PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063616

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063616

Skincare Serums - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

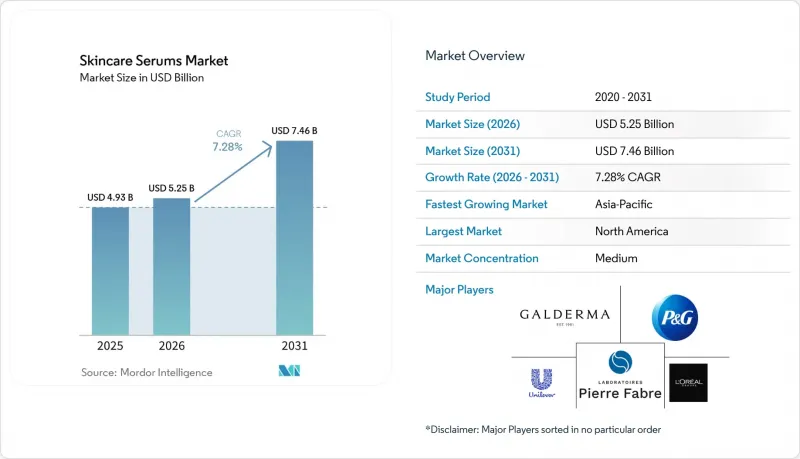

According to Mordor Intelligence, the skincare serums market size is expected to increase from USD 4.93 billion in 2025 to USD 5.25 billion in 2026 and reach USD 7.46 billion by 2031, growing at a CAGR of 7.28% over 2026-2031.

This report is Segmented by Product Type (Vitamin C, Hyaluronic Acid, Retinol/Retinoid, Peptide, Niacinamide, Multi-ingredient/Hybrid), Skin Concern (Anti-Ageing, Hydration, Acne, Brightening, Sensitivity, Repair), Gender (Women, Men), Distribution Channel (Offline, Online), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Skincare Serums Market Trends and Insights

Anti-Aging Demand Surge Among 30-45 Demographic

Clinical studies confirm that chronic PM2.5 exposure accelerates extrinsic aging by activating the aryl hydrocarbon receptor, upregulating matrix metalloproteinases, and degrading dermal collagen. Consumers aged 30-45, therefore, prioritize serums integrating palmitoyl pentapeptide-4, copper tripeptide-1, and niacinamide, seeking proactive collagen synthesis instead of reactive antioxidant defense. Brands answer with hybrid SKUs that blend retinoids, peptides, and barrier-supportive actives, compressing multi-step routines into a single bottle. Third-party dermatology seals and published clinical trials now influence purchase decisions as much as influencer marketing. North America and Western Europe lead this science-centric narrative, assisted by strict claim-substantiation rules from the FDA and European Commission.

Rising Skin-Health Awareness

Discussions once limited to wrinkles now cover barrier integrity, ceramide replenishment, and microbiome balance. Pollution-induced oxidative stress erodes tight-junction proteins and ceramide levels, undermining water retention, yet serums fortified with ceramide precursors, niacinamide, and multi-weight hyaluronic acid are reversing this decline. K-beauty's "skin-first" approach, underscored by South Korea's USD 11.4 billion cosmetics exports in 2025, spreads this barrier-centric mindset worldwide. China's USD 3.5 billion online beauty-consultation sector reinforces the trend with AI diagnostics that recommend serums based on transepidermal water loss and sebum metrics. Gen Z and millennials gravitate toward such data-backed personalization, intensifying demand for measurable skin-health outcomes.

Counterfeit & Grey-Market Products Eroding Trust

EU authorities estimate EUR 3 billion in lost cosmetics revenue and 31,717 job losses from counterfeit trade between 2016-2019. Premium serums suffer disproportionate harm because high-purity niacinamide or L-ascorbic acid is swapped for cheaper analogs that provoke irritation, denting repeat sales. Third-party sellers on global marketplaces exploit patchy brand-verification processes, while cross-border fulfillment complicates jurisdictional enforcement. Blockchain batch tracing, serialized QR codes, and customs partnerships are gaining ground, but counterfeiters now mimic holograms and serial numbers, keeping the cat-and-mouse game alive.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce & DTC Brands Lowering Entry Barriers

- Increasing Concerns Over Pollution-Induced Skin Issues

- Regulatory Crackdown on Exaggerated Efficacy Claims

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Peptide serums will outpace the overall skincare serums market at 8.12% CAGR through 2031, whereas vitamin C formulations, in spite of their 29.31% revenue, will confront maturity in North America and Europe. Clinical demonstrations that palmitoyl pentapeptide-4 and hexapeptide-8 stimulate fibroblast activity are swaying formulators toward collagen-synthesis approaches. In contrast, free L-ascorbic acid remains unstable above pH 3.5, nudging brands toward costlier derivatives, which dilutes potency and slows velocity. Retinol/retinoid serums face additional headwinds from the EU's 0.3% cap, encouraging the rapid spread of microencapsulated delivery systems that comply without efficacy loss. Hybrid, multi-active SKUs retinol plus niacinamide plus peptides satisfy the 81% of U.K. women who now prefer fewer routine steps.

Hyaluronic-acid-based serums retain a hydration niche by layering 10 kDa fractions for dermal penetration atop 2,000 kDa polymers that form a surface film. Niacinamide serums have gone mainstream thanks to wide-ranging benefits from ceramide upregulation to melanin-transfer inhibition, backed by robust safety data. ODM labs in Seoul and Incheon now prototype peptide or niacinamide hybrids for indie labels within six months, further compressing time-to-market.

Repair & barrier support will record a 10.01% CAGR through 2031, eclipsing the legacy anti-aging focus, even though the latter still contributes the single largest revenue share of 41.58% in 2025. Exhaustive studies show pollution-triggered depletion of ceramides and tight-junction proteins, intensifying demand for formulations combining ceramide NP, cholesterol, and free-fatty acids in physiological ratios. Anti-aging lines persist, yet they increasingly embed barrier-repair code in their marketing scripts, reflecting the emerging consensus that structurally sound skin ages more slowly.

Hydration-led serums leverage multi-weight hyaluronic acid to lock in surface moisture and hydrate the dermis, whereas acne/blemish solutions deploy encapsulated salicylic acid and niacinamide to reduce inflammation without peeling. Brightening options contend with ingredient bans: Europe's constraints on arbutin and kojic acid channel R&D into tranexamic acid or low-dose alpha-arbutin. Sensitivity-focused SKUs concentrate on AhR inhibition and TRPV1 damping via Centella asiatica or green-tea ferment, capitalizing on the rise of stressed-skin phenotypes in urban environments.

Geography Analysis

North America generated 37.83% of revenue in 2025, but growth is plateauing as per-capita usage approaches saturation levels and skin-minimalism curtails SKU breadth. The FDA's heightened oversight post-MoCRA raises compliance budgets but simultaneously boosts consumer confidence when products meet reporting thresholds. Mass-channel blockbusters such as Olay Super Serum reached #1 in U.S. unit sales following a 2024 reformulation that merged peptides, niacinamide, and vitamin C in one flask. Canada and Mexico deliver steady incremental volume, though U.S. DTC dominance limits domestic challenger headroom.

Asia-Pacific is set to grow at 14.67% CAGR, the fastest worldwide. China's skincare retail climbs toward RMB 701.1 billion by 2028, with domestic labels controlling 49.9% of 2024 share as they fuse ginseng, snow-mushroom, and rice-ferment storytelling with rapid ODM cycles. South Korea shipped USD 11.4 billion in cosmetics during 2025, helped by Cosmax and Kolmar Korea, which slashed launch timelines to under six months. India races toward USD 20 billion beauty spending by 2025 despite registration delays. Japan advances an epigenetic R&D storyline, exemplified by Shiseido's 2025 global rollout of New Ultimune.

Europe wrestles with tighter cosmetic legislation that caps retinol and bans certain lighteners. Beiersdorf's August 2025 release of EPICELLINE, validated through 18 months of clinical work, shows how brands respond by generating peer-reviewed dossiers. Counterfeit proliferation erodes trust and sales despite customs seizures. Elsewhere, Gulf Cooperation Council states favor halal-certified serums, while South America's macro volatility restrains discretionary spend, though Natura & Co leverages Amazonian botanicals for differentiation.

- Amorepacific Corp.

- Beiersdorf

- Clarins Group

- Coty Inc.

- Estee Lauder Companies

- Galderma

- Glossier Inc.

- Huda Beauty - Wishful

- Johnson & Johnson

- Kose Corporation

- L'Occitane International SA

- L'Oreal Group

- LVMH SE

- Natura & Co

- Pierre Fabre Group

- Procter & Gamble (Co.)

- Shiseido Company Ltd

- The Inkey List

- The Ordinary

- Unilever PLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Anti-Aging Demand Surge Among 30-45 Demographic

- 4.2.2 Rising Skin Health Awareness

- 4.2.3 Rising Disposable Income in Developing Economies

- 4.2.4 E-Commerce & DTC Brands Lowering Entry Barriers

- 4.2.5 Increasing Concerns Over Pollution-Induced Skin Issues

- 4.2.6 Micro-Dose Actives Enabling Sensitive-Skin Adoption

- 4.3 Market Restraints

- 4.3.1 Counterfeit & Grey-Market Products Eroding Trust

- 4.3.2 Regulatory Crackdown on Exaggerated Efficacy Claims

- 4.3.3 Supply Tightness for Pharma-Grade Niacinamide

- 4.3.4 "Skin-Minimalism" Trend Reducing Per-Capita SKU Count

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Vitamin C Serums

- 5.1.2 Hyaluronic Acid Serums

- 5.1.3 Retinol/Retinoid Serums

- 5.1.4 Peptide Serums

- 5.1.5 Niacinamide Serums

- 5.1.6 Multi-ingredient/Hybrid Serums

- 5.2 By Skin Concern

- 5.2.1 Anti-Ageing

- 5.2.2 Hydration & Moisturising

- 5.2.3 Acne & Blemish Control

- 5.2.4 Brightening & Pigmentation

- 5.2.5 Sensitivity & Redness

- 5.2.6 Repair & Barrier Support

- 5.3 By Gender

- 5.3.1 Women

- 5.3.2 Men

- 5.4 By Distribution Channel

- 5.4.1 Offline Retail

- 5.4.1.1 Super-/Hyper-markets

- 5.4.1.2 Beauty Specialty Stores

- 5.4.1.3 Pharmacies & Drugstores

- 5.4.2 Online Retail

- 5.4.1 Offline Retail

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Amorepacific Corp.

- 6.3.2 Beiersdorf AG

- 6.3.3 Clarins Group

- 6.3.4 Coty Inc.

- 6.3.5 Estee Lauder Companies

- 6.3.6 Galderma SA

- 6.3.7 Glossier Inc.

- 6.3.8 Huda Beauty - Wishful

- 6.3.9 Johnson & Johnson

- 6.3.10 Kose Corporation

- 6.3.11 L'Occitane International SA

- 6.3.12 L'Oreal Group

- 6.3.13 LVMH SE

- 6.3.14 Natura & Co

- 6.3.15 Pierre Fabre Group

- 6.3.16 Procter & Gamble (Co.)

- 6.3.17 Shiseido Company Ltd

- 6.3.18 The Inkey List

- 6.3.19 The Ordinary

- 6.3.20 Unilever PLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment