PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063598

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063598

Benchtop Laboratory Water Purifier - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

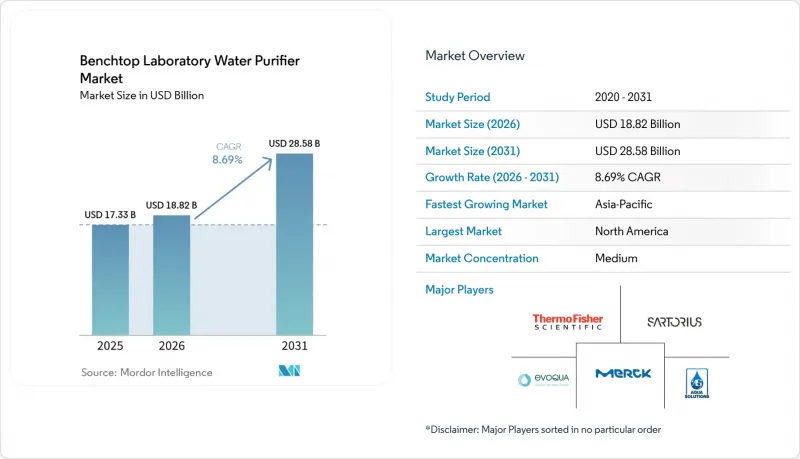

According to Mordor Intelligence, the benchtop laboratory water purifier market size is expected to grow from USD 17.33 billion in 2025 to USD 18.82 billion in 2026 and is forecast to reach USD 28.58 billion by 2031 at 8.69% CAGR over 2026-2031.

This report is Segmented by Type (Type I Ultrapure, and More), Technology (Reverse Osmosis, Electrodeionization/Ion Exchange, and, More), Water Production Capacity (≤10 L/H, 10-30 L/H, >30 L/H), End-Use Application (Pharmaceuticals & Biotechnology, and More), and Geography (North America, Europe, Asia-Pacific, and More). Market Forecasts are Provided in Terms of Value (USD).

Global Benchtop Laboratory Water Purifier Market Trends and Insights

Capital-Intensive Pharmaceutical & Biotech Capacity Additions

Biologic drug manufacturers are incorporating benchtop ultrapure modules into each clean-room suite to provide validated water on demand for media preparation, buffer pools, and sterile fill-finish steps, while preventing cross-suite contamination. Roquette's Sao Paulo innovation center, which opened in 2025, follows this model by using multiple 20 L/h dispensers instead of a single central loop, significantly reducing downtime during sanitization cycles. This modular approach aligns with India's Production Linked Incentive scheme and Brazil's innovation tax credits, both of which encourage the rapid scale-up of single-use bioreactor lines. Point-of-use qualification simplifies validation processes, as each dispenser can be documented as an independent utility. Additionally, Kincell Bio's 2026 gene-therapy expansion employs cartridge-based Type I systems in every Grade A isolator bay, eliminating 15 m of dead-leg piping per suite and reducing potential biofilm surface area by 42%.

Tightening Global Pharmacopeia Purity Standards for Lab Water

The 2025 Chinese Pharmacopoeia introduced significant updates by allowing water-for-injection through membrane separation, moving away from the distillation-only requirement and aligning with international standards. It also implemented multi-stage conductivity tests to detect sodium or ammonium breakthroughs in real time. Further, the NMPA's March 2026 guidance mandated lifecycle microbial control and online total-organic-carbon monitoring for pharmaceutical water loops.ASTM raised its D1193 Type I criteria to ≥18.2 MΩ*cm resistivity and <5 ppb TOC, a standard consistently met only by electrodeionization-plus-UV units. As a result, laboratories replacing glass stills are adopting advanced smart benchtop systems equipped with conductivity probes, TOC cells, and cloud logging capabilities, ensuring compliance with stringent regulatory audits.

High Service & Cartridge-Replacement OPEX

Consumables account for 18-22% of a benchtop unit's purchase price annually. RO membranes are priced between USD 500-1,200 per pair, electrodeionization stacks cost USD 300-800, and UV lamps range from USD 150-400. OEMs incorporate electronic chips to restrict the use of third-party cartridges, significantly increasing the cost of ion-exchange resin by 200-300%. A 20 L/h dispenser in a mid-sized QC lab incurs annual expenses of USD 3,500-5,500, excluding emergency call-outs. Universities are now extending replacement intervals from 24 to 30 months, which raises the risk of out-of-spec runs.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Expansion of Cell-&-Gene-Therapy Cleanrooms

- Boom in Semiconductor R&D Pilot Fabs Requiring Ultrapure Bench Systems

- Competition from Refurbished / Second-Hand Instruments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Type I ultrapure platforms accounted for 41.30% of the Benchtop laboratory water purifier market share and are projected to grow at a 9.87% CAGR through 2031. Laboratories utilizing high-performance liquid chromatography and ICP-MS require standards of ≥18.2 MΩ*cm resistivity and < 5 ppb TOC, which older Type II systems cannot meet. The market size for Type I units in the Benchtop laboratory water purifier sector is expected to reach USD 11.4 billion by 2031. The transition is further driven by PFAS-free construction mandates, replacing fluoropolymer tubing with PEEK or stainless alternatives to maintain undetectable fluoride levels. While Type II and Type III systems continue to serve autoclaves and glasswashers, they are losing market share as laboratory workflows become increasingly instrument-intensive.

Ultrafiltration revenue is growing at a 9.66% CAGR, outpacing the Benchtop laboratory water purifier industry average. This growth is attributed to the effectiveness of 0.05-µm hollow-fiber cassettes in reducing endotoxin levels to < 0.001 EU/mL. Reverse osmosis maintained a 35.8% revenue share in 2025 and remains the primary choice for dissolved salts. However, combined RO-E-DI-UF stacks are increasingly offered as single cabinets, eliminating the need for buyers to evaluate technologies separately. UV oxidation at 185 nm effectively breaks down organics, while 254 nm ensures microbial sterility. The integration of these four-stage processes meets the stringent reagent water standards required by CLSI GP40, particularly for molecular biology and cell-therapy laboratories.

Geography Analysis

In 2025, North America secured a dominant 39.67% share of the benchtop laboratory water purifier market. The FDA's emphasis on quality-by-design mandates electronic logging of resistivity and TOC, prompting upgrade cycles for Barnstead and Milli-Q. In a strategic move, Thermo Fisher acquired Solventum's Purification & Filtration assets for USD 4.0 billion in 2025, integrating battery-grade and medical-device water lines into the expanded Barnstead portfolio. While university refurb channels moderate new sales, aftermarket cartridges flourish, especially as OEM firmware locks dispensers to proprietary packs. In Massachusetts and North Carolina, hubs for gene and cell therapy, every Grade B side room now features UF-equipped Type I stacks.

Asia-Pacific is set to lead with a robust 7.90% CAGR through 2031. China's March 2026 Guidelines for Inspection of Pharmaceutical Water, emphasizing online microbial trending, are pushing hospitals and CDMOs to transition from distillers to membrane stacks. In India, the second tranche of the Production Linked Incentive backs 70 new biologics plants, each integrating six to eight 20 L/h dispensers. Semiconductor hubs in Taiwan, South Korea, and Japan are procuring bench units that mimic central UPW chemistry for their R&D divisions. Meanwhile, as PFAS regulations tighten, craft-beer quality labs in Australia and Vietnam are retrofitting point-of-use Type I units.

Europe, led by Germany, the UK, and France, stands as the second-largest market by value. With the harmonization of EP Chapter 0169 streamlining validation, energy-conscious labs are gravitating towards RO-based dispensers boasting over 60% water recovery, aligning with corporate net-zero ambitions.

- Aqua Solutions

- Aqua-Max of Fischer Scientific

- AquaMedix

- Aquapro Systems

- Aries FilterWorks

- Chengdu Ultrapure Technology

- Evoqua Water Technologies

- Heal Force Bio-meditech

- Hitech Instruments

- Labconco

- Marlo Incorporated

- Merck KGaA (Milli-Q)

- Organo Corporation

- Pall

- PureTec Water Systems

- Rephile Bioscience

- Sartorius AG (Arium)

- SUEZ WTS (Purite)

- Thermo Fisher Scientific

- Veolia Water Technologies (ELGA LabWater)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Capital-Intensive Pharmaceutical & Biotech Capacity Additions

- 4.2.2 Tightening Global Pharmacopeia Purity Standards for Lab Water

- 4.2.3 Rapid Expansion of Cell-&-Gene-Therapy Cleanrooms

- 4.2.4 Boom in Semiconductor R&D Pilot Fabs Requiring Ultrapure Bench Systems

- 4.2.5 Academic Lab Shift from Central RO Loops to Point-Of-Use Benchtop Units

- 4.2.6 Decentralized Micro-Brewery QA Labs Adopting ASTM Type-I Systems

- 4.3 Market Restraints

- 4.3.1 High Service & Cartridge-Replacement OPEX

- 4.3.2 Competition from Refurbished / Second-Hand Instruments

- 4.3.3 Lab-On-Chip Devices Reducing Overall Reagent-Grade Water Demand

- 4.3.4 PFAS Disposal Regulations Raising Waste-Handling Costs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 Type I (Ultrapure)

- 5.1.2 Type II (Pure)

- 5.1.3 Type III (RO/Primary)

- 5.2 By Technology

- 5.2.1 Reverse Osmosis (RO)

- 5.2.2 Electrodeionization / Ion Exchange

- 5.2.3 UV Oxidation & UV Sterilization

- 5.2.4 Ultrafiltration (UF)

- 5.3 By Water Production Capacity

- 5.3.1 ?10 L/h

- 5.3.2 10-30 L/h

- 5.3.3 >30 L/h

- 5.4 By End-use Application

- 5.4.1 Pharmaceuticals & Biotechnology

- 5.4.2 Clinical & Diagnostic Laboratories

- 5.4.3 Academic & Research Institutes

- 5.4.4 Environmental & Industrial Testing

- 5.4.5 Food & Beverage QC Laboratories

- 5.5 By Operations

- 5.5.1 Multi-Stage Purification Systems

- 5.5.2 Smart & Connected Systems (IoT-enabled)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Aqua Solutions

- 6.3.2 Aqua-Max of Fischer Scientific

- 6.3.3 AquaMedix

- 6.3.4 Aquapro Systems

- 6.3.5 Aries FilterWorks

- 6.3.6 Chengdu Ultrapure Technology

- 6.3.7 Evoqua Water Technologies

- 6.3.8 Heal Force Bio-meditech

- 6.3.9 Hitech Instruments

- 6.3.10 Labconco Corporation

- 6.3.11 Marlo Incorporated

- 6.3.12 Merck KGaA (Milli-Q)

- 6.3.13 Organo Corporation

- 6.3.14 Pall Corporation

- 6.3.15 PureTec Water Systems

- 6.3.16 Rephile Bioscience

- 6.3.17 Sartorius AG (Arium)

- 6.3.18 SUEZ WTS (Purite)

- 6.3.19 Thermo Fisher Scientific Inc.

- 6.3.20 Veolia Water Technologies (ELGA LabWater)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment