PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063676

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063676

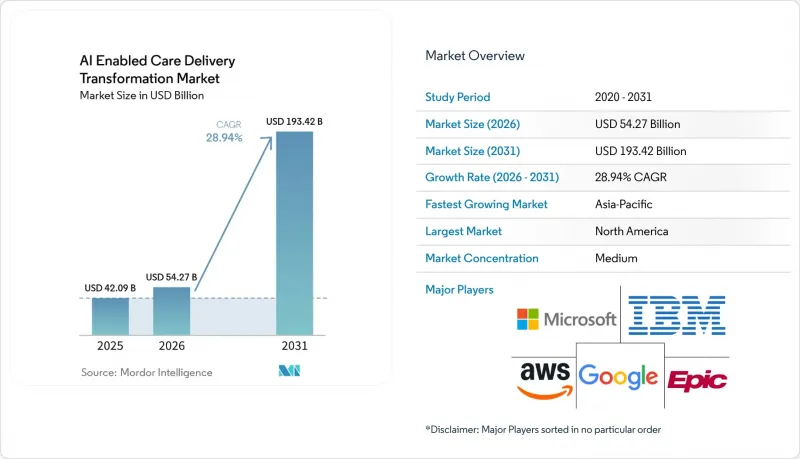

AI Enabled Care Delivery Transformation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the aI enabled care delivery transformation market size is expected to grow from USD 42.09 billion in 2025 to USD 54.27 billion in 2026 and is forecast to reach USD 193.42 billion by 2031 at 21.94% CAGR over 2026-2031.

This report is Segmented by Component (Software, Services, and Platforms / AI Models), Application (Clinical Decision Support, Patient Engagement & Virtual Care, and More), Deployment (Cloud-Based, On-Premise, and Hybrid), End User (Hospitals & Health Systems, Ambulatory Care Centers, and More), and Geography (North America, Europe, and More). The Market and Forecasted in Terms of Value (USD).

Global AI Enabled Care Delivery Transformation Market Trends and Insights

Rising AI Adoption in Clinical Workflows

Ambient documentation tools reached 68% U.S. hospital adoption in 2025, a 62% year-on-year increase that addresses physician burnout as much as efficiency. Microsoft's DAX Copilot, deployed across Epic sites, processes in excess of 1 million encounters per month and trims visit documentation by roughly five minutes, allowing each clinician to see two more patients daily. Hospitals that scale ambient AI report an 18% reduction in voluntary clinician turnover, recouping subscription costs within 14 months. Clinical-documentation-improvement platforms reached 43% penetration in 2025, propelled by Medicare Severity-Diagnosis-Related Group optimization, which lifts case-mix index scores and reimbursement. The FDA's Good AI Practice principles, published in January 2026, outline ten lifecycle tenets that give vendors regulatory clarity as they branch into diagnostic and therapeutic domains.

Growing Need to Reduce Healthcare Cost & Operational Burden

Administrative automation delivered USD 258 billion in cost savings for U.S. providers in 2024, with revenue-cycle management and prior authorization representing 64% of that value. Persistent wage inflation averaging 5.3% annually from 2022 to 2025 widens the ROI gap between human labor and algorithmic tools. A 2025 National Bureau of Economic Research study projected full-scale AI deployment could unlock USD 200-360 billion in annual savings by automating 40-60% of billing, scheduling, and utilization-review tasks. CMS guidance released in August 2025 formally allowed automated approvals for low-complexity prior-authorization requests, accelerating natural-language-processing investment. Implementation paybacks materialize within six to nine months, half the horizon typical for clinical decision support, making administrative use cases the near-term growth engine.

Data Privacy, Security & Evolving Regulations

The European Union's AI Act, effective August 2024 with phased enforcement in 2025, designates most clinical decision aids as high-risk, compelling conformity assessments, third-party audits, and post-market surveillance that extend commercialization by 9-12 months. GDPR further restricts automated outputs that create "legal or similarly significant effects" without human review, reducing efficiency gains by forcing manual checkpoints. Breach incidents involving protected health information rose 32% in 2025, heightening executive hesitation to move sensitive workloads to cloud platforms despite superior AI capacity. The FDA's August 2025 Change-Control guidance lets sponsors pre-define algorithm updates, trimming supplemental filings, but it does not override international data-localization laws that fragment training corpora. Until harmonization emerges, compliance drag will temper near-term growth, particularly for vendors aiming at multinational rollouts.

Other drivers and restraints analyzed in the detailed report include:

- Explosion of Healthcare Data

- Shift toward Value-Based & Personalized Care Models

- Integration & Workflow Adoption Challenges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software solutions commanded 52.68% of the AI enabled care delivery transformation market share in 2025, yet modular AI platforms are accelerating at a 22.71% CAGR through 2031 as providers favor configurable building blocks over bespoke code. The AI enabled care delivery transformation market size for platform offerings is projected to expand rapidly as Google's Med-PaLM 2 and Microsoft's Azure Health Data Services enable institution-level fine-tuning in days rather than quarters. Cloud vendors bundle pre-trained language and vision models that shorten validation cycles and lower capital intensity. Services revenue implementation, training, and managed analytics rise in tandem because many health systems lack in-house data-science capacity.

The December 2025 HTI-5 Rule codified FHIR interoperability, allowing vendors to "build once, deploy anywhere," which amplifies component reuse and tilts momentum toward platform ecosystems. NVIDIA's 2025 healthcare-optimized GPUs reduced inference latency for imaging models by 40%, making specialized hardware an infrastructure prerequisite for real-time use cases. The FDA's Good AI Practice guidance endorses modular pipelines that isolate preprocessing from inference, letting sponsors update sub-components without re-validation a stance that inherently privileges platform architectures over monoliths.

Administrative and workflow automation recorded the fastest expansion, advancing at a 24.61% CAGR thanks to near-term payback and quantifiable dollar savings. Revenue-cycle use cases alone represent USD 165 billion in annual spending, and AI-based prior-authorization engines cut approval time from 3.2 to 1.1 days in 2025. The CMS August 2025 memo permitting automated low-complexity approvals removed a regulatory choke point, unlocking payer/provider procurement cycles.

Clinical decision support still held a 32.46% revenue share because quality-metric improvement under value-based reimbursement preserves top-line revenue. Sepsis early-warning systems, for example, reduce mortality 15-20% when coupled with rapid-response workflows, avoiding costly ICU admissions. Patient engagement and virtual-care tools gained traction as 30 million remote monitoring devices streamed physiologic data into AI triage pipelines in 2025. Remote monitoring now consolidates around chronic-disease management, where near-real-time parameter feeds let algorithms titrate medications before decompensation.

Geography Analysis

North America generated 36.46% of 2025 revenue, underpinned by CMS reimbursement programs that reward AI-driven quality gains and offset labor shortages exacerbated by 5.3% annual wage inflation. The December 2025 HTI-5 Rule mandates decision-support transparency and FHIR APIs, lowering interoperability costs unique to the region. Canada's single-payer systems deploy AI for wait-time optimization, while Mexico's private-hospital chains bundle AI decision support into cloud EHR subscriptions for urban populations.

Asia-Pacific is the fastest-growing region at a 25.48% CAGR. China's National Healthcare Security Administration processed over 200 million AI-assisted prior-authorization claims per month in 2025, slashing approval times 60%. India's Ayushman Bharat Digital Mission is integrating smartphone-based AI screening for tuberculosis and diabetic retinopathy to reach rural districts. Japan's aging society fuels remote monitoring demand, while Australia's Therapeutic Goods Administration harmonized device review processes with the FDA in 2025, easing foreign market entry. South Korea earmarked USD 2 billion for precision-oncology AI through 2025 grants.

Europe grows more slowly because the AI Act adds 9-12 months to commercialization timelines, although the European Health Data Space promises to unlock federated learning once member states align governance. Germany pilots AI-supported diabetes programs that integrate wearable feeds with EHRs, and the U.K.'s NHS deployed AI radiology tools across 200 hospitals in 2025 to ease clinician shortages. Middle East & Africa benefit from Gulf sovereign-wealth investment: Saudi Arabia's Vision 2030 allocated USD 1.5 billion to AI smart-hospital projects in 2025. South America's ministries pilot epidemic-prediction algorithms, leveraging mobile-data telemetry to detect outbreaks faster than lab confirmations.

- Aidoc

- Amazon Web Services (AWS)

- athenahealth

- Babylon Health

- eClinicalWorks

- Epic Systems

- GE Healthcare

- Google (Alphabet)

- Health Catalyst

- IBM

- Meditech

- Microsoft

- NextGen Healthcare

- NVIDIA

- Oracle Health (Cerner)

- Koninklijke Philips

- SAS Institute

- Siemens Healthineers

- Tempus

- Viz.ai

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising AI Adoption in Clinical Workflows

- 4.2.2 Growing Need to Reduce Healthcare Cost & Operational Burden

- 4.2.3 Explosion of Healthcare Data

- 4.2.4 Shift toward Value-Based & Personalized Care Models

- 4.2.5 Synthetic Data & Federated Learning Enabling Privacy-Preserving AI

- 4.2.6 Emergence of Modular AI Micro-Services for Plug-And-Play EHR integration

- 4.3 Market Restraints

- 4.3.1 Data Privacy, Security & Evolving Regulations

- 4.3.2 Integration & Workflow Adoption Challenges

- 4.3.3 Model-Drift Risk Requiring Continuous Clinical Validation

- 4.3.4 Rising AI Compute Carbon Footprint Conflicting with ESG Goals

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.1.3 Platforms / AI Models

- 5.2 By Application

- 5.2.1 Clinical Decision Support

- 5.2.2 Patient Engagement & Virtual Care

- 5.2.3 Administrative & Workflow Automation

- 5.2.4 Remote Monitoring / Telehealth

- 5.2.5 Others

- 5.3 By Deployment

- 5.3.1 Cloud-based

- 5.3.2 On-premise

- 5.3.3 Hybrid

- 5.4 By End User

- 5.4.1 Hospitals & Health Systems

- 5.4.2 Ambulatory Care Centers

- 5.4.3 Digital Health Providers

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 Aidoc

- 6.3.2 Amazon Web Services (AWS)

- 6.3.3 athenahealth

- 6.3.4 Babylon Health

- 6.3.5 eClinicalWorks

- 6.3.6 Epic Systems

- 6.3.7 GE HealthCare

- 6.3.8 Google (Alphabet)

- 6.3.9 Health Catalyst

- 6.3.10 IBM

- 6.3.11 MEDITECH

- 6.3.12 Microsoft

- 6.3.13 NextGen Healthcare

- 6.3.14 NVIDIA

- 6.3.15 Oracle Health (Cerner)

- 6.3.16 Philips Healthcare

- 6.3.17 SAS Institute

- 6.3.18 Siemens Healthineers

- 6.3.19 Tempus

- 6.3.20 Viz.ai

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment