PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063634

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063634

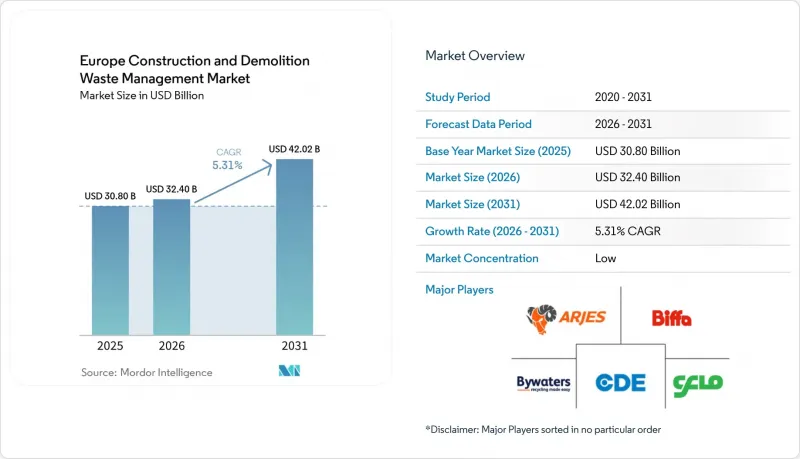

Europe Construction And Demolition Waste Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the europe construction and demolition waste management market size is expected to grow from USD 30.80 billion in 2025 to USD 32.40 billion in 2026 and is forecast to reach USD 42.02 billion by 2031 at 5.31% CAGR over 2026-2031.

This report is Segmented by Waste Type (Non-Hazardous Waste, and Hazardous Waste), by Material (Concrete & Bricks, Asphalt, and More), by Service (Collection & Transportation, Sorting & Segregation, and More), and by Geography (United Kingdom, Germany, France, Italy, Spain, BENELUX, NORDICS, and Rest of Europe). Market Forecasts are Provided in Terms of Value (USD).

Europe Construction And Demolition Waste Management Market Trends and Insights

Corporate Sustainability Commitments and ESG Reporting Requirements Pushing Waste Reduction

The Corporate Sustainability Reporting Directive has increased disclosure requirements for large companies in 2024, emphasizing waste generation, recycling, and value chain impacts. Large contractors now prioritize waste diversion in performance systems and disclose waste flows, favoring verified recovery solutions. CRH reported 98% of its locations had waste management plans in 2024, recovering 44.7 million tonnes of waste and by-products. Balfour Beatty showed progress in its 2024 sustainability plan, with assured greenhouse gas disclosures boosting customer confidence in circular delivery. Financial access is shifting as verified waste and circularity data influence green financing eligibility. The Irish Green Building Council's Home Performance Index integrates circularity into housing design, enhancing material recovery. France's EPR organization for construction expanded professional deposit sites, improving collection and reporting for contractors across regions.

Growing Adoption of Circular Economy Principles Across the European Construction Sector

The EU's Circular Material Use Rate reached 12.2% in 2024, reflecting gradual progress in secondary material usage. Regions are implementing circular policies through mandates for separate collection, on-site sorting, and selective demolition. Flanders expanded mandatory sorting in 2024, requiring more material streams to be handled separately, improving feedstock quality for recyclers. Nordic countries enhanced building surveys and material mapping under new rules, increasing transparency of demolition flows. Denmark's Solum facility showcased robotic sorting's potential to improve purity and reduce emissions. The European Commission's end-of-waste work for aggregates and other materials aims to harmonize definitions, enabling freer cross-border movement and scaling into higher-value applications. These developments strengthen market alignment with circular rules and raise standards for selective demolition and quality control.

High Initial Capital Investment for Advanced Waste Processing Facilities and Equipment

Shifting from manual to automated sorting requires significant capital that smaller operators struggle to finance. New deployments combine robotic systems with optical and hyperspectral imaging, which adds to upfront costs alongside systems integration. Danish evidence shows that robotic sorting can improve purity and lower emissions per tonne, but the pathway still demands coordinated funding and technical partnerships that smaller firms cannot easily secure. France's policy support includes funding to increase recycling capacity for building materials, yet medium-term capacity build-out remains constrained by lead times and the need for robust quality management across plants. The Joint Research Centre finds that advanced C&D recycling methods can reduce life cycle emissions per tonne but still require new investments to close the processing gap across the EU. Where national frameworks update end-of-waste rules, operators must also invest in documentation and conformity assessment, which increases setup costs before monetization of higher-grade outputs begins. These realities favor well-capitalized firms or those with long-term supply contracts that de-risk repayment, which influences consolidation dynamics in the Europe construction and demolition waste management market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Recycled Aggregates Due to Natural Resource Depletion and Aggregate Shortages

- Increasing Infrastructure Renovation and Urban Regeneration Projects in Aging European Cities

- Contamination Issues Reducing Quality and Market Acceptance of Recycled C&D Materials

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The non-hazardous segment accounted for 98.1% of the Europe construction and demolition waste management market share in 2025, which reflects the mass dominance of mineral fractions in the regional waste mix. Across Europe, the built environment produces large volumes of concrete, brick, and asphalt flows that underpin throughput at processing sites, with annual C&D waste generation measured in the hundreds of millions of tonnes across the EU. Policy actions such as separate collection mandates and selective demolition protocols are raising the baseline for recovery and creating stable logistics for predictable material streams. France's national roadmap sets aggressive targets for the separate collection of mineral waste by 2027, backed by national EPR implementation that helps standardize practice across regions. Under this policy environment, non-hazardous waste management is on a steady expansion path, with investments now targeting greater purity and higher-value outlets for recycled aggregates and other mineral derivatives.

Hazardous waste remains small by tonnage, yet it is gaining traction because pre-demolition audits and stricter handling rules are more common and better enforced. Member states with forward plans on asbestos removal and wood contamination are scaling up solutions to capture and treat this fraction under tighter supervision frameworks. Nordic countries have strengthened building surveys under new legal frameworks, which improves discovery and more reliable routing of hazardous fractions from rehabilitation projects. National requirements for documented handling under environmental management certifications also tighten data capture and governance for hazardous loads. In practice, hazardous material routing increases cost and time requirements per project and requires specialized logistics, which supports the business case for integrated operators with treatment capacity. This also materializes in contract structures that partition risk across the demolition and post-processing phases and align incentives for safety and compliance.

List of Companies Covered in this Report:

- ARJES

- Biffa

- Bywaters

- CDE Group

- CFlo World Limited

- DAW Group

- Eastern Waste Disposal (EWD)

- EnviroCraft Waste Solutions

- Geocycle (Holcim Group)

- ISM Waste & Recycling

- McLanahan

- Metso

- REMEX GmbH

- Renewi

- SmartEnds

- Stena Metall AB

- SUEZ

- Veolia

- AESG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Industry Value / Supply-Chain Analysis

- 4.3 Market Drivers

- 4.3.1 Corporate sustainability commitments and ESG reporting requirements pushing waste reduction

- 4.3.2 Growing adoption of circular economy principles across European construction sector

- 4.3.3 Rising demand for recycled aggregates due to natural resource depletion and aggregate shortages

- 4.3.4 Increasing infrastructure renovation and urban regeneration projects in aging European cities

- 4.3.5 Technological advancements in automated sorting and AI-based waste segregation systems

- 4.3.6 Rising construction activity driven by residential housing demand and green building initiatives

- 4.4 Market Restraints

- 4.4.1 High initial capital investment for advanced waste processing facilities and equipment

- 4.4.2 Contamination issues reducing quality and market acceptance of recycled C&D materials

- 4.4.3 Lack of standardized quality specifications for recycled materials across EU member states

- 4.4.4 Fragmented waste collection infrastructure in Eastern European countries

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Circular Economy & Material Flow Analysis

- 4.9 Environmental & Life-Cycle Assessment Considerations

5 Market Size & Growth Forecasts

- 5.1 By Waste Type

- 5.1.1 Non-Hazardous Waste

- 5.1.2 Hazardous Waste

- 5.2 By Material

- 5.2.1 Concrete & Bricks

- 5.2.2 Asphalt

- 5.2.3 Metal

- 5.2.4 Timber

- 5.2.5 Soil and Sand

- 5.2.6 Gypsum & Drywall

- 5.2.7 Others (Plastic, Wood, Glass)

- 5.3 By Service

- 5.3.1 Collection & Transportation

- 5.3.2 Sorting & Segregation

- 5.3.3 Recycling & Material Recovery

- 5.3.4 Landfilling & Disposal

- 5.4 By Geography

- 5.4.1 United Kingdom

- 5.4.2 Germany

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.4.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.4.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 ARJES

- 6.4.2 Biffa

- 6.4.3 Bywaters

- 6.4.4 CDE Group

- 6.4.5 CFlo World Limited

- 6.4.6 DAW Group

- 6.4.7 Eastern Waste Disposal (EWD)

- 6.4.8 EnviroCraft Waste Solutions

- 6.4.9 Geocycle (Holcim Group)

- 6.4.10 ISM Waste & Recycling

- 6.4.11 McLanahan

- 6.4.12 Metso

- 6.4.13 REMEX GmbH

- 6.4.14 Renewi

- 6.4.15 SmartEnds

- 6.4.16 Stena Metall AB

- 6.4.17 SUEZ

- 6.4.18 Veolia

- 6.4.19 AESG

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment