PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063651

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063651

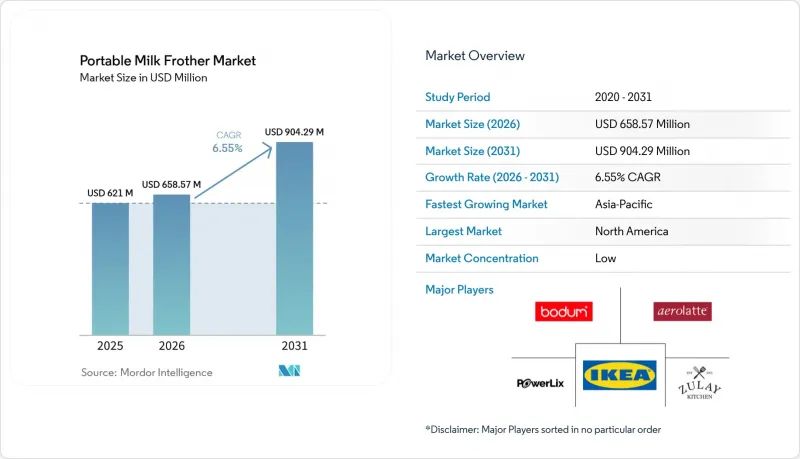

Portable Milk Frother - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the portable milk frother market size is projected to be USD 621 million in 2025, USD 658.57 million in 2026, and reach USD 904.29 million by 2031, growing at a CAGR of 6.55% from 2026 to 2031.

This report is Segmented by Product Type (Handheld, Electric, Multifunctional), Power Source (Battery-Powered, Rechargeable USB/Type-C, Manual), End-User (Household and Commercial), Distribution Channel (B2C/Retail and B2B), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). Forecasts are in Value (USD Million).

Global Portable Milk Frother Market Trends and Insights

Home Brewing Dominance and Rising At-Home Specialty Coffee Routines

Home coffee preparation remains structurally elevated in 2026, as consumers preserve habits formed during the pandemic and refine their routines with simple, effective tools. Specialty coffee engagement reported by industry associations supports this shift, with more households bringing cafe-style methods into the kitchen and adopting accessories that improve drink texture and consistency. Portable frothers fit these patterns because they create microfoam quickly without requiring counter space, water lines, or expensive training, which reduces the barrier to better-tasting cappuccinos and lattes at home. As households experiment with iced and hot formats, the same tool works across dairy and non-dairy options, further increasing utility and daily use frequency. Adjacent appliance categories, including entry-level espresso and drip systems, continue to grow in the United States and reinforce an ecosystem of accessories that complement home barista behavior. Together, these dynamics extend the portable milk frother market beyond hobbyists to mainstream home brewers who want professional results with minimal complexity.

E-Commerce Access and Discovery Driving Low-Ticket Device Adoption

Online marketplaces compress discovery and evaluation into a few clicks, which benefits low-ticket kitchen tools that promise visible results on the first use. Digital-first brands amplify this with video demos, high-volume reviews, and quick delivery promises that convert browsing into checkout across cooking and beverage categories. Direct-to-consumer strategies also unlock first-party data and enable subscription bundles with complementary items, building retention that would be difficult in a purely wholesale model. These capabilities matter for handheld frothers because buyers often add them to baskets that already include beans, syrups, or mugs, which keeps the price-to-value ratio attractive without discounting. For the portable milk frother market, online channels broaden reach into households that may not visit specialty shops and provide a steady flow of replenishment opportunities tied to coffee and tea rituals. Growth posted by major small-appliance companies in digital channels suggests this online shift is a durable structural factor rather than a temporary sales spike.

Commoditized Competition and Price Pressure on Marketplaces

The category is highly fragmented and characterized by aggressive price matching on search-driven product grids, which compresses margins for many sellers. A dispersed long tail of private-label listings competes with established brands on colorways, minor feature sets, and review volume rather than durable performance advantages. This environment supports rapid unit growth but can slow value growth, especially when low-priced products rise to the top of recommendation slots. The portable milk frother market, therefore, exhibits a concentration pattern in which the top ten brands hold a small, combined share, and category leaders protect their positions through branding, quality controls, and channel discipline. Established players respond by investing in certifications, packaging, and post-purchase support that reduce returns and sustain ratings, while newcomers often trade speed for price. As marketplaces tighten policy and counterfeit enforcement, differentiation based on durability and compliance can improve resilience even if headline prices remain competitive.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Plant-Based Milks and Cold Foam Habits Expanding Use-Cases

- USB-C Rechargeable Designs Cut Battery Waste and Boost Travel Utility

- Substitutes Cap Demand: Espresso Steam Wands, Immersion Blenders, Manual Plungers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electric portable frothers accounted for 65.4% of 2025 revenue and are forecast to grow at 6.63% through 2031, indicating that push-button convenience remains the dominant purchase driver in this category. The portable milk frother market size for electric formats benefits from quick foam generation, minimal cleanup, and versatile use across dairy and non-dairy beverages, which suits everyday routines in compact kitchens. Influenced by cafe textures and home recipe experimentation, consumers align around consistent outcomes over manual skill, so electric wands become the default choice for first-time buyers and upgraders. Premium brands position electric frothers with improved shafts, motors, and ergonomic grips, while value brands focus on color options and fast shipping to stand out on marketplaces. As formats evolve, companies also introduce temperature-aware features and dedicated heads to stabilize foam with different milks, which supports higher average selling prices and encourages accessory purchases.

Manual handheld whisks and pump-based devices continue to appeal to minimalists and to users who prefer complete control over foam density. However, their share contracts as rechargeable units add convenience at accessible prices. These manual tools are well-suited to off-grid or travel contexts and offer the advantage of mechanical simplicity without charging requirements. Multifunctional devices in the "others" sub-segment integrate dedicated pitchers, travel tumblers, or temperature indicators that create a premium experience beyond standard handheld wands. As brands educate users on technique, manual sets remain relevant as second devices in households that already own an electric wand but want a backup or a travel kit. The portable milk frother market accommodates both styles, although the center of gravity remains with electric formats due to speed, predictability, and channel visibility.

Battery-powered AA or AAA frothers commanded 61.5% of the 2025 share, supported by low upfront prices and easy availability at big-box stores and online marketplaces that carry alkaline batteries as everyday goods. This category favors impulse purchases and quick setup, since units can be used immediately without charging, which matters for gifting and last-minute pantry additions. However, rechargeable USB-C models are the fastest-growing power segment at a projected 6.81% CAGR, a sign that buyers value universal charging and fewer consumables in daily routines. Brands that operate broader cordless ecosystems have an advantage because a single dock can power multiple small appliances, reducing clutter and fostering attachment across product families. The portable milk frother market, therefore, exhibits a gradual shift from disposables to rechargeable formats as features and pricing converge.

Manual power remains relevant in contexts where charging and battery waste are concerns, or where users want a simple device that works anywhere with no cords or cells to manage. In parallel, rechargeable growth is tempered by air-cargo rules for lithium shipments, which require brands to manage state-of-charge thresholds and labeling for compliant fulfillment. Compliance investments favor established players that can absorb overhead and standardize processes across warehouses and carriers, thereby differentiating offerings beyond price alone. Over time, as customers upgrade from battery-powered to rechargeable devices, opportunities for accessory attachments and replacement heads emerge to extend product life. The portable milk frother industry thus balances convenience, compliance, and sustainability in a way that supports steady mix shifts toward cordless charging.

Geography Analysis

North America accounted for 34.2% of global revenue in 2025, reflecting a mature home-coffee culture, high ecommerce penetration, and widespread availability of compatible accessories across price points. Specialty coffee engagement and cafe-inspired drink formats anchor daily routines, which support demand for tools that create reliable foam profiles in both dairy and non-dairy drinks. Growth is steadier in this region due to higher installed bases and slower category rotation among long-time users, yet new colorways and cordless formats keep refresh cycles active. Compliance and safety practices have high visibility, so certifications and documented testing help brands win trust with both retail buyers and procurement teams. The portable milk frother market size in North America, therefore, reflects a mix of replacement-driven volume and premium upgrades rather than new-to-category expansion.

Asia-Pacific is the fastest-growing region, with a 7.02% CAGR, as urban cafe culture, rising disposable incomes, and strong mobile-first shopping behavior drive accessory demand. As more cafes and quick-service chains standardize foam textures in iced and hot drinks, home users look for ways to mirror those experiences with compact devices. E-commerce infrastructure in key markets enables brands to launch color and feature refreshes at speed, which keeps attention high among younger consumers. Logistics and battery shipping rules are relevant in this region due to cross-border flows and marketplace fulfillment models, so compliance maturity provides an execution edge. The portable milk frother market benefits as local and global brands create offerings tuned to regional tastes and kitchen layouts, including apartment-friendly kits and travel-ready options.

Europe grows steadily on the back of established espresso culture, strong interest in sustainability, and a preference for durable materials and repairability in small appliances. Brands emphasize rechargeable formats and recyclable packaging as environmental expectations shape product selection and messaging. Retailers curate displays that focus on materials, ergonomics, and certifications, which signal reliability and align with consumer expectations for long-lived devices. As foam-forward recipes gain traction in iced and hot menus, home users expect consistent texture without noise or splashing, which drives attention to motor quality and head design. The portable milk frother market in Europe, therefore, tilts toward premium features and conscientious design while still offering entry-level options to bring new users into the category.

- Zulay Kitchen

- PowerLix

- Aerolatte

- IKEA (PRODUKT)

- Bodum (SCHIUMA)

- Maestri House

- Dualit

- Hario (Creamer Z)

- Bean Envy

- Bonsenkitchen

- Epare

- Ozeri

- SimpleTaste

- Chefman

- Bialetti (Tuttocrema)

- Norpro

- MHW-3BOMBER

- Golde (Superwhisk)

- Teaspressa

- Kitchen Guru

- CNPUSA

- Barista Brew Labs

- FoodVille

- AKEfit

- NNEDSZ

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 Home brewing dominance and rising at-home specialty coffee routines

- 4.1.2 E-commerce access and discovery driving low-ticket device adoption

- 4.1.3 Growth of plant-based milks and cold foam habits expanding use-cases

- 4.1.4 Impulse gifting and sub-USD 25 price tiers expand category entry

- 4.1.5 USB-C rechargeable designs cut battery waste and boost travel utility

- 4.1.6 Social virality of beverage trends (e.g., whipped/dalgona; seasonal foam) spikes demand

- 4.2 Market Restraints

- 4.2.1 Commoditized competition and price pressure on marketplaces

- 4.2.2 Substitutes (espresso steam wands, immersion blenders, manual plungers) cap demand

- 4.2.3 Durability/warranty issues and sporadic safety incidents erode trust

- 4.2.4 Lithium battery air-cargo/SoC rules add cross-border cost/complexity for rechargeables

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Bargaining Power of Buyers

- 4.4.4 Threat of Substitutes

- 4.4.5 Industry Rivalry

- 4.5 Insights Into The Latest Trends And Innovations in the Industry

- 4.6 Insights On Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, Etc.) In The Industry

5 Market Size & Growth Forecasts (Value in USD Million)

- 5.1 By Product Type

- 5.1.1 Handheld (Manual Push / Whisk Rod)

- 5.1.2 Electric Portable Frothers

- 5.1.3 Others (Multi-Functional, Travel-mug-integrated frothers, etc.)

- 5.2 By Power Source

- 5.2.1 Battery-powered (AA/AAA)

- 5.2.2 Rechargeable (USB / Type-C)

- 5.2.3 Manual

- 5.3 By End-user

- 5.3.1 Household/Residential

- 5.3.2 Commercial (Cafes, small offices, boutique setups)

- 5.4 By Distribution Channel

- 5.4.1 B2C/Retail Channels

- 5.4.1.1 Multi-brand Stores

- 5.4.1.2 Exclusive Brand Outlets

- 5.4.1.3 Online

- 5.4.1.4 Other Distribution Channels

- 5.4.2 B2B/Direct Sales

- 5.4.1 B2C/Retail Channels

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 India

- 5.5.4.2 China

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East And Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East And Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Zulay Kitchen

- 6.4.2 PowerLix

- 6.4.3 Aerolatte

- 6.4.4 IKEA (PRODUKT)

- 6.4.5 Bodum (SCHIUMA)

- 6.4.6 Maestri House

- 6.4.7 Dualit

- 6.4.8 Hario (Creamer Z)

- 6.4.9 Bean Envy

- 6.4.10 Bonsenkitchen

- 6.4.11 Epare

- 6.4.12 Ozeri

- 6.4.13 SimpleTaste

- 6.4.14 Chefman

- 6.4.15 Bialetti (Tuttocrema)

- 6.4.16 Norpro

- 6.4.17 MHW-3BOMBER

- 6.4.18 Golde (Superwhisk)

- 6.4.19 Teaspressa

- 6.4.20 Kitchen Guru

- 6.4.21 CNPUSA

- 6.4.22 Barista Brew Labs

- 6.4.23 FoodVille

- 6.4.24 AKEfit

- 6.4.25 NNEDSZ

7 Market Opportunities & Future Outlook

- 7.1 USB-C travel frother kits bundled with spill-proof insulated mugs and carry cases for on-the-go cold-foam and matcha

- 7.2 Plant-based micro-foam optimization (swappable whisks + auto-speed presets tuned for oat/almond/soy)