PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063678

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063678

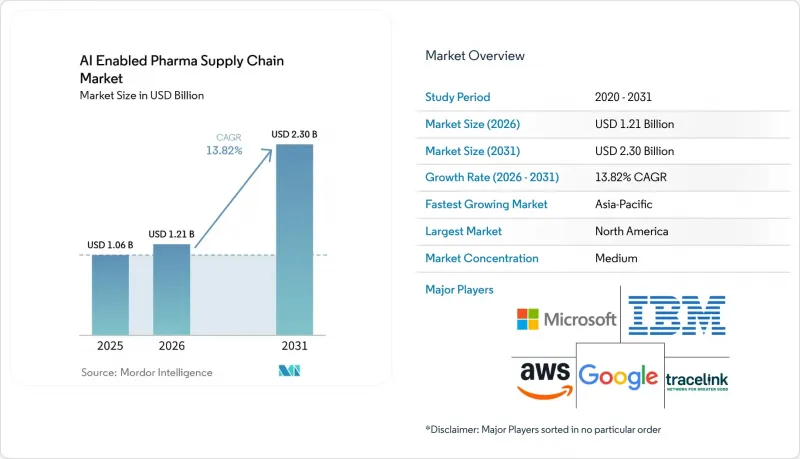

AI Enabled Pharma Supply Chain - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the aI enabled pharma supply chain market size is projected to expand from USD 1.06 billion in 2025 and USD 1.21 billion in 2026 to USD 2.30 billion by 2031, registering a CAGR of 13.82% between 2026 to 2031.

This report is Segmented by Component (Software, Services, and Platforms / AI Models), Application (Demand Forecasting & Planning, Logistics & Distribution Management, and More), Deployment (Cloud-Based, and More), End-User (Pharmaceutical Companies, Biotechnology Companies, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market and Forecasted in Terms of Value (USD).

Global AI Enabled Pharma Supply Chain Market Trends and Insights

Rising Demand for Predictive Supply-Chain Management

Pharmaceutical companies are replacing monthly planning cycles with always-on engines that forecast demand 18 months ahead, blending clinical-trial enrollment signals, payer formulary updates, and weather data. Merck's five-year, USD 1 billion Vertex AI rollout aims to trim safety stock 30%, freeing cash for pipeline acquisitions. An extra percentage point of inventory ties up USD 200-300 million in working capital at a top-20 firm, so precision matters. AI-driven forecast accuracy gains of 15-25 points unlock USD 3-5 billion that can fund dividend increases. The January 2026 FDA-EMA principles clarified documentation expectations, giving quality teams the legal cover to automate replenishment workflows. Early adopters already report 8-10 day lead-time reductions, improving service levels for temperature-sensitive oncology drugs.

Growing Complexity of Global Pharmaceutical Distribution Networks

China-plus-one strategies now split active-ingredient sourcing across India, Vietnam, and Mexico, forcing brand owners to manage more suppliers. IBM Watsonx tracks 2.3 million pharmaceutical SKUs in 87 countries and flags export-license delays or port congestion 14 days early, letting firms switch to pre-qualified alternates. India's 1,300+ global capability centers feed region-specific demand models that surface opaque distributor sales data. Brazil and Argentina CMOs employ AI procurement engines to hedge currency swings that shift input costs 20% within a quarter. As logistics corridors stretch, visibility gaps amplify risk; predictive ETA tools that combine real-time vessel traffic with customs filings improve schedule adherence by 11-15%. These shifts raise the baseline need for the AI enabled pharma supply chain market to deliver end-to-end transparency across fragmented geographies.

High Implementation Cost and Integration Complexity

Mid-tier companies with USD 500 million-USD 3 billion in revenue run IT budgets near 3% of revenue, yet full AI platform rollouts can cost USD 15-25 million. TraceLink's 2026 survey reported 68% of executives view integration as the primary barrier, because each API interface needs 400-600 engineering hours and GMP validation that drags go-live by nine months. CMOs with net margins below 12% often defer AI until vendors offer modular "start small" kits focused on one high-impact use case, such as demand sensing. Legacy ERP instances from the 1990s complicate matters with customized code that resists modern REST connectors. Capital budgeting committees demand payback within 24 months, forcing suppliers to provide outcome-based pricing. These realities temper near-term spending, although as more reference sites emerge, perceived risk declines and the AI enabled pharma supply chain industry broadens adoption.

Other drivers and restraints analyzed in the detailed report include:

- Need for Cost Optimization and Operational Efficiency

- Rapid Digitalization of Pharma Operations

- Data Privacy, Compliance and Regulatory Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Platforms and AI models will grow at 14.71% CAGR through 2031, outpacing every other component. Software captured 63.45% share in 2025 because of the entrenched installed base. Blue Yonder added autonomous agents in 2026 that already manage inventory across 37 distribution centers.

NVIDIA-backed GPU simulation lets Kinaxis model 10,000 disruption scenarios in two hours. Demand for explainable AI that passes EU AI Act transparency tests is driving upgrades away from black-box rules engines. Services revenues are rising at the broader AI enabled pharma supply chain market growth rate because drug makers outsource model tuning on validated infrastructure.

Cold-chain monitoring is forecast to post 15.69% CAGR through 2031 as gene and cell-therapy launches triple ultra-cold shipments. Demand-forecasting retained 32.48% of the AI enabled pharma supply chain market share in 2025, though its growth is plateauing. Edge sensors now feed 10-second interval data to predictive models that cut equipment downtime 30% and extend chiller life by two years.

Risk-and-disruption engines are graduating from pilot to production, ingesting 340,000 fresh data points daily to score supplier vulnerabilities. Logistics optimization saves 18-25% in expedited freight by forecasting delivery windows within 15 minutes. These cascading use cases ensure the AI enabled pharma supply chain market continues widening its application stack in response to real-world shocks.

Geography Analysis

North America commanded 38.51% of global revenue in 2025, reflecting early mover deployments and the January 2026 FDA-EMA principles that clarified AI validation. Merck's USD 1 billion Vertex AI roll-out and McKesson's IBM WatsonX demand engine, which improved forecast accuracy to 92% and cut stock-outs 35%, exemplify the region's scale. Canada uses AI to balance provincial formulary nuances, while Mexican CMOs employ AI quality tools to strengthen nearshore supply for U.S. brands.

Asia-Pacific is projected to grow at 18.25% CAGR, outstripping every other region. India's 1,300+ global capability centers funnel AI talent into the AI enabled pharma supply chain market, helping exporters satisfy 54 diverse serialization regimes. China-plus-one diversification pushes API work to Vietnam and Indonesia, compelling real-time visibility platforms where 40% of tier-2 vendors still use spreadsheets. Japan's on-premise mandates channel spending into sovereign data centers, while Australia's AI-assisted regulatory pilots shorten approval cycles to nine months

Annex 22 and GDPR localization add USD 3-6 million per roll-out, incentivizing explainable on-premise solutions. Germany, the United Kingdom, France, Italy, and Spain control 65% of regional pharmaceutical output, and manufacturers there are pilot-testing agentic replenishment within tightly validated sandboxes. The Middle East, spearheaded by Saudi and UAE localization programs, and South America, driven by Brazil's e-prescribing mandate, round out emerging catch-up markets.

- Accenture

- Amazon Web Services (AWS)

- Blue Yonder

- Cognizant

- Coupa Software / Llamasoft

- DHL Supply Chain

- Google Cloud

- IBM

- Infor

- Kinaxis

- Manhattan Associates

- Microsoft

- NVIDIA

- O9 Solutions

- OPTEL Group

- Oracle

- SAP

- SAS Institute

- TraceLink

- Zebra Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Predictive Supply-Chain Management

- 4.2.2 Growing Complexity of Global Pharmaceutical Distribution Networks

- 4.2.3 Need for Cost Optimization and Operational Efficiency

- 4.2.4 Rapid Digitalization of Pharma Operations

- 4.2.5 AI-Driven Sustainability Mandates

- 4.2.6 Oncology Cold-Chain Precision via Edge-AI Sensors

- 4.3 Market Restraints

- 4.3.1 High Implementation Cost and Integration Complexity

- 4.3.2 Data Privacy, Compliance and Regulatory Constraints

- 4.3.3 Scarcity of Annotated GMP-Grade Supply-Chain Datasets

- 4.3.4 Model Drift Risk Amid Volatile Demand Shocks

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.1.3 Platforms / AI Models

- 5.2 By Application

- 5.2.1 Demand Forecasting & Planning

- 5.2.2 Logistics & Distribution Management

- 5.2.3 Cold-Chain Monitoring

- 5.2.4 Risk & Disruption Management

- 5.2.5 Others

- 5.3 By Deployment

- 5.3.1 Cloud-based

- 5.3.2 On-premise

- 5.3.3 Hybrid

- 5.4 By End-User

- 5.4.1 Pharmaceutical Companies

- 5.4.2 Biotechnology Companies

- 5.4.3 Contract Manufacturing Organizations (CMOs)

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 Accenture

- 6.3.2 Amazon Web Services (AWS)

- 6.3.3 Blue Yonder

- 6.3.4 Cognizant

- 6.3.5 Coupa Software / Llamasoft

- 6.3.6 DHL Supply Chain

- 6.3.7 Google Cloud

- 6.3.8 IBM

- 6.3.9 Infor

- 6.3.10 Kinaxis

- 6.3.11 Manhattan Associates

- 6.3.12 Microsoft

- 6.3.13 NVIDIA

- 6.3.14 O9 Solutions

- 6.3.15 OPTEL Group

- 6.3.16 Oracle

- 6.3.17 SAP SE

- 6.3.18 SAS Institute

- 6.3.19 TraceLink

- 6.3.20 Zebra Technologies

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment