PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063819

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063819

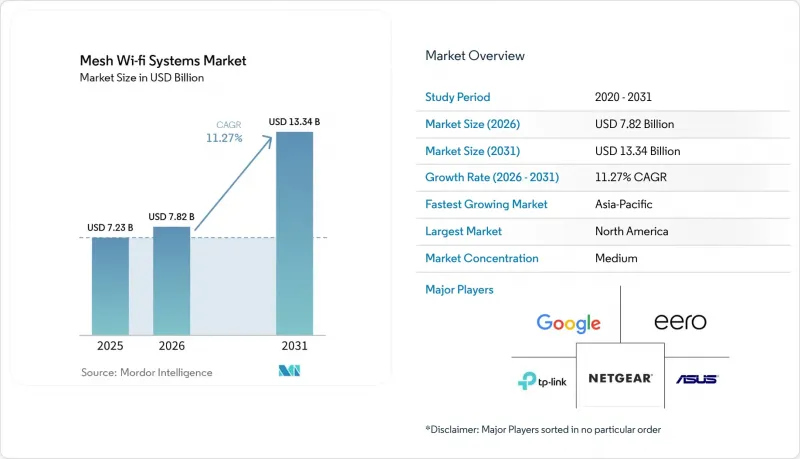

Mesh Wi-fi Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the mesh wi-Fi system markets size is projected to expand from USD 7.23 billion in 2025 and USD 7.82 billion in 2026 to USD 13.34 billion by 2031, registering a CAGR of 11.27% between 2026 to 2031.

This report is Segmented by Component (Hardware, Software, and Services), Band Count (Dual-Band, Tri-Band, Quad-Band, and Higher), Wi-Fi Standard (Wi-Fi 5, Wi-Fi 6, Wi-Fi 6E, and Wi-Fi 7), Application (Residential, and More), Distribution Channel (Online Retail and Marketplaces, and Offline/Brick-and-Mortar), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Mesh Wi-fi Systems Market Trends and Insights

Explosive Growth in Smart-Home Device Installations

Households now host 15-20 connected devices, from speakers to appliances, all vying for bandwidth. Matter 1.4.2 certification across more than 500 devices lets homeowners unify control, so mesh systems become the logical backbone. Compared with extenders, Thread-based mesh cuts packet loss by 40%, improving user satisfaction and slashing ISP support calls. As a result, retailers promote "whole-home bundles" that pair mesh kits with smart bulbs and locks. The Mesh Wi-Fi systems market, therefore, expands in lockstep with every incremental camera or voice assistant added to a residence.

Rapid Roll-Out of Gigabit and Fibre-to-the-Home Internet

Operators in South Korea, Japan, and large U.S. metros deliver symmetrical gigabit services that expose weak Wi-Fi links inside the home. To preserve promised speeds, telcos package mesh nodes into premium fiber plans, charging USD 5-10 per month and converting capital expenditure into subscription revenue. Europe's 295 million homes passed by fiber, and China's 206.8 million gigabit users repeat the pattern, proving that last-mile performance is now a competitive differentiator. Consequently, the Mesh Wi-Fi systems market captures value every time a new fiber strand reaches a front door.

Persistent Semiconductor Supply Constraints

Advanced 6 nm and 5 nm semiconductor capacity remains constrained as smartphone and data-center customers outcompete consumer networking vendors for wafer allocation. Wi-Fi 7 chipsets carry a 40-50% cost premium over Wi-Fi 6E, forcing vendors to prioritize flagship mesh systems and delay broader portfolio rollouts. Lead times extending beyond 30 weeks strain working capital, disrupt inventory planning, and limit peak-season availability. Until additional fabrication capacity comes online, supply bottlenecks will continue to suppress unit shipments, delay price normalization, and moderate near-term growth in the Mesh Wi-Fi systems market.

Other drivers and restraints analyzed in the detailed report include:

- Price Erosion in Wi-Fi 6/6E Chipsets

- Telco Adoption of Mesh CPE for Whole-Home Coverage

- Rising Cyber-Security Vulnerabilities in Home Networks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware accounted for 63.4% of the Mesh Wi-Fi market share in 2025, as customers still purchase physical nodes as the first step toward reliable coverage. Yet service revenue, growing at a 13.81% CAGR, signals a pivot to recurring revenue as ISPs and vendors sell security subscriptions, parental controls, and analytics. The Mesh Wi-Fi systems market size tied to services is projected to outpace hardware incrementally each year between 2026 and 2031 as telcos bake USD 5-15 monthly charges into fiber bundles.

Software innovation underpins this shift. Cloud dashboards give homeowners device-level visibility, while AI engines orchestrate channel selection without user input. Vendors that master over-the-air updates and data analytics increase lifetime customer value, mitigating the 4- to 5-year replacement cycle that still governs node refreshes. The winner's playbook, therefore, combines affordable hardware with sticky cloud features that users pay for long after the initial install.

Dual-band kits held 48.19% share of the Mesh Wi-Fi system market in 2025 because cost-sensitive buyers needed only 2.4 GHz and 5 GHz coverage for email, streaming, and smart speakers. As bandwidth demand balloons, tri-band models add a second 5 GHz radio for dedicated backhaul, balancing price and performance. Quad-band systems are now expanding at a 15.62% CAGR, leveraging 6 GHz channels unlocked by global regulators.

With Wi-Fi 7, vendors dedicate one 6 GHz radio to backhaul and a second to clients, while legacy devices remain on 2.4 GHz and 5 GHz. Interference drops, latency sinks, and 8K streaming coexist with cloud gaming. As chipset pricing falls, quad-band premiums narrow, nudging power users, remote workers, and gamers toward higher-tier bundles. The Mesh Wi-Fi systems market size for quad-band products is therefore set to grow faster than any other configuration through 2031.

Geography Analysis

North America generated 38.96% of the Mesh Wi-Fi systems market revenue in 2025, underpinned by gigabit fiber coverage, smart-home penetration, and telco mesh bundles that now serve tens of millions of subscribers. The United States dominates regional value, backed by USD 42.45 billion in BEAD program funding that supports networks in every state. Canada's 12 million fiber homes and CAD 10 (USD 7.90) monthly managed Wi-Fi premiums add steady uptake, while Mexico's 8 million FTTH lines cluster mesh demand in its three largest cities.

Europe follows, buoyed by 160 million fiber subscribers and a 54% take-up rate that spotlights the inadequacy of legacy routers once speeds exceed 1 Gbps. Operators such as Deutsche Telekom and Orange integrate mesh networking into gigabit plans, while the EU's Cyber Resilience Act requires 5-year security support, boosting consumer trust. Russia deploys distributed nodes in concrete apartment blocks, highlighting how building stock shapes architectural choices in the Mesh Wi-Fi market.

Asia-Pacific is the fastest climber at a 14.28% CAGR, propelled by China's 206.8 million gigabit users and India's BharatNet project linking 250,000 villages. Japan's 85% fiber penetration and South Korea's 95% FTTH reach foster early adoption of Wi-Fi 7, as gamers demand stable, low-latency links. Southeast Asian capitals layer mesh onto new fiber backbones priced below USD 150 per kit, pushing affordable coverage into rising middle-class homes. Outside the top three regions, the Middle East modernizes broadband for Saudi Vision 2030, South America scales slowly amid macroeconomic stress, and sub-Saharan Africa remains early-stage, favoring 4G fixed wireless over FTTH for now.

- NETGEAR Inc.

- TP-Link Corporation Limited

- Eero LLC

- Google LLC

- Linksys Holding Inc.

- ASUStek Computer Inc.

- D-Link Corporation

- Ubiquiti Inc.

- Zyxel Communications Corporation

- Huawei Technologies Co., Ltd.

- Xiaomi Communications Co., Ltd.

- Shenzhen Tenda Technology Co., Ltd.

- Mercusys Technologies Co., Ltd.

- Commscope Holding Company Inc.

- ARRIS International plc

- Netis Systems Co., Ltd.

- Vilo Living Inc.

- Actiontec Electronics Inc.

- Synology Inc.

- Cambium Networks Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive Growth in Smart-Home Device Installations

- 4.2.2 Rapid Roll-Out of Gigabit and Fibre-to-the-Home Internet

- 4.2.3 Price Erosion in Wi-Fi 6/6E Chipsets

- 4.2.4 Telco Adoption of Mesh CPE for Whole-Home Coverage

- 4.2.5 Government-Funded Digital-Inclusion Programs

- 4.2.6 AI-Driven Self-Healing Network Algorithms

- 4.3 Market Restraints

- 4.3.1 Persistent Semiconductor Supply Constraints

- 4.3.2 Rising Cyber-Security Vulnerabilities in Home Networks

- 4.3.3 Consumer Confusion Over Wi-Fi Standards (6E vs 7)

- 4.3.4 Import Tariffs on Networking Hardware

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Band Count

- 5.2.1 Dual-Band Mesh Systems

- 5.2.2 Tri-Band Mesh Systems

- 5.2.3 Quad-Band and Higher Mesh Systems

- 5.3 By Wi-Fi Standard

- 5.3.1 Wi-Fi 5 (802.11ac)

- 5.3.2 Wi-Fi 6 (802.11ax)

- 5.3.3 Wi-Fi 6E (802.11axe)

- 5.3.4 Wi-Fi 7 (802.11be)

- 5.4 By Application

- 5.4.1 Residential

- 5.4.2 Commercial and Enterprise

- 5.4.3 Industrial and Logistics

- 5.4.4 Government and Public Sector

- 5.5 By Distribution Channel

- 5.5.1 Online Retail and Marketplaces

- 5.5.2 Offline / Brick-and-Mortar

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 ASEAN

- 5.6.4.6 Oceania

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 North Africa

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NETGEAR Inc.

- 6.4.2 TP-Link Corporation Limited

- 6.4.3 Eero LLC

- 6.4.4 Google LLC

- 6.4.5 Linksys Holding Inc.

- 6.4.6 ASUStek Computer Inc.

- 6.4.7 D-Link Corporation

- 6.4.8 Ubiquiti Inc.

- 6.4.9 Zyxel Communications Corporation

- 6.4.10 Huawei Technologies Co., Ltd.

- 6.4.11 Xiaomi Communications Co., Ltd.

- 6.4.12 Shenzhen Tenda Technology Co., Ltd.

- 6.4.13 Mercusys Technologies Co., Ltd.

- 6.4.14 Commscope Holding Company Inc.

- 6.4.15 ARRIS International plc

- 6.4.16 Netis Systems Co., Ltd.

- 6.4.17 Vilo Living Inc.

- 6.4.18 Actiontec Electronics Inc.

- 6.4.19 Synology Inc.

- 6.4.20 Cambium Networks Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment