PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063624

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063624

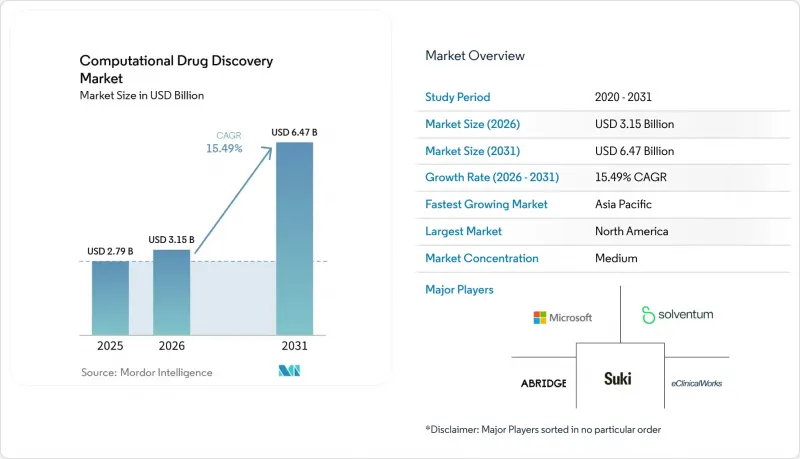

Computational Drug Discovery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the computational drug discovery market size is expected to be USD 2.79 billion in 2025, USD 3.15 billion in 2026, and reach USD 6.47 billion by 2031, growing at a CAGR of 15.49% from 2026 to 2031.

This report is Segmented by Component (Software/AI Platforms, Services), Workflow (Target Identification and Validation, and Others), End User (Pharmaceutical and Biotechnology Companies, and Others), Technology (Structure-Based Drug Design (SBDD), and Others), and Geography (North America, Europe, Asia-Pacific, and Others). Market Forecasts are Provided in Terms of Value (USD).

Global Computational Drug Discovery Market Trends and Insights

Escalating R&D Cost Pressures Driving Adoption of In-Silico Platforms

Per-drug R&D costs topped USD 2.6 billion in 2024 while Phase II oncology success rates stalled near 8%, forcing sponsors to trim attrition early. Virtual workflows collapse target-to-candidate cycles from six years to under two, letting teams fail fast and cheaply. Eli Lilly's USD 2.75 billion pact with Insilico Medicine delivered Rentosertib into Phase IIa inside 30 months, validating the approach.Venture funding, down 40% for classic biotech Series A rounds in 2025, now favors asset-light AI business models. CROs meanwhile mandate ADME/Tox predictions before wet-lab studies, cutting preclinical attrition up to one-third and saving USD 1-3 million per program.

Rapid Advances in AI/ML and Generative Chemistry Algorithms

DrugCLIP screens 10 trillion protein-molecule pairs daily, shrinking month-long hit campaigns to hours. Isomorphic Labs' IsoDDE improves antibody-antigen accuracy 2.3-fold over AlphaFold3, enabling design without crystal structures.AstraZeneca's MapDiff halves the loop from virtual hit to synthesized analog, and GPU clusters built on H100 silicon trim model-training windows from 18 months to six for Genesis Therapeutics. Latent Labs' antibody platform iterates affinity maturation 56 times faster than hybridoma, proving generative AI's reach beyond small molecules. Together these gains expand pipeline breadth while slashing per-program cost.

High Upfront HPC and Specialized-Talent Requirements

Building a fit-for-purpose cluster costs USD 2-5 million, with another USD 0.5-1 million a year to operate, figures that deter mid-size biotechs. Less than 10,000 experts globally command cross-disciplinary AI and medicinal-chemistry skills, and salaries top USD 200,000 in major hubs. Academic grants rarely cover GPUs, forcing labs into national queues stretching past six months. Emerging economies face higher cloud pricing-20-30% above U.S. rates-because of limited data-center capacity. Training supply lags demand; fewer than 50 universities offer dedicated AI-drug-discovery programs, producing only a small fraction of the 5,000 specialists needed yearly.

Other drivers and restraints analyzed in the detailed report include:

- Cloud/SaaS Delivery Models Lowering Entry Barriers

- Regulatory Embrace of Model-Informed Drug-Development Guidelines

- Data Silos and Poor Interoperability Across Multi-Omics Datasets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software/AI platforms led the computational drug discovery market size with a 59.58% revenue share in 2025 and are projected to expand at a 17.24% CAGR to 2031. Their dominance reflects pharma's pivot toward owning core algorithms, exemplified by Lilly's decision to run Insilico's generative engine on internal servers after the USD 2.75 billion deal. Services still matter for smaller sponsors seeking turnkey campaigns, but cloud-native pricing models-USD 0.05 per ADME prediction on Mind the Byte-have eroded the premium once charged by CROs.

Rising subscription footprints mean platform vendors now bundle quarterly model updates, compliance toolkits, and user training, blurring the former product-service divide. Certara's Simcyp package, re-launched in 2025, adds automatic PBPK template refreshes and on-demand webinars, fostering stickiness while helping clients satisfy ICH M15 traceability rules. Services revenue therefore grows modestly as sponsors emphasize skills transfer rather than perpetual outsourcing.

Target identification and validation held 56.53% of 2025 spending, yet lead discovery is advancing at a 16.82% CAGR, tightening the gap. Breakthroughs like DrugCLIP's 10 trillion-pair daily throughput allow sponsors to compress hit-identification from six months to under a week, turbo-charging internal medicinal chemistry.

Ultra-large screens also democratize fragment expansion for rare-disease targets once deemed commercially unattractive. PyRMD2Dock's 7.3% sub-micromolar hit rate against CD28 shows that algorithmic scale can rival physical HTS quality for a fraction of the cost. Regulatory constraints still require wet-lab confirmation for pre-clinical ADME/Tox predictions, but integration with quantum-enabled free-energy estimation shortens cycle times even there.

Geography Analysis

North America contributed 47.76% of 2025 global revenue, driven by venture capital depth, dense pharma headquarters, and first-mover cloud adoption. FDA programs such as model-informed paired meetings and Project Optimus have accelerated regulatory comfort with algorithmic dossiers, reducing cycle times and anchoring platform vendors' largest commercial footprints.

Asia-Pacific posts the fastest expansion, a 17.34% CAGR, as China, India, and Japan bankroll sovereign AI and streamline approval pathways. China hosts one-third of the global innovation pipeline, executing parallel in-silico and wet-lab campaigns that shorten hit-to-IND durations to 18 months. India's Peptris capital-raise and Japan's Ono-Congruence partnership in 2026 highlight rising regional sophistication in peptide and biophysics-driven discovery, respectively.

Europe benefits from high-caliber academic consortia and EMA openness to digital-biology evidence, though venture funding lags the United States and regulatory fragmentation across member states hampers scale. Middle East & Africa and South America remain nascent but attract multinational clinical trials as local CROs adopt cloud SaaS platforms that circumvent HPC shortages.

- Atomwise Inc.

- Benevolent AI

- BioSolveIT

- Certara USA

- Charles River

- Cloud Pharmaceuticals

- Cresset

- Cyclica Inc.

- Dassault Systemes

- Deep Genomics

- Evotec

- Exscientia plc

- Iktos

- Insilico Medicine

- NVIDIA

- Optibrium Ltd.

- Recursion Pharmaceuticals

- Schrodinger Inc.

- Simulations Plus Inc.

- XtalPi

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating R&D Cost Pressures Driving Adoption of In-Silico Platforms

- 4.2.2 Rapid Advances in AI/ML and Generative Chemistry Algorithms

- 4.2.3 Cloud/Saas Delivery Models Lowering Entry Barriers

- 4.2.4 Regulatory Embrace of Model-Informed Drug Development (MIDD) Guidelines

- 4.2.5 Quantum Computing Breakthroughs Enabling Sub-Hour Free-Energy Calculations

- 4.2.6 Patient Digital-Twin Integration Fuelling In-Silico Trial Simulation Demand

- 4.3 Market Restraints

- 4.3.1 High Upfront HPC and Specialized-Talent Requirements

- 4.3.2 Data Silos and Poor Interoperability Across Multi-Omics Datasets

- 4.3.3 Regulatory Pushback on Explainability of AI-Designed Molecules

- 4.3.4 GPU/Compute Supply-Chain Crunch Limiting Capacity 2026-2029

- 4.4 Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software / AI platforms

- 5.1.2 Services

- 5.2 By Workflow

- 5.2.1 Target Identification and Validation

- 5.2.2 Lead Discovery

- 5.2.3 Lead Optimization

- 5.2.4 Pre-clinical ADME/Tox Prediction

- 5.2.5 Others

- 5.3 By End-user

- 5.3.1 Pharmaceutical and Biotechnology Companies

- 5.3.2 Contract Research Organizations (CROs)

- 5.3.3 Academic and Research Institutes

- 5.4 By Technology

- 5.4.1 Structure-Based Drug Design (SBDD)

- 5.4.2 Ligand-Based Drug Design (LBDD)

- 5.4.3 AI / Generative-AI Platforms

- 5.4.4 Molecular Dynamics and Simulation

- 5.4.5 Quantum / Accelerated Computing

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1 Atomwise Inc.

- 6.3.2 BenevolentAI

- 6.3.3 BioSolveIT GmbH

- 6.3.4 Certara USA Inc.

- 6.3.5 Charles River Laboratories

- 6.3.6 Cloud Pharmaceuticals

- 6.3.7 Cresset

- 6.3.8 Cyclica Inc.

- 6.3.9 Dassault Systemes

- 6.3.10 Deep Genomics

- 6.3.11 Evotec SE

- 6.3.12 Exscientia plc

- 6.3.13 Iktos

- 6.3.14 Insilico Medicine

- 6.3.15 NVIDIA

- 6.3.16 Optibrium Ltd.

- 6.3.17 Recursion Pharmaceuticals

- 6.3.18 Schrodinger Inc.

- 6.3.19 Simulations Plus Inc.

- 6.3.20 XtalPi Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment