PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063863

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063863

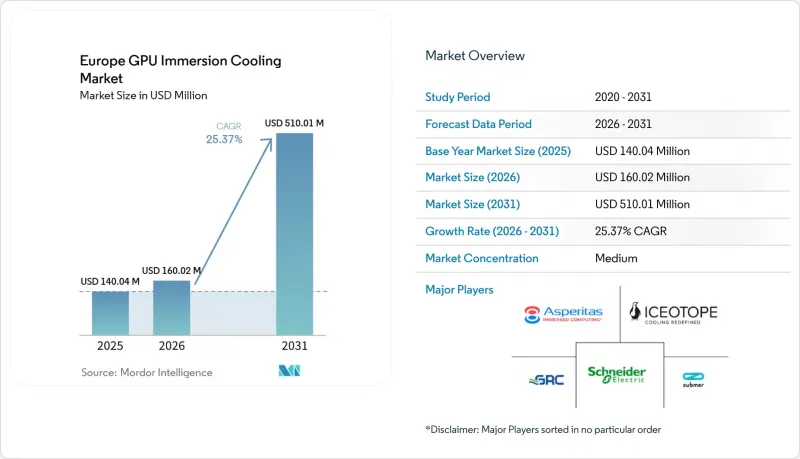

Europe GPU Immersion Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the europe gPU immersion cooling market size is expected to be USD 140.04 million in 2025, USD 160.02 million in 2026, and reach USD 510.01 million by 2031, growing at a CAGR of 25.37% from 2026 to 2031.

This report is Segmented by Immersion Type (Single-Phase, and Two-Phase), Solution Type (Tanks/Systems, Dielectric Fluids, and Immersion-Optimized GPU Servers), Deployment (Hyperscale/Cloud, Enterprise, and Government and Research HPC), GPU Power Density (Below 300W, 300W-700W, and Above 700W), and Geography (Germany, France, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe GPU Immersion Cooling Market Trends and Insights

Surging AI and HPC Workloads Driving Higher-Density GPU Deployments

Generative-AI training racks built around NVIDIA H100 and H200 accelerators routinely exceed 120 kilowatts, a level that outstrips the economic ceiling of raised-floor air cooling. National and pan-European research initiatives have funded billion-euro infrastructure projects that specify liquid cooling from day one, creating reference blueprints that enterprises can emulate. EuroHPC-backed supercomputers in Hungary and Sweden, both announced in 2025, openly mandate immersion-ready designs to cope with petaflop-scale heat loads. These flagship systems reinforce a virtuous cycle of volume commitments that lower technology risk for commercial buyers. As the forthcoming B-series GPU family pushes individual chip power past 1 kilowatt, immersion transitions from an experimental option to a necessity for maintaining rack throughput without a parallel rise in facility power.

EU Data Center Sustainability Regulations and Carbon Targets

The delegated regulation under the Energy Efficiency Directive compels sites above 500 kilowatts to publish annual power-usage-effectiveness and water-usage-effectiveness metrics beginning in 2025, a disclosure regime that favors immersion-equipped plants achieving PUE near 1.05. Parallel commitments under the Climate Neutral Data Centre Pact demand net-zero operations by 2030, effectively hard-coding liquid cooling into expansion blueprints. Operators such as Asperitas have demonstrated single-phase designs that deliver coolant temperatures high enough for direct district-heating export, addressing waste-heat clauses within the Pact. Newly approved IEC standards covering natural-ester dielectric fluids provide certification pathways that streamline tender procedures, further accelerating adoption.

High Up-Front Capex Versus Traditional Air Cooling

Turnkey immersion racks cost USD 30,000-50,000, dwarfing the USD 1,000-2,000 price of a conventional rack, even though whole-facility comparisons can favor immersion when scale effects are considered. Retrofit pilots often face a 40% cost premium because owners must re-plumb chilled-water loops, upgrade floor loading, and commission dielectric-compatible monitoring systems. Cash-constrained enterprises that operate under three-year payback rules struggle to reconcile those economics, particularly when incremental air-cooling upgrades deliver near-term relief. Cooling-as-a-service and leasing schemes are emerging but remain embryonic, limiting near-term impact on capital allocations.

Other drivers and restraints analyzed in the detailed report include:

- Escalating Electricity Prices in Western Europe Encouraging Energy-Efficient Cooling

- Rapid Decline in Dielectric Fluid Costs

- Limited Availability of GPU-Qualified Immersion-Ready Warranties

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Single-phase immersion cooling held 78.56% of the Europe GPU immersion cooling market share in 2025, underscoring widespread confidence in its fluid stability and simple operations. The Europe GPU immersion cooling market size tied to single-phase designs is expanding steadily as suppliers such as Shell and Perstorp bring PFAS-free hydrocarbon fluids to market, reducing both cost and regulatory risk. Enterprises value the compatibility of these systems with existing chilled-water loops, a factor that shortens retrofit timelines. In urban edge sites, pumpless natural-convection variants demonstrated by Asperitas are proving attractive because they operate quietly and generate 55-degree-Celsius outlet temperatures suitable for district heating.

Two-phase systems are on track for a 25.55% CAGR through 2031, yet they remain concentrated in hyperscale and research settings where rack densities cross 150 kilowatts. Fluorocarbon fluid loss, pressure-control complexity, and specialised seals have limited penetration outside those niches. The CoolHeatDC project, co-funded by SINTEF, aims to commercialise two-phase modules tied directly to heat pumps, a configuration that could broaden appeal if field trials validate maintenance expectations. As GPUs inch toward 1 kilowatt per device, two-phase designs will likely capture incremental share, though single-phase is set to maintain the majority position for the remainder of the decade.

Tanks and heat-exchange systems represented 55.34% of the Europe GPU immersion cooling market size in 2025 because early adopters sourced enclosures and servers separately. That procurement model is shifting as Dell, Hewlett Packard Enterprise, Lenovo, and Supermicro release immersion-optimized SKUs that bundle server chassis, cold plates, and certified fluid compatibility. Europe GPU immersion cooling industry observers note that these turnkey offers compress deployment cycles and eliminate warranty disputes, positioning integrated servers for the strongest growth at 25.63% through 2031.

Fluid suppliers are differentiating through sustainability metrics, with Perstorp's PFAS-free Synmerse range and Oleon's plant-based formulations highlighting the trend. Tank manufacturers such as DCX and Baltimore Aircoil have responded by publishing standardised module footprints, cutting lead times to under two months for high-volume orders. Analysts expect that once server OEMs finish extending liquid-ready lines across their full GPU portfolios, the balance of revenue will tilt toward integrated systems, while standalone tanks will retain relevance for hyperscale custom builds and facility retrofits.

List of Companies Covered in this Report:

- Submer Technologies SL

- Asperitas BV

- Iceotope Technologies Limited

- Green Revolution Cooling Inc.

- Schneider Electric SE

- DCX -The Liquid Cooling Company Sp. z o.o.

- LiquidStack Inc.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Lenovo Group Limited

- Atos SE

- Fujitsu Limited

- Super Micro Computer Inc.

- Rittal GmbH and Co. KG

- Vertiv Group Corp.

- Midas Green Technologies LLC

- Boston Limited

- Inspur Systems Inc.

- ASUS Tek Computer Inc.

- Trane Technologies plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging AI and HPC Workloads Driving Higher-Density GPU Deployments

- 4.2.2 Rapid Decline in Dielectric Fluid Costs

- 4.2.3 Escalating Electricity Prices in Western Europe Encouraging Energy-Efficient Cooling

- 4.2.4 EU Data Center Sustainability Regulations and Carbon Targets

- 4.2.5 Increased Venture Funding for European Immersion Cooling Start-ups

- 4.2.6 Growing Preference for Edge Data Centers in Urban Europe

- 4.3 Market Restraints

- 4.3.1 Limited Availability of GPU-Qualified Immersion-Ready Warranties

- 4.3.2 High Up-Front Capex Versus Traditional Air Cooling

- 4.3.3 Fragmented Dielectric Fluid Standards Across EU

- 4.3.4 Supply Chain Constraints for High-Performance Tanks and Seals

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Immersion Type

- 5.1.1 Single-Phase Immersion Cooling

- 5.1.2 Two-Phase Immersion Cooling

- 5.2 By Solution Type

- 5.2.1 Immersion Cooling Tanks / Systems

- 5.2.2 Dielectric Fluids

- 5.2.3 Immersion-Optimized GPU Server Systems

- 5.3 By Deployment

- 5.3.1 Hyperscale / Cloud

- 5.3.2 Enterprise

- 5.3.3 Government and Research (HPC)

- 5.4 By GPU Power Density

- 5.4.1 Below 300W

- 5.4.2 300W - 700W

- 5.4.3 Above 700W

- 5.5 By Region

- 5.5.1 Europe

- 5.5.1.1 Germany

- 5.5.1.2 United Kingdom

- 5.5.1.3 France

- 5.5.1.4 Italy

- 5.5.1.5 Rest of Europe

- 5.5.1 Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Submer Technologies SL

- 6.4.2 Asperitas BV

- 6.4.3 Iceotope Technologies Limited

- 6.4.4 Green Revolution Cooling Inc.

- 6.4.5 Schneider Electric SE

- 6.4.6 DCX -The Liquid Cooling Company Sp. z o.o.

- 6.4.7 LiquidStack Inc.

- 6.4.8 Dell Technologies Inc.

- 6.4.9 Hewlett Packard Enterprise Company

- 6.4.10 Lenovo Group Limited

- 6.4.11 Atos SE

- 6.4.12 Fujitsu Limited

- 6.4.13 Super Micro Computer Inc.

- 6.4.14 Rittal GmbH and Co. KG

- 6.4.15 Vertiv Group Corp.

- 6.4.16 Midas Green Technologies LLC

- 6.4.17 Boston Limited

- 6.4.18 Inspur Systems Inc.

- 6.4.19 ASUS Tek Computer Inc.

- 6.4.20 Trane Technologies plc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment