PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063700

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063700

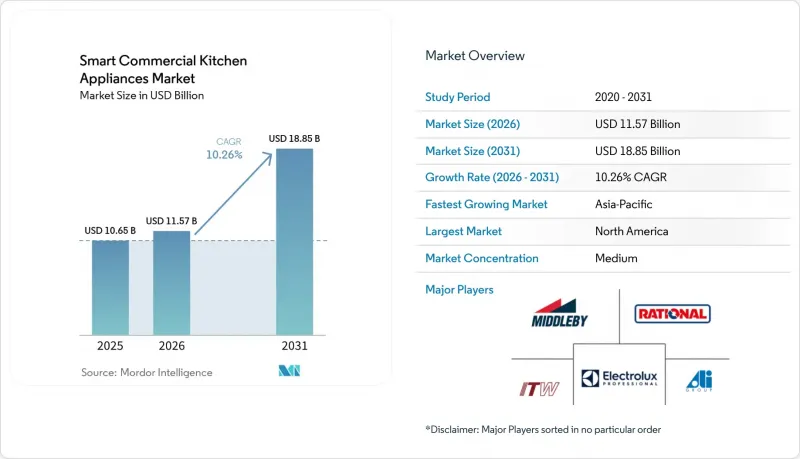

Smart Commercial Kitchen Appliances - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the smart commercial kitchen appliances market size was valued at USD 10.65 billion in 2025 and estimated to grow from USD 11.57 billion in 2026 to reach USD 18.85 billion by 2031, at a CAGR of 10.26% during the forecast period (2026-2031).

This report is Segmented by Product Type (Smart Cooking, Smart Refrigeration, Smart Warewashing, Smart Beverage), Installation Type (Countertop, Floor-Standing, Built-In), End-User (QSR Chains, Full-Service, Cafes/Bakeries, Hotels, Institutional, Others), Distribution Channel (Direct OEM, Dealers/Distributors), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Smart Commercial Kitchen Appliances Market Trends and Insights

Labor Shortages Push Automation and Connected Equipment ROI

Persistent staffing gaps and wage inflation have made automation financially viable in many kitchens, which strengthens adoption across the Smart Commercial Kitchen Appliances market as operators seek predictable output and lower on-the-line labor exposure. Robotic fry stations, AI-enabled makelines, and connected prep systems deliver measurable benefits by increasing throughput, reducing rework, and minimizing safety incidents during peak service windows. Deployed systems that automate repetitive, high-heat tasks show clear reductions in injuries and oil waste while stabilizing food quality at scale for chains with uniform menus. Automation of oil handling and filtration, paired with digital verification, also helps operators qualify for premium credits because it lowers the risk profile for burns and spills. The technology's second-order effect is labor redeployment: servers handling 40% more tables with Bear Robotics' Servi bots report 12% higher guest satisfaction, transforming headcount debates into service-quality arbitrage.

Energy Efficiency Mandates and Utility Costs Accelerate Smart Retrofits

The United States Department of Energy commercial refrigeration standards (effective January 2029, compliance deadline extended from 2025) will tighten maximum daily energy consumption limits by 6.5% versus current baselines, with projected cumulative savings of 1.11 quadrillion BTUs through 2058. Platforms that integrate sensors, edge logic, and centralized dashboards help sites reduce total energy use while improving compliance with equipment-level limits and audit requirements. Operators that coordinate startup sequences and schedule high-load processes outside billing peaks cut demand charges without sacrificing speed of service or food safety when capacity constraints are tight. Participation in demand-response programs creates a new incentive layer for connected electric kitchens, since kitchens can pre-cool or pre-heat and then coast during events with minimal guest impact. Integrated demand-response solutions both streamline enrollment and automate response at the device level, which reduces operational friction for multi-unit chains.

High Upfront Capex and Retrofit Complexity

Initial equipment purchases and site modifications create budget friction for smaller operators and independents, especially when floor plans must be reconfigured for robotics or higher-capacity electric loads in the smart commercial kitchen appliances market. Payback periods can stretch when deployment requires cabinetry changes, ventilation modifications, or panel upgrades to meet code and handle new duty cycles. Subscription and Robotics-as-a-Service models help some operators shift these investments into operating expense, but total cost of ownership still depends on maintenance diligence and training consistency. Older facilities face electrical capacity constraints when moving to induction or higher-wattage equipment, and integrating sensors with legacy HVAC or fire systems often requires custom gateways that add time and cost. Where building systems do not support modern protocols, BACnet or Modbus bridges can close gaps, but they introduce added complexity and require careful change control.

Other drivers and restraints analyzed in the detailed report include:

- Digital HACCP and Food Safety Compliance Standardize Connected Equipment

- Chain Standardization and Multi-Site Remote Fleet Control

- Interoperability and Standards Fragmentation Across Brands/Platforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Smart cooking appliances captured 38.91% of 2025 Smart Commercial Kitchen Appliances market share, led by connected combi ovens, smart fryers with oil-management sensors, and induction solutions that meet electrification goals without sacrificing speed. The segment's role evolves from reactive monitoring toward predictive automation as equipment self-adjusts to load variability and supports centralized recipe control across fleets. Fry stations that pair filtration with digital verification reduce waste and elevate consistency, while connected multi-cookers enable remote firmware updates that keep HACCP features aligned with changing standards. Refrigeration appliances are navigating refrigerant rules that phase out high-GWP gases, which accelerates transitions to A2L and R-290 systems and promotes supervisory controls that protect inventory with continuous temperature tracking. Smart warewashing adds automated logging and consumption optimization, with new models integrating connected assistants that support HACCP and energy alerts.

Smart beverage appliances will be the fastest-growing category at a 10.45% CAGR, as cafes and bakery chains standardize barista-quality output with bean-to-cup systems that lift peak-hour throughput and reduce training demands. Documented performance from commercial bean-to-cup systems shows large gains in drinks per hour and tight variance control that keeps quality consistent across shifts and sites. OEMs are extending data layers into beverage dispense for waste reduction and automated quality checks, which both improves margins and sustains guest experience at high transaction volumes. Refrigeration and display case connectivity aligns with food-safety logging mandates and helps reduce spoilage losses in smaller formats where a single failure can disrupt daily sales. The Smart Commercial Kitchen Appliances market continues to benefit where beverage, refrigeration, and warewashing modules operate on unified platforms that offer single-pane monitoring and push-based updates.

Floor-standing and back-of-house systems held a 56.46% share in 2025 within the Smart Commercial Kitchen Appliances market, reflecting long-standing adoption in full-service and institutional kitchens with higher-capacity needs. Large combi ovens, blast chillers, and walk-in refrigeration remain anchors for batch-based production and banquet output, and their connectivity brings recipe control, HACCP automation, and remote diagnostics across fleets. Compact countertop units, however, are forecast to grow the fastest at a 10.83% CAGR, as ghost kitchens, forecourts, and convenience operators invest in space-efficient, ventless tools that install quickly and scale modularly. AI-vision combi ovens and modular, multi-technology platforms pack more cooking types into smaller footprints, while leasing models reduce the barrier to trial for new locations.

As digital ordering concentrates transactions during peaks, compact ventless systems help maintain service times in sites that cannot support full kitchen retrofits, and they integrate cleanly into unified dashboards for staff who rotate tasks. Efficiency standards tighten in coming years and reward smaller cavities and smarter control logic, so compact systems that coordinate with building management save energy while preserving output. For beverage and front-of-house applications, high-flow dispense controls and accurate mixture management improve speed and product quality while lowering wastage, which compounds returns in small formats. The Smart Commercial Kitchen Appliances market benefits where these compact systems integrate natively with enterprise platforms for recipe pushes and firmware updates that maintain compliance and consistency over time.

Geography Analysis

North America accounted for 32.73% of the Smart Commercial Kitchen Appliances market size in 2025, supported by large chain penetration, tighter food-safety oversight, and strong vendor ecosystems for connected kitchens. Wage pressures in key states since 2024 have further sharpened the case for automation as chains look to protect margins with predictive systems and safer, standardized workflows. Regulatory tailwinds shape purchase timing, with the region preparing for DOE efficiency compliance cycles and EPA refrigerant restrictions on high-GWP gases in new and retrofit contexts. Utilities reinforce adoption with demand-response programs that pay for load shed during events, and purpose-built solutions integrate directly into OEM platforms so multi-unit chains can monetize flexibility without adding operational risk. Canada and Mexico expand through cafe, bakery, and convenience formats that value compact connected units and IoT oversight across refrigeration, cooking, and warewashing workflows.

Asia-Pacific is projected to post the highest growth at an 11.63% CAGR, led by markets where demographic constraints and government programs push toward robotics and digital oversight. Japan continues to deploy service robots at scale in full-service and family-dining formats, which supports higher throughput and improves safety without adding back-of-house headcount. China expands investment in cloud kitchens and connected prep lines, moving toward consistent, high-volume output under software-driven coordination with centralized data layers. South Korea and India diversify demand, while Southeast Asian markets like Singapore adopt continuous monitoring for HACCP and leverage open-interface platforms to connect multi-brand fleets in small footprints. Documented Asia-Pacific deployments show large reductions in equipment failure incidence and faster repair cycles when fleets are brought under unified IoT control with edge computing for local failover.

Europe grows at a moderate pace due to high baseline automation in key countries, but evolving food-safety practices and energy standards still support replacement cycles that favor connected systems. Germany sets the tone in premium connected combi ovens and remote-fleet control, with OEM platforms that push standardized recipes, log HACCP data, and reduce on-site maintenance. OEMs in the region also integrate sustainability into manufacturing and product design, including use of low-GWP refrigerants and renewable-energy operations, which aligns with buyer priorities in public and private tenders. South America sees steady adoption in hospitality hubs, while the Middle East and Africa add capacity through hotel and food-court expansions that pair connected cooking with centralized monitoring to maintain standards at scale. Across regions, the Smart Commercial Kitchen Appliances market advances where local rebate programs, building-code changes, and data-protection regimes converge with chain strategies for standardized execution and compliance.

List of Companies Covered in this Report:

- The Middleby Corporation

- Ali Group

- ITW Food Equipment Group

- Electrolux Professional AB

- Welbilt Inc.

- Hoshizaki Corporation

- Rational AG

- Hobart Corporation

- True Manufacturing Co.

- Meiko Maschinenbau GmbH

- Winterhalter Gastronom GmbH

- Duke Manufacturing

- Alto-Shaam Inc.

- Manitowoc Ice

- Franke Coffee Systems

- Epta S.p.A.

- Fagor Industrial

- Turbo Air Inc.

- Carrier Commercial Refrigeration

- Vollrath Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Labor shortages push automation and connected equipment ROI

- 4.2.2 Energy efficiency mandates and utility costs accelerate smart retrofits

- 4.2.3 Digital HACCP and food safety compliance standardize connected equipment

- 4.2.4 Chain standardization and multi-site remote fleet control

- 4.2.5 Demand-response and grid incentives for connected electric kitchens

- 4.2.6 Insurance and compliance credits for IoT-verified operations

- 4.3 Market Restraints

- 4.3.1 High upfront capex and retrofit complexity

- 4.3.2 Interoperability and standards fragmentation across brands/platforms

- 4.3.3 Cybersecurity, data ownership, and IT integration risks

- 4.3.4 Electrical capacity constraints in older sites limit electrification

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Industry Rivalry

- 4.6 Insights Into The Latest Trends And Innovations in the Industry

- 4.7 Insights On Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, Etc.) In The Industry

- 4.8 Insights on Regulatory Framework and Energy-Efficiency Standards in Key Geographies

5 Market Size & Growth Forecasts (Value in USD Billion)

- 5.1 By Product Type

- 5.1.1 Smart Cooking Appliances

- 5.1.1.1 Smart Ovens (combi ovens, convection ovens etc)

- 5.1.1.2 Smart Air Fryers and Fryers (Open/Pressure; smart oil management)

- 5.1.1.3 Multi-Cookers & Multifunctional Cookers

- 5.1.1.4 Smart Grills/Griddles/Induction Hobs

- 5.1.1.5 Smart Ranges & Cooktops

- 5.1.1.6 Others (Steamers & Sous-vide/Precision Cookers)

- 5.1.2 Smart Refrigeration Appliances (Commercial Refrigerators and Freezers)

- 5.1.3 Smart Warewashing Appliances

- 5.1.4 Smart Beverage Appliances (Coffee/Espresso; Tea Brewers; Dispensers)

- 5.1.1 Smart Cooking Appliances

- 5.2 By Installation Type

- 5.2.1 Countertop/Compact

- 5.2.2 Floor-standing/Back-of-house

- 5.2.3 Built-in/Backbar/Front-of-house

- 5.3 By End-User

- 5.3.1 QSR & Fast Casual Chains

- 5.3.2 Full-Service Restaurants

- 5.3.3 Cafes/Bakeries & Coffee Chains

- 5.3.4 Hotels & Resorts

- 5.3.5 Institutional (Education, Healthcare, Corporate)

- 5.3.6 Others (Ghost/Cloud Kitchens, Convenience Retail & Forecourt, Catering & Events)

- 5.4 By Distribution Channel

- 5.4.1 Direct OEM

- 5.4.2 Dealers/Distributors

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 India

- 5.5.4.2 China

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East And Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East And Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 The Middleby Corporation

- 6.4.2 Ali Group

- 6.4.3 ITW Food Equipment Group

- 6.4.4 Electrolux Professional AB

- 6.4.5 Welbilt Inc.

- 6.4.6 Hoshizaki Corporation

- 6.4.7 Rational AG

- 6.4.8 Hobart Corporation

- 6.4.9 True Manufacturing Co.

- 6.4.10 Meiko Maschinenbau GmbH

- 6.4.11 Winterhalter Gastronom GmbH

- 6.4.12 Duke Manufacturing

- 6.4.13 Alto-Shaam Inc.

- 6.4.14 Manitowoc Ice

- 6.4.15 Franke Coffee Systems

- 6.4.16 Epta S.p.A.

- 6.4.17 Fagor Industrial

- 6.4.18 Turbo Air Inc.

- 6.4.19 Carrier Commercial Refrigeration

- 6.4.20 Vollrath Company

7 Market Opportunities & Future Outlook

- 7.1 Utility-integrated demand response and electrification programs for connected kitchen fleets (tariff arbitrage, load shedding)

- 7.2 InsurTech partnerships to monetize IoT-verified compliance, reducing premiums and financing costs for independents