PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063627

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063627

Thermoplastic Elastomers In Medical Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

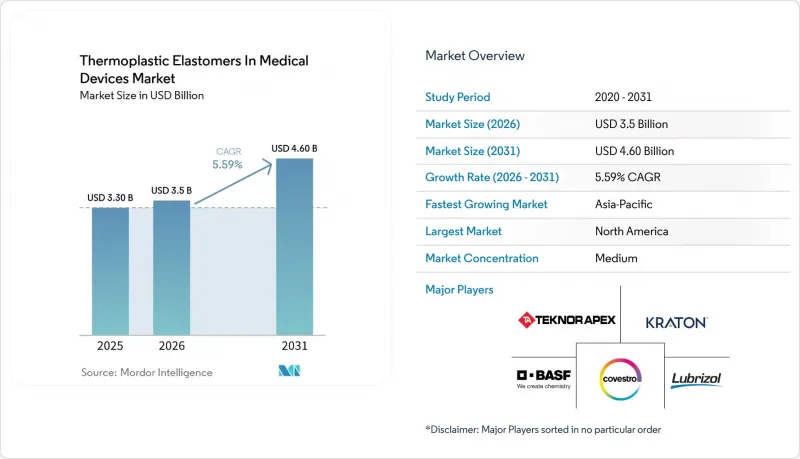

According to Mordor Intelligence, the thermoplastic elastomers in medical devices market size was valued at USD 3.30 billion in 2025 and is estimated to grow from USD 3.5 billion in 2026 to reach USD 4.60 billion by 2031, at a CAGR of 5.59% during the forecast period (2026-2031).

This report is Segmented by Material Type (Thermoplastic Elastomer - Styrenic / Styrene-Ethylene-Butylene-Styrene (TPE-S/SEBS), and More), Application (Catheters & Tubing, and More), Processing Technology (Extrusion, Injection Molding, Blow Molding & Film, and More), and Geography (North America, Europe, and More). Market Forecasts are Provided in Value (USD).

Global Thermoplastic Elastomers In Medical Devices Market Trends and Insights

Shift Away from PVC/Phthalates in Sensitive Uses

European Regulation 2023/2482 identifies DEHP as a substance of concern, setting a final application deadline of January 1, 2029, for medical devices containing DEHP. This provides OEMs with a 36-month window to reformulate, prompting a shift toward SEBS and thermoplastic polyurethane (TPU) alternatives that eliminate plasticizer leaching concerns. Guidance issued in 2024 requires a benefit-risk analysis for devices releasing more than 10 µg/kg body weight/day of plasticizer, effectively disqualifying traditional PVC lines. North American manufacturers are aligning their timelines with European counterparts to maintain global consistency, driving a collective shift in the thermoplastic elastomers in the medical devices market toward phthalate-free materials.

Growth in Minimally Invasive, Catheter-Based Therapies

Catheter laboratories are expanding their range of cardiovascular, neurovascular, and urological procedures, which rely on kink-resistant, pushable shafts. Polyether block amide (PEBA) compounds, such as Pebax Rnew, reduce advancement force by 50% compared to nylon 12, minimizing vessel trauma and shortening procedure times. Flexural-fatigue testing demonstrates that PEBA shafts endure 10,000 cycles at 90-degree bends, nearly tripling the lifespan of conventional polyurethane catheters, supporting broader adoption in same-day discharge environments. FDA 510(k) pathways enable manufacturers to update catheter designs using existing master files, reducing approval times by half and driving further penetration in the thermoplastic elastomers in medical devices market.

E &L Validation and Sterilization-Induced Property Shifts

ISO 10993-18:2020 requires detailed chemical-profile testing, with each E&L program costing approximately USD 300,000 and taking nine months to complete. Gamma sterilization at 50 kGy can decrease the tensile strength of unmodified PEBA by 25%, prompting compounders to include antioxidant packages, which subsequently introduce new extractables. Ethylene-oxide sterilization leaves residual ethylene chlorohydrin, which must remain below 4 µg/device under ISO 10993-7:2024 limits. These scientific and regulatory challenges extend development timelines, restraining near-term growth of the thermoplastic elastomers in the medical devices market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Wearable and Home-Care Devices

- OEM Change-Control Burden Under EU MDR Favors Stable Suppliers

- Cost Premium vs PVC and Silicone in Volume Applications

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, styrenic block copolymers accounted for 43.18% of the thermoplastic elastomers in medical devices market size due to their cost-effective transparency and 50 kGy gamma stability. PEBA is expected to grow at an annual rate of 7.12% through 2031, driven by the increasing demand for neurovascular and peripheral-vascular catheters requiring ultra-thin, kink-resistant walls. Arkema's bio-based Pebax Rnew 30R53, with 30% castor-oil content, achieves Shore D 53 hardness, aligning with EU Green Deal procurement rules. TPU held 22% of revenue in 2025, preferred for infusion-set tubing designed to withstand pump-driven abrasion for seven days of wearable use. TPE-E and TPC are suitable for autoclave applications up to 121 °C, although their ester linkages limit gamma stability. TPV and TPO remain below 8%, constrained by opacity and higher extractables.

Geography Analysis

In 2025, North America accounted for 36.33% of the revenue in the thermoplastic elastomers for medical devices market. This dominance is supported by key clusters in Minnesota, Massachusetts, and California, where industry leaders such as Medtronic, Abbott, and Boston Scientific are scaling new catheter and wearable lines under FDA scrutiny. Meanwhile, Europe, contributing a steady 28% to the market revenue, maintains its position due to stricter MDR documentation, which benefits established material suppliers capable of providing comprehensive E&L dossiers. Asia-Pacific, currently holding 26% of the market, is expected to drive growth, with an expansion rate of 7.63% projected through 2031.

The region's growth is driven by three key factors. Firstly, with China and India promoting local sourcing, Teknor Apex's 2026 joint venture, PolyTek, with DCM Shriram, is set to streamline operations. Their in-region compounding reduces lead times by six weeks. Secondly, as reimbursement for continuous-glucose monitoring expands, millions more lives are covered, encouraging sensor manufacturers to localize assembly. Lastly, Japanese and South Korean OEMs are focusing on high-purity grades; suppliers meeting ISO 10993-18 standards can secure price premiums of 10-15%.

In contrast, Latin America and the combined regions of the Middle East & Africa account for a mere 8% of the thermoplastic elastomers in medical devices market revenue. High import duties and a limited installed base discourage investments in advanced two-shot injection presses. Additionally, while legacy PVC remains acceptable for short-term consumables, it is notable that major multinationals might redirect surplus capacity from the West to these regions. This shift could occur once DEHP sales face restrictions in Europe and North America.

- Actega DS GmbH

- Arkema S.A.

- Avient Corporation

- BASF

- Celanese Corporation

- Compagnie de Saint-Gobain S.A.

- Covestro

- Duke Extrusion

- Dynasol Group

- Elastron Kimya A.S.

- HEXPOL AB

- KRAIBURG TPE GmbH & Co. KG

- Kraton

- Kuraray Co., Ltd.

- Lubrizol

- Mitsubishi Chemical

- Nordson MEDICAL

- RTP Company

- Tekni-Plex, Inc.

- Teknor Apex Company

- TSRC Corporation

- Zeus Company Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift Away from PVC/Phthalates in Sensitive Uses

- 4.2.2 Growth in Minimally Invasive, Catheter-Based Therapies

- 4.2.3 Expansion of Wearable and Home-Care Devices

- 4.2.4 OEM Change-Control Burden Under EU MDR Favors Stable Suppliers

- 4.2.5 Overmolding-Driven Part Consolidation (Bonding To PP/PA)

- 4.2.6 Gamma-Stable Transparent Tpes Enabling PVC-Free IV/Tubing

- 4.3 Market Restraints

- 4.3.1 E&L Validation and Sterilization-Induced Property Shifts

- 4.3.2 Cost Premium Vs PVC and Silicone in Volume Applications

- 4.3.3 OEM Material Change-Control Under MDR Extends Timelines

- 4.3.4 Supply-Chain Fragility for Medical-Grade Resins, Sterilization Bottlenecks

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter;s Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material Type

- 5.1.1 Thermoplastic Elastomer - Styrenic / Styrene-Ethylene-Butylene-Styrene (TPE-S/SEBS)

- 5.1.2 Thermoplastic Polyurethane (TPU)

- 5.1.3 Thermoplastic Elastomer - Amide / Polyether Block Amide (TPE-A/PEBA)

- 5.1.4 Thermoplastic Elastomer - Polyester / Thermoplastic Copolyester (TPE-E/TPC)

- 5.1.5 Thermoplastic Vulcanizate (TPV)

- 5.1.6 Thermoplastic Polyolefin (TPO)

- 5.2 By Application

- 5.2.1 Catheters & Tubing

- 5.2.2 Syringes & Plungers

- 5.2.3 Stoppers & Seals

- 5.2.4 Connectors & Device Housings

- 5.2.5 Wearables & Skin-Contact Interfaces

- 5.3 By Processing Technology

- 5.3.1 Extrusion

- 5.3.2 Injection Molding

- 5.3.3 Blow Molding & Film

- 5.3.4 Overmolding & 2K

- 5.3.5 Additive / Other

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Actega DS GmbH

- 6.3.2 Arkema S.A.

- 6.3.3 Avient Corporation

- 6.3.4 BASF SE

- 6.3.5 Celanese Corporation

- 6.3.6 Compagnie de Saint-Gobain S.A.

- 6.3.7 Covestro AG

- 6.3.8 Duke Extrusion

- 6.3.9 Dynasol Group

- 6.3.10 Elastron Kimya A.S.

- 6.3.11 HEXPOL AB

- 6.3.12 KRAIBURG TPE GmbH & Co. KG

- 6.3.13 Kraton Corporation

- 6.3.14 Kuraray Co., Ltd.

- 6.3.15 Lubrizol Corporation

- 6.3.16 Mitsubishi Chemical Corporation

- 6.3.17 Nordson MEDICAL

- 6.3.18 RTP Company

- 6.3.19 Tekni-Plex, Inc.

- 6.3.20 Teknor Apex Company

- 6.3.21 TSRC Corporation

- 6.3.22 Zeus Company Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment