PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063847

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063847

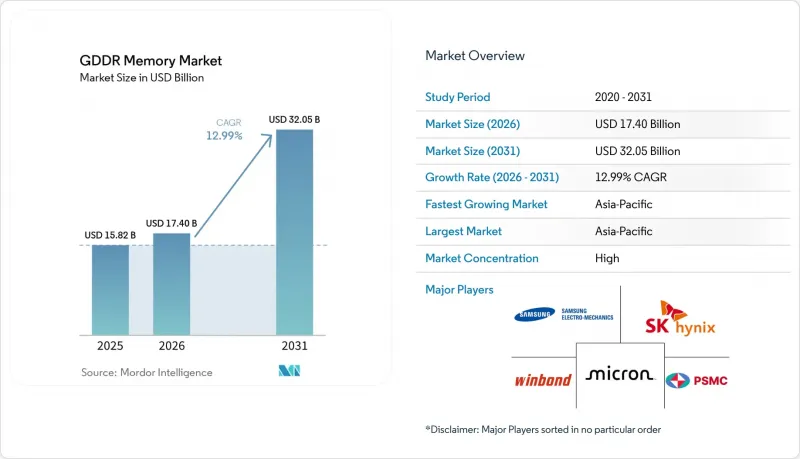

GDDR Memory - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the GDDR memory market size is expected to increase from USD 15.82 billion in 2025 to USD 17.4 billion in 2026 and reach USD 32.05 billion by 2031, growing at a CAGR of 12.99% over 2026-2031.

This report is Segmented by Memory Type (GDDR5, GDDR5X, GDDR6, and GDDR6X), Application (Gaming Graphics, Professional Visualization, AI and Compute, and More), Density (≤ 8 Gb, 8-16 Gb, and More), Data Rate (≤ 12 Gbps, 12-16 Gbps, and More), End-User Industry (Consumer Electronics, IT and Data Centers, Media and Entertainment, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global GDDR Memory Market Trends and Insights

Growing Demand for Real-Time Ray Tracing in AAA Games

NVIDIA's GeForce RTX 50 series debuted in January 2025 with GDDR7 running at 30 Gbps, delivering 1.7 TB/s aggregate bandwidth on the RTX 5090 and enabling path-traced lighting pipelines previously limited to offline renders. DLSS 4 adoption expanded to more than 250 titles the same year, escalating bandwidth needs for pixel-accurate reflections and global illumination. AMD's Radeon RX 9000 family, released in February 2025, relied on 18-20 Gbps GDDR6 to service mainstream ray-traced workloads, reinforcing GDDR6 as the volume node while ceding the performance crown to GDDR7. Micron data shows 30% higher frame rates for GDDR7-equipped boards across 1080p to 4K tests relative to GDDR6, confirming bandwidth as the critical performance lever. As studio pipelines shift from rasterization to hybrid tracing, GPU vendors market sustained memory throughput as a headline spec, propelling the GDDR memory market.

Expansion of AI Accelerator Cards Requiring High-Bandwidth Memory

Edge inference and workstation AI workloads increasingly opt for GDDR7 over costly HBM stacks. NVIDIA's RTX PRO 6000 Blackwell, launched in March 2025, integrates 96 GB of GDDR7 memory, delivering 1.79 TB/s and supporting local large-language-model inference and generative image synthesis. Samsung's 24 Gb GDDR7, introduced in October 2024, uses PAM3 signaling to exceed 40 Gbps while cutting power draw by more than 30% through clock-gating and dual-VDD rails. Micron benchmarks suggest 20% lower inference latency than GDDR6 at 32 Gbps. These performance and cost dynamics widen the GDDR memory market beyond gaming into enterprise AI hardware.

Supply Chain Disruptions Due to Geopolitical Tensions

U.S. export rules tightened in December 2024, adding 140 mainland Chinese entities to the Entity List and restricting on-site tool service critical for 10 nm DRAM lines. ChangXin Memory Technologies stockpiled spares to buffer until 2027, but lead times for niche lithography modules still exceed 60 weeks. South Korea's dominance, with USD 173.4 billion in semiconductor exports in 2025, creates single points of failure, amplified by maritime choke points. Alleged intellectual-property leaks worth KRW 5 trillion (USD 3.56 billion) in December 2025 underscore rivalry risks. Buyers now carry 40-week inventories, inflating working capital and pressuring OEM margins, a drag on the GDDR memory market growth vector.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Adoption of 4K/8K Displays in Consumer Electronics

- Rising Data Center GPU Deployments for Cloud Gaming Services

- Rising ASP Volatility Linked to Cryptocurrency Mining Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

GDDR6's market share reached 53.84% in 2025, reflecting broad design wins across gaming, workstation, and automotive boards. Sustained 18-20 Gbps speed bins and mature yield profiles enable cost advantages that keep GDDR6 the default choice for mainstream cards. Momentum for GDDR6X is strongest in enthusiast GPUs, where its 13.79% forecast CAGR mirrors rising appetite for 20-23 Gbps lanes. At the cutting edge, Micron and Samsung now sample GDDR7 with 32-40 Gbps capability, promising 60% higher system bandwidth and resetting performance expectations. Over the medium term, OEMs are expected to split workflows: cost-sensitive SKUs on GDDR6, flagship parts on GDDR7, and sustain healthy multi-node demand within the GDDR memory market share landscape.

Backward-compatible GDDR5 and GDDR5X continue to play a significant role in supporting consoles and value GPUs, providing a cost-effective solution for these segments. However, the increasing obsolescence of these nodes and the reduction in wafer allocations indicate their gradual phase-out, which is expected to be completed by 2028. Samsung's strategy of sampling 24 Gbps GDDR6 highlights the company's focus on extending the lifecycle of the current node, ensuring its relevance until GDDR7 production capacity becomes more widely available. As a result, buyers will face an extended transition period where GDDR5, GDDR5X, and GDDR6 coexist in the market. During this time, they will need to carefully balance their bill-of-materials (BOM) budgets with their performance requirements to make optimal purchasing decisions.

Gaming graphics captured 59.32% of the GDDR memory market share in 2025, driven primarily by the consistent demand for discrete GPU shipments to PC builders and console OEMs. However, unit growth in this segment is showing signs of plateauing, prompting suppliers to shift their focus to emerging AI and compute workflows. These workflows are now demonstrating the fastest growth, with a compound annual growth rate (CAGR) of 13.68%. The RTX PRO 6000 Blackwell, with a 96 GB frame buffer, is a prime example of this strategic shift. It highlights the adoption of GDDR7 as a cost-effective alternative to HBM for inference cards, particularly in scenarios where latency and board-level simplicity take precedence over achieving multi-terabyte-per-second aggregates.

In the professional visualization segment, the market is increasingly adopting a hybrid approach that blends traditional gaming technologies with advanced AI capabilities. Meanwhile, embedded graphics for automotive clusters are leaning toward mid-speed GDDR6, as the extended qualification cycles in this sector favor the use of mature nodes. Across various verticals, the ongoing transition from pure raster pipelines to a combination of ray-traced and AI-enhanced workloads is further reinforcing the structural demand for high-bandwidth graphics DRAM, ensuring its critical role in supporting next-generation applications.

Geography Analysis

Asia-Pacific accounted for 68.42% of the GDDR memory market share in 2025 and is projected to expand at a 14.19% CAGR to 2031. South Korea hosts the world's largest DRAM mega-fabs, including Samsung's Pyeongtaek and SK hynix's Icheon and Yongin campuses, which together churn out more than 65% of global GDDR wafers. Samsung increased Xi'an NAND investment by 67.5% year on year to KRW 465.4 billion (USD 308.8 million), diverting capital toward memory capacity for AI workloads. SK hynix, meanwhile, committed KRW 21.6 trillion (USD 15.2 billion) to accelerate Yongin's cleanroom start to February 2027, positioning the cluster as the first high-volume 1Y DRAM site. China's ChangXin Memory Technologies crept to roughly 5% global DRAM share by Q3 2025, buoyed by state-backed funds and a planned USD 4.2 billion Shanghai IPO.

North America represents the fastest strategic shift in fabrication localization. Micron's USD 20 billion FY 2026 CAPEX is allocated to finance new DRAM fabrication facilities in Idaho and New York, as well as a USD 7 billion advanced-packaging hub in Singapore. This significant investment is supported by the CHIPS and Science Act, which awarded Micron USD 6.165 billion and Intel USD 7.865 billion in direct grants. These grants aim to anchor a robust domestic back-end ecosystem, reducing reliance on overseas production. In contrast, Europe's EU Chips Act lags behind with smaller pilot lines, leaving the region heavily dependent on imports to meet its semiconductor needs.

South America and the Middle East and Africa currently account for marginal volumes in the global semiconductor market. However, these regions are experiencing low-teens demand growth, driven primarily by the import of gaming rigs and OEM-distributed products. Despite this growth, limited local assembly capacity and underdeveloped semiconductor policies hinder their ability to establish a significant manufacturing presence. As a result, these regions are expected to continue relying on Asia-Pacific-produced dies throughout the forecast period, maintaining their current share in the GDDR memory market.

- Samsung Electronics Co., Ltd.

- SK hynix Inc.

- Micron Technology, Inc.

- Winbond Electronics Corporation

- Powerchip Semiconductor Manufacturing Corporation

- Yangtze Memory Technologies Co., Ltd.

- Nanya Technology Corporation

- ADATA Technology Co., Ltd.

- Kingston Technology Corporation

- SMART Modular Technologies, Inc.

- G.Skill International Enterprise Co., Ltd.

- Corsair Memory, Inc.

- PNY Technologies, Inc.

- Patriot Memory LLC

- TeamGroup Inc.

- Apacer Technology Inc.

- Galax

- ChangXin Memory Technologies

- Windbond Electronics Corporation

- Xi'an UniIC Semiconductors Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Real-Time Ray Tracing in AAA Games

- 4.2.2 Expansion of AI Accelerator Cards Requiring High-Bandwidth Memory

- 4.2.3 Increasing Adoption of 4K/8K Displays in Consumer Electronics

- 4.2.4 Rising Data Center GPU Deployments for Cloud Gaming Services

- 4.2.5 Maturing 10 nm-Class DRAM Node Enabling Cost-Effective GDDR6 Production

- 4.2.6 Government Incentives for Domestic Semiconductor Manufacturing

- 4.3 Market Restraints

- 4.3.1 Supply Chain Disruptions Due to Geopolitical Tensions

- 4.3.2 Rising ASP Volatility Linked to Cryptocurrency Mining Cycles

- 4.3.3 Thermal Design Constraints in High-Density GDDR Packages

- 4.3.4 Competition From HBM3 in High-Performance Computing

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Memory Type

- 5.1.1 GDDR5

- 5.1.2 GDDR5X

- 5.1.3 GDDR6

- 5.1.4 GDDR6X

- 5.2 By Application

- 5.2.1 Gaming Graphics

- 5.2.2 Professional Visualization

- 5.2.3 AI and Compute

- 5.2.4 Embedded and Industrial Graphics

- 5.3 By Density

- 5.3.1 <= 8 Gb

- 5.3.2 8-16 Gb

- 5.3.3 Above 16 Gb

- 5.4 By Data Rate

- 5.4.1 <= 12 Gbps

- 5.4.2 12-16 Gbps

- 5.4.3 Above 16 Gbps

- 5.5 By End-User Industry

- 5.5.1 Consumer Electronics (Gaming, Consoles)

- 5.5.2 IT and Data Centers (AI, Cloud Inference)

- 5.5.3 Media and Entertainment (Rendering, VFX)

- 5.5.4 Industrial and Healthcare

- 5.5.5 Aerospace and Defense

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Southeast Asia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Samsung Electronics Co., Ltd.

- 6.4.2 SK hynix Inc.

- 6.4.3 Micron Technology, Inc.

- 6.4.4 Winbond Electronics Corporation

- 6.4.5 Powerchip Semiconductor Manufacturing Corporation

- 6.4.6 Yangtze Memory Technologies Co., Ltd.

- 6.4.7 Nanya Technology Corporation

- 6.4.8 ADATA Technology Co., Ltd.

- 6.4.9 Kingston Technology Corporation

- 6.4.10 SMART Modular Technologies, Inc.

- 6.4.11 G.Skill International Enterprise Co., Ltd.

- 6.4.12 Corsair Memory, Inc.

- 6.4.13 PNY Technologies, Inc.

- 6.4.14 Patriot Memory LLC

- 6.4.15 TeamGroup Inc.

- 6.4.16 Apacer Technology Inc.

- 6.4.17 Galax

- 6.4.18 ChangXin Memory Technologies

- 6.4.19 Windbond Electronics Corporation

- 6.4.20 Xi'an UniIC Semiconductors Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment