PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063862

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063862

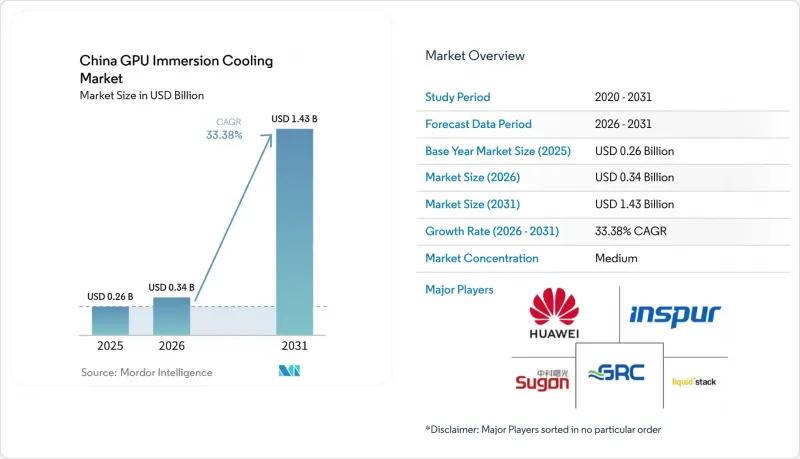

China GPU Immersion Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the china gPU immersion cooling market size is expected to be USD 0.34 billion in 2026 and reach USD 1.43 billion by 2031, growing at a CAGR of 33.38% from 2026 to 2031.

This report is Segmented by Immersion Type (Single-Phase, and Two-Phase), Solution Type (Tanks/Systems, Dielectric Fluids, and Immersion-Optimized GPU Server Systems), Deployment (Hyperscale/Cloud, Enterprise, and Government and Research HPC), GPU Power Density (Below 300W, 300W-700W, and Above 700W), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

China GPU Immersion Cooling Market Trends and Insights

Surging AI Model Training Workloads in Chinese Data Centers

China's installed base of AI-oriented GPUs tripled between 2024 and 2025, and MIIT projects domestic output to hit 300,000 units in 2026. Model-training clusters such as DeepSeek's planned 50,000-GPU facility in Inner Mongolia run at sustained loads of 350 W-700 W per chip, driving thermal densities beyond the economic reach of air cooling. Sugon's 60,000-GPU installation in Zhengzhou demonstrates that immersion architectures reclaim 40% floor area by removing hot-aisle containment and supplemental chillers. Although inference nodes proliferate at the edge, training jobs dominate immersion adoption because they draw the highest continuous power. National algorithm-registration rules that compel on-premises compute for sensitive data amplify GPU demand, further tightening the thermal envelope.

Government Carbon-Neutrality Mandates for Data Center PUE Reduction

The National Development and Reform Commission's February 2025 directive obliges new data centers to achieve PUE below 1.3, while existing sites must retrofit to 1.5 by 2027. Beijing augments the policy with a CNY 0.10 (USD 0.013) kWh surcharge on sites above PUE 1.35, imposing multi-million-yuan penalties on a 10 MW facility. Alibaba's Hangzhou campus records a 1.09 PUE with single-phase immersion versus 1.25 under air flow, thanks to 30%-35% auxiliary-power savings. MIIT's Green Data Center badge fast-tracks grid connections for projects under PUE 1.2, and counties such as Helinge'er layer 1% subsidies atop utility discounts, tipping return-on-capital decisively toward immersion.

Limited Domestic Supply Chain for High-Grade Dielectric Fluids

3M's August 2025 Novec exit removed the dominant fluorocarbon source, forcing operators to qualify domestic substitutes such as Uni-President Petrochemical's IMF F6210. Prices for single-phase fluid plunged from CNY 640,000 (USD 89,000) t-1 in 2024 to CNY 200,000 (USD 27,900) t-1 by early 2026, yet supply is concentrated among three producers, raising procurement risk. Two-phase fluids remain scarcer and costlier because local producers lack mid-boiling-point chemistries. Shell and Sinopec's January 2026 joint venture targets 5,000 t annual capacity by 2027, but hyperscalers pre-buy 18-24 months of stock, inflating working capital.

Other drivers and restraints analyzed in the detailed report include:

- Emergence of Immersion-Ready 700 + W GPU Reference Designs From OEMs

- Accelerating Expansion of Domestic GPU Manufacturing Capabilities

- Fire Codes and Building Standards Lagging Immersion Installations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Single-phase designs held 78.22% of China GPU immersion cooling market size in 2025 because mineral-oil fluids cost CNY 35,000-105,000 (USD 4,860-14,583) t-1, far below two-phase fluorocarbons. Alibaba's Hangzhou and Zhangbei campuses validated 1.05 PUE with single-phase tanks, proving that complex phase-change loops are not mandatory for efficiency targets. Two-phase systems, however, extract latent heat and return it as building warming, cutting total facility energy use by 18% during winter at the Zhengzhou supercomputing node.

Looking ahead, two-phase capacity is set to rise at a 33.67% CAGR because northern provinces can exploit low ambient temperatures for passive rejection. Yet price parity hinges on domestic fluorocarbon output scaling after 2028. For now, enterprises favor single-phase because maintenance is simpler and third-party service networks are mature. Government HPC buyers weigh energy-recovery credits more heavily, nudging the segment mix slowly toward two-phase.

Immersion-optimized GPU server systems secured the biggest slice of China GPU immersion cooling market share at 55.34% in 2025 and will remain the primary growth engine. Sugon's I980-G80 rack cuts deployment from six weeks to ten days, eliminating field retrofits. Inspur's NF5498 arrives with fluid-resistant coatings, shifting thermal-validation liability to the OEM and reassuring risk-averse CIOs.

Dielectric fluids present lower invoice totals because they amortize over five-to-seven years, whereas servers refresh triennially. Stand-alone tank makers face price pressure from new domestic entrants who discount Western gear by 30%-40%. Vendors now bundle multi-year fluid-service contracts, turning capex into opex and aligning budgets with cloud business models, which supports uptake across the China GPU immersion cooling industry.

List of Companies Covered in this Report:

- Sugon Information Industry Co., Ltd.

- Huawei Technologies Co., Ltd.

- Inspur Electronic Information Industry Co., Ltd.

- Lenovo Group Limited

- Tencent Holdings Limited

- Alibaba Group Holding Limited

- Baidu, Inc.

- China Mobile Communications Corporation

- GRC (Green Revolution Cooling, Inc.)

- LiquidStack Holdings Inc.

- Submer Technologies SL

- CoolIT Systems Inc.

- Iceotope Technologies Limited

- Shenzhen Immersion Cooling Technology Co., Ltd.

- Zhejiang Tiangong Cooling Technology Co., Ltd.

- Qingdao Haier Intelligent Cooling Technology Co., Ltd.

- Chemours Chemical (Shanghai) Co., Ltd.

- Shell plc

- Sinopec Lubricants Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging AI Model Training Workloads in Chinese Data Centers

- 4.2.2 Government Carbon-Neutrality Mandates for Data Center PUE Reduction

- 4.2.3 Accelerating Expansion of Domestic GPU Manufacturing Capabilities

- 4.2.4 Rising Electricity Tariffs in Tier-1 Cities Encouraging Thermal Efficiency

- 4.2.5 Availability of Subsidized Industrial Parks in Cooler Northern Provinces

- 4.2.6 Emergence of Immersion-Ready 700+ W GPU Reference Designs from OEMs

- 4.3 Market Restraints

- 4.3.1 Limited Domestic Supply Chain for High-Grade Dielectric Fluids

- 4.3.2 Fire Codes and Building Standards Lagging Immersion Installations

- 4.3.3 Water-Based Adiabatic Alternatives Competing on Capex

- 4.3.4 Perceived Warranty Risk by GPU Vendors for Immersion Use

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE and GROWTH FORECASTS

- 5.1 By Immersion Type

- 5.1.1 Single-Phase Immersion Cooling

- 5.1.2 Two-Phase Immersion Cooling

- 5.2 By Solution Type

- 5.2.1 Immersion Cooling Tanks / Systems

- 5.2.2 Dielectric Fluids

- 5.2.3 Immersion-Optimized GPU Server Systems

- 5.3 By Deployment

- 5.3.1 Hyperscale / Cloud

- 5.3.2 Enterprise

- 5.3.3 Government and Research (HPC)

- 5.4 By GPU Power Density

- 5.4.1 Below 300W

- 5.4.2 300W - 700W

- 5.4.3 Above 700W

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Sugon Information Industry Co., Ltd.

- 6.4.2 Huawei Technologies Co., Ltd.

- 6.4.3 Inspur Electronic Information Industry Co., Ltd.

- 6.4.4 Lenovo Group Limited

- 6.4.5 Tencent Holdings Limited

- 6.4.6 Alibaba Group Holding Limited

- 6.4.7 Baidu, Inc.

- 6.4.8 China Mobile Communications Corporation

- 6.4.9 GRC (Green Revolution Cooling, Inc.)

- 6.4.10 LiquidStack Holdings Inc.

- 6.4.11 Submer Technologies SL

- 6.4.12 CoolIT Systems Inc.

- 6.4.13 Iceotope Technologies Limited

- 6.4.14 Shenzhen Immersion Cooling Technology Co., Ltd.

- 6.4.15 Zhejiang Tiangong Cooling Technology Co., Ltd.

- 6.4.16 Qingdao Haier Intelligent Cooling Technology Co., Ltd.

- 6.4.17 Chemours Chemical (Shanghai) Co., Ltd.

- 6.4.18 Shell plc

- 6.4.19 Sinopec Lubricants Company

7 MARKET OPPORTUNITIES and FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment