PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063728

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063728

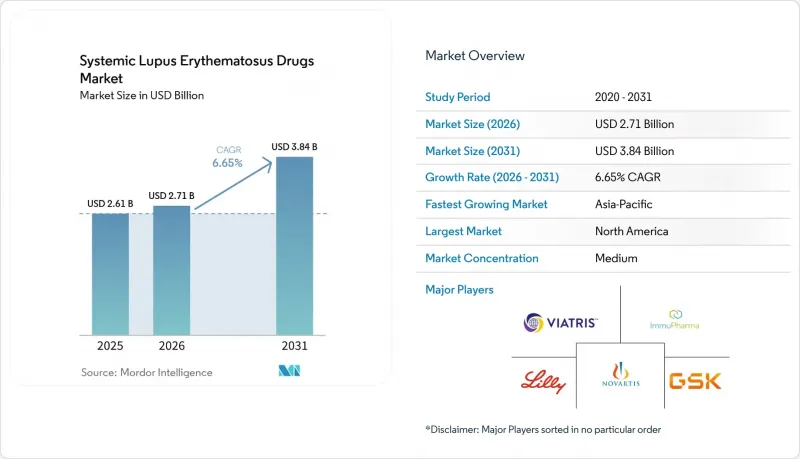

Systemic Lupus Erythematosus Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the systemic lupus erythematosus drugs market size is expected to increase from USD 2.61 billion in 2025 to USD 2.71 billion in 2026 and reach USD 3.84 billion by 2031, growing at a CAGR of 6.65% over 2026-2031.

This report is Segmented by Treatment Type (NSAIDs, Antimalarials, Corticosteroids, and More), Route of Administration (Oral, Intravenous, Subcutaneous), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Systemic Lupus Erythematosus Drugs Market Trends and Insights

Rising Prevalence and Earlier Diagnosis

Commercial biomarker panels detecting T-cell autoantibodies and cell-bound complement activation products (CB-CAPs) have moved lupus detection into an earlier therapeutic window. Medicare reimbursement of USD 840.65 per test for the AVISE panel in 2025 underscores payer support for molecular tools that enlarge the treatable cohort. Predictive assays like AMPEL's LuGENE enable clinicians to alter therapy before clinical deterioration, directly expanding demand for targeted treatments across the systemic lupus erythematosus drugs market.

Rapid Approvals of Novel Biologics

The FDA's acceptance of obinutuzumab's supplemental application for lupus nephritis with an October 2025 decision timeline exemplifies the agency's accelerated review posture. Phase III data showed a 46.4% complete renal response versus 33.1% for standard care, establishing a new benchmark. Parallel fast-track designations for allogeneic CAR-T candidates from Adicet Bio and Sana Biotechnology further highlight momentum, positioning next-generation modalities to reshape competitive dynamics within the systemic lupus erythematosus drugs market.

High Therapy Cost and Reimbursement Hurdles

Despite Medicare's USD 2,000 annual out-of-pocket cap for Part D in 2025, cumulative drug costs remain prohibitive for many patients. Payers demand real-world evidence and health-economic analyses before approving high-priced biologics, imposing step-therapy barriers that slow adoption. Biosimilar launches add marginal price pressure but have yet to meaningfully erode branded utilization in the systemic lupus erythematosus drugs market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Companion-Diagnostic Biomarkers

- Tele-Rheumatology Boosting Access

- Safety Concerns: Infection and Malignancy Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The systemic lupus erythematosus drugs market size for biologics translated to 36.02% of total sales in 2025. GSK's Benlysta maintained double-digit growth, buoyed by expanded indications and an autoinjector format approved in 2024. Stem-cell and gene-based therapies, though nascent, hold the fastest growth outlook at a 9.41% CAGR as curative intent resonates with payers and patients.

Multiple CAR-T assets secured fast-track or orphan-drug status in 2024-2025, reflecting regulator confidence and investor appetite. Immunosuppressants and DMARDs remain clinical mainstays that enable steroid tapering, yet guideline updates from the American College of Rheumatology prioritize steroid minimization, indirectly boosting biologic adoption. Manufacturing scale-up globally points to a durable rise in demand across the systemic lupus erythematosus drugs market.

Geography Analysis

North America generated 43.20% of systemic lupus erythematosus drugs market revenue in 2025, supported by comprehensive insurance coverage, robust clinical-trial infrastructure and rapid uptake of FDA-designated breakthrough therapies. Implementation of the USD 2,000 Part D out-of-pocket ceiling in 2025 further reduces access barriers, while value-based contracting aligns payer incentives with outcome improvements. Canada's evolving pan-Canadian Pharmaceutical Alliance negotiations shape pricing corridors, whereas Mexico's Seguro Popular reforms introduce incremental reimbursement headroom.

Asia-Pacific is advancing at a 8.72% CAGR, the highest regional trajectory in the systemic lupus erythematosus drugs market. Japan approved voclosporin (LUPKYNIS) for lupus nephritis in 2024, creating precedent for accelerated filings of novel agents. China's National Medical Products Administration adopted conditional approvals for domestic biologics such as telitacicept, while pilot reimbursement programs in Beijing and Shanghai subsidize targeted therapies. Australia listed anifrolumab on the Pharmaceutical Benefits Scheme in 2024, improving affordability and catalyzing market expansion. India and South Korea leverage expanding specialty-care networks and rising autoimmune-disease awareness to unlock latent demand.

Europe remains pivotal, anchored by established health-technology-assessment frameworks and stable reimbursement pathways. Germany's early-benefit assessments embed real-world evidence requirements that reward durable efficacy, while the United Kingdom's post-Brexit regulatory landscape continues to parallel EMA standards. Southern-European markets negotiate centralized tenders that temper price-growth but secure broad access. Real-world registries across France and Italy inform adaptive guidelines that integrate companion-diagnostic data, reinforcing precision-medicine adoption in the systemic lupus erythematosus drugs market.

- Abbvie

- AnaptysBio

- AstraZeneca

- Aurinia Pharmaceuticals Inc.

- Biogen

- Bristol-Myers Squibb

- Eli Lilly and Company

- Equillium

- Roche

- GlaxoSmithKline

- Idorsia

- ImmuPharma

- Kyverna Therapeutics

- Merck

- Novartis

- Pfizer

- RemeGen

- Sanofi

- UCB

- Viatris

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence & Earlier Diagnosis of SLE

- 4.2.2 Rapid Approvals of Novel Biologics

- 4.2.3 Expansion of Companion-Diagnostic Biomarkers

- 4.2.4 Tele-Rheumatology Boosting Access in Underserved Areas

- 4.2.5 Venture Funding Surge for Autoimmune Biotech Platforms

- 4.2.6 Favorable Orphan-Drug & Fast-Track Designations

- 4.3 Market Restraints

- 4.3.1 High Therapy Cost & Reimbursement Hurdles

- 4.3.2 Safety Concerns: Infection & Malignancy Risks

- 4.3.3 Cold-Chain Complexity for mAbs & Cell Therapies

- 4.3.4 Physician Inertia Toward Switching from Legacy Steroids

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Treatment Type

- 5.1.1 Non-Steroidal Anti-Inflammatory Drugs (NSAIDs)

- 5.1.2 Antimalarials

- 5.1.3 Corticosteroids

- 5.1.4 Immunosuppressants / DMARDs

- 5.1.5 Biologics

- 5.1.6 Stem-cell & Gene-based Therapies

- 5.2 By Route of Administration

- 5.2.1 Oral

- 5.2.2 Intravenous

- 5.2.3 Subcutaneous

- 5.3 By Distribution Channel

- 5.3.1 Hospital Pharmacies

- 5.3.2 Retail Pharmacies

- 5.3.3 Online Pharmacies

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AbbVie

- 6.3.2 AnaptysBio

- 6.3.3 AstraZeneca Plc

- 6.3.4 Aurinia Pharmaceuticals Inc.

- 6.3.5 Biogen

- 6.3.6 Bristol Myers Squibb Company

- 6.3.7 Eli Lilly and Company

- 6.3.8 Equillium

- 6.3.9 F. Hoffmann-La Roche Ltd

- 6.3.10 GSK Plc

- 6.3.11 Idorsia

- 6.3.12 ImmuPharma

- 6.3.13 Kyverna Therapeutics

- 6.3.14 Merck & Co.

- 6.3.15 Novartis AG

- 6.3.16 Pfizer Inc.

- 6.3.17 RemeGen

- 6.3.18 Sanofi

- 6.3.19 UCB

- 6.3.20 Viatris Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment