PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063814

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063814

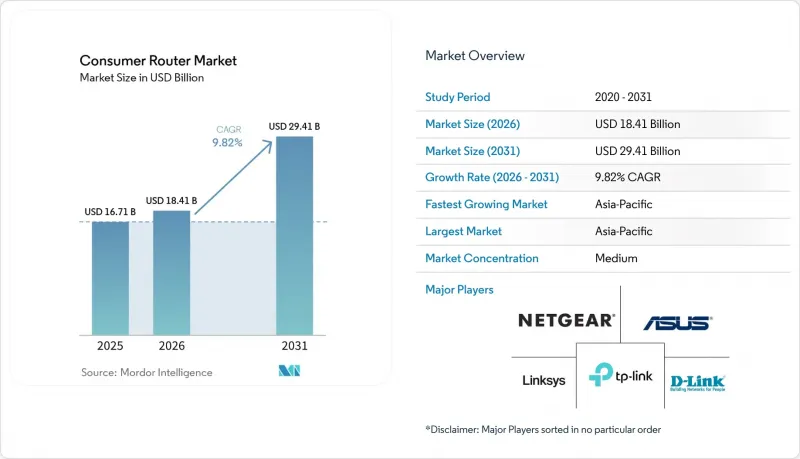

Consumer Router - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the consumer router market size is expected to be USD 16.7 billion in 2025, USD 18.41 billion in 2026, and reach USD 29.41 billion by 2031, growing at a CAGR of 9.82% from 2026 to 2031.

This report is Segmented by Product Type (Single-Band, Dual-Band, Tri-Band, and Mesh Wi-Fi Systems), Technology Standard (Wi-Fi 5, Wi-Fi 6, Wi-Fi 6E, and Wi-Fi 7 Ready), Application (Residential, Small Office / Home Office (SOHO), and Small Business), Distribution Channel (Online, and Offline), and Geography (North America, Asia Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Consumer Router Market Trends and Insights

Rapid Adoption Of Wi-Fi 6 And Wi-Fi 6E Standards

Wi-Fi 6E opens seven 160 MHz-wide channels in the 6 GHz band, eliminating legacy channel congestion and supporting latency-sensitive use cases such as cloud gaming and virtual reality. Mandatory WPA3 encryption and Hash-to-Element key exchange raise the security baseline, shrinking the attack surface for downgrade exploits. Wi-Fi 7 is forecast to exceed 90% of consumer and enterprise access-point shipments by 2029, driven by multi-link operation that aggregates 2.4, 5, and 6 GHz spectrum for theoretical throughput above 40 Gbps. ASUS showcased this capability at CES 2026 through the ROG NeoCore, revealing a two-year cadence between major standard releases and compressing product life cycles. Uneven spectrum allocation across Asia-Pacific complicates global SKU planning, yet early-moving jurisdictions are already recording accelerated replacement cycles. The net result is a shortening payback period for router upgrades, which directly lifts the consumer router market.

Surge In Smart-Home And IoT Device Installations

Households now average 17-18 connected endpoints, up from 11 in 2022, and device penetration is projected to reach 68.6% of global homes by 2027. Legacy single-band routers struggle when 40+ devices contend for airtime, leading to noticeable quality-of-service degradation. Security risks have scaled in parallel; a 2025 study reported 5,200 malicious connection attempts per IoT device each month, with 75% exploiting router vulnerabilities. Vendors such as TP-Link use on-device machine learning to prioritize real-time traffic and schedule firmware downloads during off-peak periods. The rise of Matter-certified ecosystems demands IPv6-native support and persistent low-power links, forcing a new baseline for router silicon. Collectively, these dynamics accelerate mid-cycle upgrades and uplift the consumer router market.

High Average Selling Prices Of Tri-Band And Mesh Systems

Flagship mesh kits such as NETGEAR Orbi 970 and ASUS ZenWiFi Pro ET12 list between USD 1,200 and USD 1,500, pricing many households out of the premium tier. NETGEAR's July 2025 Orbi 370 introduction at USD 599 for a two-pack narrowed the entry barrier by 30%, but it still exceeds the sub-USD 150 sweet spot that dominates unit volumes. Dual-band products now account for 65% of shipments yet generate under 40% of total revenue, underscoring margin compression. Vendors are caught between cannibalizing their own value portfolios and conceding the high-margin segment to rivals. This price bifurcation slows upgrade intent and weighs on the consumer router market.

Other drivers and restraints analyzed in the detailed report include:

- Growth Of Remote Work And Hybrid Learning Models

- Mainstream Broadband Penetration In Emerging Economies

- Persistent Semiconductor Supply Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mesh systems are growing at 14.30% annually through 2031, the fastest within the consumer router market. Dual-band routers, once the default, accounted for 65.12% of 2025 unit volume, yet their share is eroding as households discover that two radios cannot efficiently serve 17+ IoT endpoints. Tri-band designs dedicate a high-band backhaul that gamers and content creators value for low-latency uploads, lifting attach rates in North America and Europe. Single-band models now play niche roles, such as in Guinea's fixed-wireless access market, priced at CNY 429 (USD 61) or less.

NETGEAR's Orbi 370 at USD 599 compresses the price-performance curve, democratizing 320 MHz channels and 4K QAM that were confined to USD 1,200 flagships. The Wi-Fi Alliance certified more than 1,200 Wi-Fi 7 products by early 2026, unleashing scale economies that lower silicon cost baselines. Chinese challenger Tenda pushed price walls further with the Taishan BE7200 Ultra at CNY 429 (USD 61), pressuring global brands to defend margins. Vendor success now hinges on balancing sub-USD 150 dual-band throughput expectations with premium mesh differentiation, a trade-off central to the trajectory of the consumer router market size over the next five years.

Wi-Fi 6 retained 45.21% shipment share in 2025, indicating maturity and broad device compatibility, while Wi-Fi 6E is climbing 12.49% annually through 2031. The shift is principally motivated by the unlicensed 6 GHz spectrum, which provides 7 160 MHz channels, bypassing congestion in older bands. Wi-Fi 7 device shipments jumped from 583 million in 2025 to 1.1 billion in 2026, signaling an 88% growth rate that eclipses prior adoption curves for Wi-Fi standards.

Wi-Fi 5 stubbornly clings to 22% share in low-cost routers priced below USD 50. ASUS's CES 2026 preview of a Wi-Fi 8-ready ROG NeoCore platform demonstrates a two-year cadence that will likely compress router amortization periods and expand the consumer router market in bleeding-edge segments. Persistent regulatory fragmentation, however, forces vendors to maintain dual certification pathways, which inflate engineering costs. As more jurisdictions harmonize 6 GHz rules, unified SKU roadmaps will emerge, offering procurement leverage and reducing time-to-market for new designs.

Geography Analysis

Asia-Pacific dominated the consumer router market in 2025 with 34.12% revenue share and is projected to post an 11.13% CAGR through 2031. India alone added 28 million fiber connections in 2025, leapfrogging legacy DSL and driving demand for multi-gigabit routers in tier-2 and tier-3 cities. Chinese vendors, TP-Link, Huawei, Xiaomi, and Tenda, maintain more than 70% domestic share, propped up by vertical integration and localized firmware. Xiaomi's April 2026 BE3600 Pro release at CNY 1,799 (USD 248) and Huawei's Wi-Fi X portable router at CNY 2,499 (USD 364) spotlight the rapid commoditization of Wi-Fi 7 in the region.

North America and Europe collectively contributed about 48% of 2025 revenue. Growth moderates to 8.5% annually as replacement cycles lengthen beyond 4 years, but high attach rates for tri-band mesh units keep revenue density elevated. The Federal Communications Commission's March 2026 ban on specified foreign-sourced routers is forcing redesigns and supplier diversification, potentially delaying product refreshes. The European Union's harmonized 6 GHz framework, in contrast, accelerates time-to-market for Wi-Fi 6E devices.

South America is slated to grow from USD 1.45 billion in 2024 to USD 5.18 billion by 2034, with a 14.3% CAGR, with Brazil capturing more than half of the regional spend. The Middle East and Africa remain early-stage but show outsized potential, with fixed-wireless LTE routers priced under USD 100 bridging the digital divide. Localization hurdles, including import duties, currency volatility, and multilingual firmware, favor lower-margin regional entrants, but multinationals that address these frictions can unlock incremental market share in the consumer router market.

- TP-Link Technologies Co., Ltd.

- NETGEAR, Inc.

- ASUSTeK Computer Inc.

- D-Link Corporation

- Linksys Holdings, Inc.

- Ubiquiti Inc.

- MikroTikls SIA

- Zyxel Communications Corporation

- Shenzhen Tenda Technology Co., Ltd.

- Mercusys Technologies Co., Ltd.

- eero LLC

- Google LLC (Nest Devices)

- Buffalo Inc.

- AVM Computersysteme Vertriebs GmbH

- Edimax Technology Co., Ltd.

- Peplink International Limited

- DrayTek Corp.

- Comtrend Corporation

- Synology Inc.

- Huawei Device Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mainstream Broadband Penetration in Emerging Economies

- 4.2.2 Rapid Adoption of Wi-Fi 6 and Wi-Fi 6E Standards

- 4.2.3 Surge in Smart-Home and IoT Device Installations

- 4.2.4 Growth of Remote Work and Hybrid Learning Models

- 4.2.5 Telecom ISP Bundling of Premium Routers

- 4.2.6 AI-Enabled Network Optimisation in Consumer Routers

- 4.3 Market Restraints

- 4.3.1 Persistent Semiconductor Supply Constraints

- 4.3.2 High Average Selling Prices of Tri-Band and Mesh Systems

- 4.3.3 Limited Consumer Awareness of Wi-Fi Standards

- 4.3.4 Cyber-security and Firmware Maintenance Challenges

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porters Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensiyt of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Single-Band Routers

- 5.1.2 Dual-Band Routers

- 5.1.3 Tri-Band Routers

- 5.1.4 Mesh Wi-Fi Systems

- 5.2 By Technology Standard

- 5.2.1 Wi-Fi 5 (802.11ac)

- 5.2.2 Wi-Fi 6 (802.11ax)

- 5.2.3 Wi-Fi 6E (6 GHz)

- 5.2.4 Wi-Fi 7 Ready (802.11be)

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Small Office / Home Office (SOHO)

- 5.3.3 Small Business

- 5.4 By Distribution Channel

- 5.4.1 Online Retail

- 5.4.2 Offline Retail

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Kenya

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 TP-Link Technologies Co., Ltd.

- 6.4.2 NETGEAR, Inc.

- 6.4.3 ASUSTeK Computer Inc.

- 6.4.4 D-Link Corporation

- 6.4.5 Linksys Holdings, Inc.

- 6.4.6 Ubiquiti Inc.

- 6.4.7 MikroTikls SIA

- 6.4.8 Zyxel Communications Corporation

- 6.4.9 Shenzhen Tenda Technology Co., Ltd.

- 6.4.10 Mercusys Technologies Co., Ltd.

- 6.4.11 eero LLC

- 6.4.12 Google LLC (Nest Devices)

- 6.4.13 Buffalo Inc.

- 6.4.14 AVM Computersysteme Vertriebs GmbH

- 6.4.15 Edimax Technology Co., Ltd.

- 6.4.16 Peplink International Limited

- 6.4.17 DrayTek Corp.

- 6.4.18 Comtrend Corporation

- 6.4.19 Synology Inc.

- 6.4.20 Huawei Device Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment