-related adverse events, with concurrent regimens gaining traction where safety and benefit are consistent.

Growing evidence for durable T-cell memory supports finite-course adjuvant vaccination, while checkpoint agents remain central for metastatic salvage or in tumors where immune suppression is substantial. As payload engineering improves, monotherapy may anchor select adjuvant regimens where biomarker-enriched cohorts show strong recurrence-free survival without added checkpoint toxicity. Sponsors are also optimizing delivery routes to broaden antigen presentation and improve T-cell priming, which can influence the relative role of monotherapy in early-stage disease.

Melanoma contributed 31.57% of 2025 revenue, supported by high tumor mutational burden and strong clinical visibility from advanced adjuvant programs. NSCLC is expected to expand at a 23.61% CAGR to 2031, helped by large incident populations and momentum from immuno-oncology adoption that primes the care pathway for vaccine integration. High TMB biology in melanoma and smoking-related lung cancer provides abundant neoepitopes, which align with multi-epitope payloads designed to prevent antigen escape. In CNS tumors and other immune-cold settings, delivery challenges remain, though adjunctive strategies and improved trafficking have shown survival gains in select programs. Across indications, adjuvant and MRD-guided approaches are central because they engage the immune system when disease is most vulnerable to T-cell-mediated clearance.

Evidence from dendritic cell and tumor lysate vaccines has demonstrated survival improvements in difficult settings like glioblastoma, reinforcing the potential of antigen-directed priming when delivery barriers are addressed. Renal cell carcinoma and other solid tumors with immunogenic features have shown robust antigen-specific responses in early trials, which keeps them in focus for vaccine-led adjuvant innovation. The neoantigen targeted therapies market will likely diversify from melanoma-led revenue toward larger lung and colorectal opportunities as biomarker-defined subgroups become standard in trial designs. As datasets scale, indications with validated ctDNA stratification and well-characterized neoantigen landscapes should be first to embed vaccines into routine care pathways.

Geography Analysis

North America held 35.23% of 2025 revenue due to clinical trial density, concentration of sequencing infrastructure, and established immuno-oncology care pathways that can absorb adjuvant vaccine integration. The region continues to run pivotal studies in melanoma and lung cancer, with leading sponsors reporting extended follow-up and expansion into additional tumor types. The neoantigen targeted therapies market in North America benefits from ecosystem readiness, yet broader access will track with coverage decisions that hinge on mature recurrence-free survival data. As hospital networks adapt cell therapy workflows to vaccine logistics, time-to-first-dose post-surgery is expected to shorten, improving utilization of adjuvant windows.

Europe maintains a substantial revenue base and infrastructure depth, supported by cohesive facilitation mechanisms at the EU level and national delivery programs in priority countries. NHS England's program provides a structured channel for enrolling patients and coordinating multi-site delivery, which broadens operational capacity beyond academic centers. The neoantigen targeted therapies market in Europe is set to benefit from coordinated trial networks and real-world data collection as patient numbers rise across adjuvant indications. Sustained focus on validated biomarkers and method transparency will support health technology assessments and pricing dialogues that shape regional uptake trajectories.

Asia-Pacific is projected to post the fastest growth at a 25.72% CAGR, supported by investment in genomic infrastructure and a rising incident cancer burden that creates strong demand for post-surgical interventions. Active academic programs and expanding trial capacity in large markets are laying the groundwork for scaled manufacturing and faster turnaround times. Population HLA distributions in select countries support shared-neoantigen strategies, which can improve unit economics in prevention or adjuvant niches. Outside APAC, targeted activity in Latin America includes early-phase initiatives focused on pathogen-linked malignancies that broaden regional immunotherapy portfolios. Across regions, the neoantigen targeted therapies market share distribution will continue to track the pace of biomarker adoption, reimbursement clarity, and the diffusion of decentralized GMP capacity from academic nodes into national hospital systems.

- Achilles Therapeutics plc

- BioNTech

- CureVac N.V.

- Elicio Therapeutics, Inc.

- Evaxion Biotech A/S

- Genentech

- Geneos Therapeutics, Inc.

- Gritstone bio, Inc.

- Immatics N.V.

- Merck

- Moderna

- Nouscom AG

- Nykode Therapeutics ASA

- Transgene

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Global Cancer Incidence

- 4.2.2 Advances in High-Throughput Sequencing and Bioinformatics

- 4.2.3 Positive Late-Stage Clinical Readouts in Personalized Neoantigen Immunotherapies

- 4.2.4 Regulatory and Investor Support for Individualized Oncology

- 4.2.5 Shift to Adjuvant or MRD-Guided Use Enabled by ctDNA-Based Patient Selection

- 4.2.6 Emergence of Shared Frameshift Neoantigen Products Expanding Treatable Populations

- 4.3 Market Restraints

- 4.3.1 Manufacturing Complexity, Turnaround Time, and Cost per Patient

- 4.3.2 Clinical and Logistical Challenges Across Biopsy to Sequencing to Manufacturing Chain

- 4.3.3 Uncertain Reimbursement Models for Individualized Therapies

- 4.3.4 Tumor Heterogeneity and Antigen Escape Limiting Durability

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Therapy Type

- 5.1.1 Monotherapy

- 5.1.2 Combination Therapy

- 5.2 By Cancer Indication

- 5.2.1 Melanoma

- 5.2.2 Non-small Cell Lung Cancer (NSCLC)

- 5.2.3 Colorectal Cancer (MSI-H/dMMR)

- 5.2.4 Pancreatic Ductal Adenocarcinoma (PDAC)

- 5.2.5 Ovarian Cancer

- 5.2.6 Others

- 5.3 By Delivery Platform

- 5.3.1 mRNA-based Vaccines

- 5.3.2 Peptide-based Vaccines

- 5.3.3 DNA-based Vaccines

- 5.3.4 Others

- 5.4 By End User

- 5.4.1 Academic & Research Institutes

- 5.4.2 Tertiary Care Hospitals

- 5.4.3 Specialty Oncology Centers/Infusion Clinics

- 5.5 By Route of Administration

- 5.5.1 Intramuscular

- 5.5.2 Subcutaneous

- 5.5.3 Intradermal

- 5.5.4 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 Achilles Therapeutics plc

- 6.3.2 BioNTech SE

- 6.3.3 CureVac N.V.

- 6.3.4 Elicio Therapeutics, Inc.

- 6.3.5 Evaxion Biotech A/S

- 6.3.6 Genentech, Inc.

- 6.3.7 Geneos Therapeutics, Inc.

- 6.3.8 Gritstone bio, Inc.

- 6.3.9 Immatics N.V.

- 6.3.10 Merck & Co., Inc.

- 6.3.11 Moderna, Inc.

- 6.3.12 Nouscom AG

- 6.3.13 Nykode Therapeutics ASA

- 6.3.14 Transgene SA

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment