PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063719

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063719

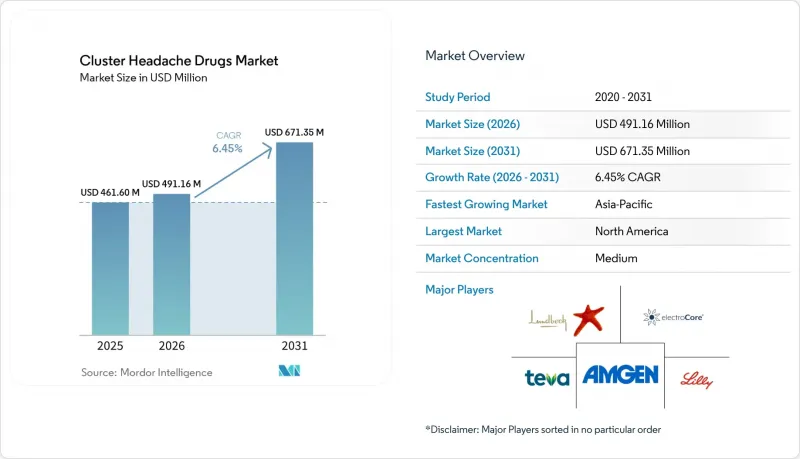

Cluster Headache Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the cluster headache drugs market size is projected to be USD 461.60 million in 2025, USD 491.16 million in 2026, and reach USD 671.35 million by 2031, growing at a CAGR of 6.45% from 2026 to 2031.

This report is Segmented by Treatment Type (Acute Treatment, and More), Drug Class (Triptans, CGRP Monoclonal Antibodies, and More), Route of Administration (Oral, Injectable, Intranasal, and More), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and More), and Geography (North America, Europe, Asia Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Cluster Headache Drugs Market Trends and Insights

Growing Diagnosed Patient Pool

Earlier recognition of trigeminal-autonomic cephalalgias is shortening what historically was a multi-year wait for an accurate diagnosis. Intensified primary-care training and algorithm-based teleconsultations allow practitioners to flag hallmark unilateral pain patterns within months of onset. National headache registries report a steady rise in newly coded cluster headache cases, particularly in rural U.S. counties where tele-neurology platforms have replaced sporadic outreach clinics. The financial case for aggressive case-finding is compelling. Every undiagnosed patient incurs more than USD 11,000 in direct and indirect annual costs, driving payers to fund awareness campaigns and expedited referral pathways. Asia-Pacific health systems are adopting similar protocols, contributing to double-digit growth in patient identification across China and India.

Expansion of Targeted Biologics Pipelines

CGRP monoclonal antibodies such as galcanezumab have demonstrated a median 52% reduction in weekly attack frequency, setting a new efficacy benchmark for episodic cluster headache prevention. Late-stage assets targeting pituitary adenylate cyclase-activating peptide (PACAP-38) and ATP-sensitive potassium channels promise additional disease-modifying options. Amgen's Phase II PAC1 antagonist (AMG 301) has entered multi-center dosing studies with interim results anticipated in 2026, while pre-clinical Kir6.1 modulators are showing favorable blood-brain-barrier penetration profiles. Patent estates that extend beyond 2035 are fueling venture capital inflows and cross-licensing deals, reinforcing a virtuous cycle of pipeline innovation.

High Treatment Costs & Affordability Hurdles

Average annual acquisition costs for a CGRP inhibitor hover at USD 6,900 and remain beyond reach for many uninsured or under-insured patients. Less than half of large U.S. payers cover all approved CGRP products, and 64% impose prior-authorization steps that can delay therapy initiation by several weeks. Disparities widen in low-income markets, where retail prices mirror U.S. list prices but household health budgets are a fraction of OECD averages. Orphan drug pricing inflates budget-impact models; median annual spend for rare-disease therapies exceeds USD 200,000, straining national formularies. These cost headwinds slow uptake, particularly in cash-pay segments of Southeast Asia and parts of Latin America, thereby tempering topline market growth.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advances in Delivery & Neuromodulation

- Growth of Specialized Clinics & Telehealth

- Specialist Shortages & Diagnostic Delays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Preventive regimens generated 38.3% of 2025 revenue but are set to rise fastest at 19.3% CAGR through 2031. Galcanezumab's ability to cut episodic attack frequency by more than half has repositioned prophylaxis as the standard of care for patients with predictable cyclical bouts. Pay-for-performance contracts signed in 2025 between two large U.S. pharmacy-benefit managers and CGRP manufacturers link reimbursement to real-world reductions in emergency-department visits. Acute interventions remain vital, capturing 61.7% share of the cluster headache drugs market size in 2024, supported by reliable agents such as high-flow oxygen and subcutaneous triptans. Innovations like the Brekiya autoinjector are sustaining acute segment relevance by reducing injection anxiety and streamlining at-home administration. Clinicians now employ hybrid protocols that combine an acute self-rescue plan with maintenance CGRP dosing, improving health-related productivity and diminishing overall cost of care.

CGRP monoclonal antibodies led the drug-class hierarchy with 30.4% of the cluster headache drug market share in 2025 and maintain the highest expansion rate at 23.5% CAGR. Three agents galcanezumab, fremanezumab, and erenumab have captured prescriber confidence due to sustained efficacy and monthly subcutaneous dosing convenience. Triptans, available in generic form, keep a firm footing for rapid pain abortive use but add minimal incremental growth. Ergot alkaloids, revitalized by autoinjector technology, serve niche patient cohorts who respond poorly to triptans. Looking forward, PACAP and KATP modulators could diversify the preventive portfolio; their differentiated mechanisms may extend therapeutic benefit to antibody non-responders.

Geography Analysis

North America anchors nearly 48% of global revenue, driven by early biologic adoption, broad insurance coverage, and dense networks of academic headache centers. Legislative changes in 2025 that mandate equal reimbursement for telehealth visits in 42 states have lowered rural access disparities, yet clinician shortages persist west of the Mississippi River. U.S. payers are experimenting with indication-based pricing that ties CGRP payment levels to patient response, laying the groundwork for outcome-based agreements across other drug classes. Canada benefits from centralized price negotiations; identical CGRP injectors cost 32% less than the U.S. average, encouraging faster uptake among publicly funded provincial plans.

Europe represents a mature but heterogeneous landscape. Germany and Scandinavia reimburse all three licensed CGRP antibodies with minimal step-therapy requirements, whereas Central- and Eastern-European markets impose stricter budget caps that hamper adoption. Health-technology-assessment agencies in France and Italy approved Fremanezumab in late 2024 after real-world evidence showed 1.7 fewer emergency-room visits per month among continuous users. Spain's cost-effectiveness committee placed erenumab well below its EUR 30,000 (USD 35,243) threshold, propelling prescriber confidence and widening patient access. The European Commission's push for cross-border telemedicine services is expected to alleviate specialist shortages in peripheral regions by 2027.

Asia-Pacific is the fastest-growing territory, rising at a 10.9% CAGR. China's National Medical Products Administration cleared rimegepant in January 2025, marking the first CGRP receptor antagonist venue in the world's largest patient pool. Large urban hospitals in Shanghai and Beijing now include cluster headache pathways in their neurologic centers of excellence, accelerating diagnosis rates. Japan's April 2025 guideline update endorsed long-term anti-CGRP prophylaxis after a favorable two-year safety surveillance, further normalizing biologic use. Thailand and Indonesia are following suit through national formularies that earmark orphan-drug budgets for rare-headache indications, though reimbursement ceilings still limit uptake to tertiary-care hospitals.

- Eli Lilly and Company

- Amgen

- Novartis

- Teva Pharmaceutical Industries

- Lundbeck A/S

- Abbvie

- Pfizer

- Otsuka Pharma

- electroCore Inc.

- Zogenix Inc. (UCB)

- Impel NeuroPharma

- AstraZeneca

- Satsuma Pharma

- Johnson & Johnson

- Dr. Reddy's Laboratories

- Cipla

- Endo International

- WraSer Pharmaceuticals

- Hikma Pharmaceuticals

- Upsher-Smith Labs

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Diagnosed Patient Population Worldwide

- 4.2.2 Expansion Of Targeted Biologics and Novel Therapeutic Pipelines

- 4.2.3 Increasing Healthcare Expenditure and Orphan Drug Reimbursements

- 4.2.4 Technological Advancements in Drug Delivery and Neuromodulation

- 4.2.5 Proliferation of Specialized Headache Clinics and Telemedicine Services

- 4.2.6 Regulatory Incentives Accelerating Rare Disease Drug Approvals

- 4.3 Market Restraints

- 4.3.1 High Treatment Costs and Affordability Challenges

- 4.3.2 Limited Specialist Availability and Diagnostic Delays

- 4.3.3 Long Term Safety and Efficacy Uncertainties for Emerging Therapies

- 4.3.4 Supply Chain Constraints in Essential Acute Care Modalities

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, uSD)

- 5.1 By Treatment Type

- 5.1.1 Acute Treatment

- 5.1.2 Preventive Treatment

- 5.2 By Drug Class

- 5.2.1 Triptans

- 5.2.2 CGRP Monoclonal Antibodies

- 5.2.3 Ergot Alkaloids

- 5.2.4 Calcium-Channel Blockers (Verapamil)

- 5.2.5 Others

- 5.3 By Route of Administration

- 5.3.1 Oral

- 5.3.2 Injectable

- 5.3.3 Intranasal

- 5.3.4 Inhalation (Medical Oxygen)

- 5.3.5 Neuromodulation Device

- 5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 Online Pharmacies

- 5.4.4 Specialty Clinics

- 5.4.5 Home Healthcare Providers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Eli Lilly & Co.

- 6.3.2 Amgen Inc.

- 6.3.3 Novartis AG

- 6.3.4 Teva Pharmaceutical

- 6.3.5 Lundbeck A/S

- 6.3.6 AbbVie Inc.

- 6.3.7 Pfizer Inc.

- 6.3.8 Otsuka Pharma

- 6.3.9 electroCore Inc.

- 6.3.10 Zogenix Inc. (UCB)

- 6.3.11 Impel NeuroPharma

- 6.3.12 AstraZeneca plc

- 6.3.13 Satsuma Pharma

- 6.3.14 Johnson & Johnson (Janssen)

- 6.3.15 Dr. Reddy's Laboratories

- 6.3.16 Cipla Ltd.

- 6.3.17 Endo International

- 6.3.18 WraSer Pharmaceuticals

- 6.3.19 Hikma Pharmaceuticals

- 6.3.20 Upsher-Smith Labs

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment