PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063921

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063921

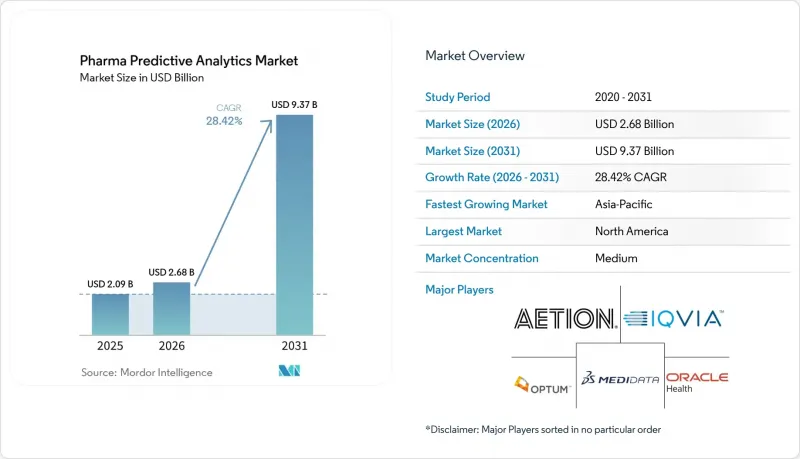

Pharma Predictive Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the pharma predictive analytics market size is expected to increase from USD 2.09 billion in 2025 to USD 2.68 billion in 2026 and reach USD 9.37 billion by 2031, growing at a CAGR of 28.42% over 2026-2031.

This report is Segmented by Component (Software and Services), Deployment (On-Premise and Cloud-Based), Technology (Big Data Analytics, and More), Data Source (Clinical-Trial Data, and More), Application (Drug Discovery & Development, and More), Therapeutic Area (Oncology, and More), End User (Pharmaceutical Companies, and More), and Geography. The Market and Forecasted in Terms of Value (USD).

Global Pharma Predictive Analytics Market Trends and Insights

Rising Adoption of AI & ML in Drug Discovery

The pharma predictive analytics market is seeing a stronger commitment to AI-led drug discovery from large pharmaceutical and technology companies. In January 2026, NVIDIA and Eli Lilly announced a co-innovation AI lab with planned investment of up to USD 1 billion over 5 years to connect wet-lab and dry-lab learning systems in a continuous loop. Merck states in March 2026 that its KERMT deep-learning model, trained on more than 11 million molecules, is already cutting early development timelines by 30% or more by screening out weak candidates before costly synthesis. In the pharma predictive analytics market, the clearest near-term value of ML sits in hit-to-lead optimization because that stage produces large data volumes and repeated failure patterns that models can learn from quickly. This is also pushing drug developers to formalize validation, documentation, and credibility standards for AI outputs before they are used in regulated submissions.

Growing Volume of Healthcare & Real-World Data

The pharma predictive analytics market is gaining momentum from the simultaneous expansion of data volume and regulatory usability in real-world evidence. In December 2025, the FDA removes a major barrier by allowing sponsors to use de-identified real-world datasets in submissions without requiring individual patient-level data in every case. In March 2026, the agency adopts ICH M14, which creates clearer standards for the design and reporting of non-interventional pharmacoepidemiological studies used in post-approval safety assessment. The practical effect in the pharma predictive analytics market is that companies with FHIR-ready and audit-ready data environments can turn these changes into a competitive advantage faster than companies still relying on fragmented records. Europe is reinforcing the same direction through the EMA's DARWIN network, which already connects 20 data partners and covers 130 million patients across the region.

Data-Privacy & Multi-Jurisdiction Compliance Complexity

The pharma predictive analytics market still faces material friction from privacy rules and model-governance obligations that differ across regions. In the United States and Europe, expectations now extend beyond basic data handling and into transparency, bias control, documentation, and post-deployment monitoring for high-risk AI systems. The EU AI Act is scheduled for full enforcement for high-risk AI systems in August 2026, which increases the compliance load for many pharma analytics applications. In the pharma predictive analytics market, this means data governance can no longer sit only with legal teams because model development, testing, and deployment now need the same compliance structure. Vendors and sponsors with unified architectures built around standards such as CDISC and FHIR will absorb these requirements faster than organizations working across disconnected data estates.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Focus on Personalized & Precision Medicine

- Need to Reduce Clinical-Trial Costs & Improve Success Rates

- High Implementation & Integration Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 68.34% share in 2025, while services are forecast to grow at a 28.93% CAGR through 2031. The pharma predictive analytics market still leans toward software because enterprise buyers want integrated analytics suites that can support discovery, clinical, safety, and commercial teams on a common platform. Cloud-native architecture has also made large deployments easier to manage across functions, which helped software expand faster during the early adoption phase. At the same time, service demand is rising because many pharmaceutical companies now need domain-specific support to extract usable value from tools they already deployed.

That shift is changing vendor positioning in the pharma predictive analytics market because buyers increasingly prefer a single provider for both platform delivery and implementation support. In March 2026, IQVIA launches IQVIA.ai as a unified agentic AI platform with more than 150 intelligent agents, which reflects a bundled platform-and-services model rather than a standalone software sale. This bundling strategy raises switching costs and narrows the room for smaller service specialists in the pharma predictive analytics industry. Regulatory qualification also remains important because enterprise buyers continue to screen for software environments that can be validated under GxP and related quality expectations.

On-premise retained 64.82% share in 2025, while cloud-based deployment is projected to grow at a 29.36% CAGR through 2031. The pharma predictive analytics market still has a large on-premise base because major pharmaceutical companies continue to prioritize IP protection, internal control, and compatibility with legacy data centers. This is especially true in environments where compound data, patient records, and model outputs need tight access control. Cloud adoption is rising quickly, but it is not replacing local infrastructure in a uniform way.

Instead, the pharma predictive analytics market is moving toward hybrid architectures where sensitive data stays on-premise, and collaboration or inference layers shift to the cloud. IQVIA and NVIDIA state in January 2025 that their collaboration uses NVIDIA DGX Cloud while maintaining healthcare-grade controls for data integrity and compliance. In Japan, AI Data Inc. launched AI PharmaCDS on IDX in November 2025 as a high-security domestic cloud environment, which shows how data residency requirements are shaping deployment design in APAC. These patterns suggest that the pharma predictive analytics market will continue to support on-premise, sovereign cloud, and private cloud models alongside broader public cloud adoption.

Big data analytics held 36.18% share in 2025, while AI and ML are projected to grow at a 30.42% CAGR through 2031. The pharma predictive analytics market still depends on big data infrastructure because model performance falls when data pipelines are fragmented, have low volume, or are poorly curated. That is why storage, integration, and processing layers remain foundational even as AI gains more attention. AI and ML are growing faster because their value is now visible in candidate optimization, patient stratification, and pharmacovigilance signal detection.

NLP is also becoming more important in the pharma predictive analytics market because large volumes of clinical notes, regulatory text, and scientific literature still sit in unstructured form. IBM Research presents an agentic AI platform at ACS Spring 2026 that uses natural-language prompts to coordinate molecule generation and screening workflows at scale. The FDA's internal use of Project Elsa in 2025 also signals that text-based AI tools are becoming more acceptable inside regulated environments, even if governance expectations remain high. Over time, the pharma predictive analytics market is likely to favor platforms that combine big data infrastructure, AI model layers, and NLP interfaces in one stack.

Geography Analysis

North America accounted for 36.46% of the pharma predictive analytics market size in 2025. It remained the largest regional cluster because the region combines deep pharmaceutical R&D spending, broad real-world data assets, and earlier regulatory clarification around AI-supported evidence generation. The pharma predictive analytics market also benefits in North America from stronger institutional capacity to document, validate, and operationalize AI tools inside regulated drug development settings. FDA actions on AI in regulatory decision-making and real-world evidence have helped create a more usable compliance baseline for companies working across development and post-approval analytics. The main structural constraint across the region remains data interoperability because fragmented EHR networks still limit how easily sponsors and vendors can build high-quality datasets at scale.

Europe remains a significant center in the pharma predictive analytics market because the region combines advanced research clusters with a stricter compliance framework that raises the quality bar for enterprise platforms. The EU AI Act is increasing implementation burden, but it is also formalizing expectations around governance, transparency, and post-market oversight for high-risk AI systems. Germany, France, the United Kingdom, and Italy continue to anchor regional deployment through established biotech ecosystems and strong public-private research capacity. Europe's regulatory pathway is also becoming more operational, as the EMA issued its first qualification opinion on an AI methodology in 2025 for AIM-NASH in liver-biopsy image analysis.

Asia-Pacific is projected to grow at a 32.98% CAGR through 2031 and stands as the fastest-growing region in the pharma predictive analytics market. Growth is being driven by digital health mandates, industry-academic collaboration, and a broader push by domestic pharmaceutical companies to build stronger analytics capability. Japan, South Korea, and China account for most of the current activity. Takeda begins AI demand forecasting across around 100 products in August 2025, while South Korea is funding a 5-year AI drug development program, and China launched Fosun Pharma's PharmAID Decision Intelligent Agent Platform in February 2025, showing the range of regional deployment models. South America is still an earlier-stage opportunity, but outsourcing-led clinical activity is beginning to create demand for analytics infrastructure that can support future expansion in the pharma predictive analytics market.

- Aetion

- Axtria

- Benevolent AI

- BioAge Labs

- Clarivate

- ConcertAI

- Cytel

- Deep 6 AI

- Exscientia

- GNS Healthcare

- IBM Watson Health / Merative

- Indegene

- IQVIA

- Medidata Solutions

- Optum

- Oracle Health Sciences

- Owkin

- Saama Technologies

- SAS Institute

- ZS Associates

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of AI & ML in Drug Discovery

- 4.2.2 Growing Volume of Healthcare & Real-World Data

- 4.2.3 Increasing Focus on Personalized & Precision Medicine

- 4.2.4 Need to Reduce Clinical-Trial Costs & Improve Success Rates

- 4.2.5 Emergence of Federated Learning for Cross-Institution Analytics

- 4.2.6 Accelerating Regulatory Sandboxes for Real-Time Trial Analytics

- 4.3 Market Restraints

- 4.3.1 Data-Privacy & Multi-Jurisdiction Compliance Complexity

- 4.3.2 High Implementation & Integration Costs

- 4.3.3 Algorithmic Bias Triggering Regulatory Push-Back

- 4.3.4 Shortage of Curated Domain-Specific Labeled Datasets

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 On-Premise

- 5.2.2 Cloud-Based

- 5.3 By Technology

- 5.3.1 Artificial Intelligence (AI) & Machine Learning (ML)

- 5.3.2 Natural Language Processing (NLP)

- 5.3.3 Big Data Analytics

- 5.3.4 Others

- 5.4 By Data Source

- 5.4.1 Electronic Health Records (EHRs)

- 5.4.2 Clinical-Trial Data

- 5.4.3 Genomic Data

- 5.4.4 Claims & Billing Data

- 5.4.5 Real-World Evidence (RWE) Data

- 5.4.6 Others

- 5.5 By Application

- 5.5.1 Drug Discovery & Development

- 5.5.2 Clinical-Trial Optimization

- 5.5.3 Patient Outcome Prediction

- 5.5.4 Pharmacovigilance & Drug Safety

- 5.5.5 Precision Medicine

- 5.5.6 Others

- 5.6 By Therapeutic Area

- 5.6.1 Oncology

- 5.6.2 Cardiovascular Diseases

- 5.6.3 Neurology

- 5.6.4 Infectious Diseases

- 5.6.5 Others

- 5.7 By End User

- 5.7.1 Pharmaceutical Companies

- 5.7.2 Biotechnology Companies

- 5.7.3 Contract Research Organizations (CROs)

- 5.7.4 Others

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Mexico

- 5.8.2 Europe

- 5.8.2.1 Germany

- 5.8.2.2 United Kingdom

- 5.8.2.3 France

- 5.8.2.4 Italy

- 5.8.2.5 Spain

- 5.8.2.6 Rest of Europe

- 5.8.3 Asia-Pacific

- 5.8.3.1 China

- 5.8.3.2 India

- 5.8.3.3 Japan

- 5.8.3.4 Australia

- 5.8.3.5 South Korea

- 5.8.3.6 Rest of Asia-Pacific

- 5.8.4 Middle East and Africa

- 5.8.4.1 GCC

- 5.8.4.2 South Africa

- 5.8.4.3 Rest of Middle East and Africa

- 5.8.5 South America

- 5.8.5.1 Brazil

- 5.8.5.2 Argentina

- 5.8.5.3 Rest of South America

- 5.8.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 Aetion

- 6.3.2 Axtria

- 6.3.3 BenevolentAI

- 6.3.4 BioAge Labs

- 6.3.5 Clarivate

- 6.3.6 ConcertAI

- 6.3.7 Cytel

- 6.3.8 Deep 6 AI

- 6.3.9 Exscientia

- 6.3.10 GNS Healthcare

- 6.3.11 IBM Watson Health / Merative

- 6.3.12 Indegene

- 6.3.13 IQVIA

- 6.3.14 Medidata Solutions

- 6.3.15 Optum

- 6.3.16 Oracle Health Sciences

- 6.3.17 Owkin

- 6.3.18 Saama Technologies

- 6.3.19 SAS Institute

- 6.3.20 ZS Associates

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment