PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072950

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072950

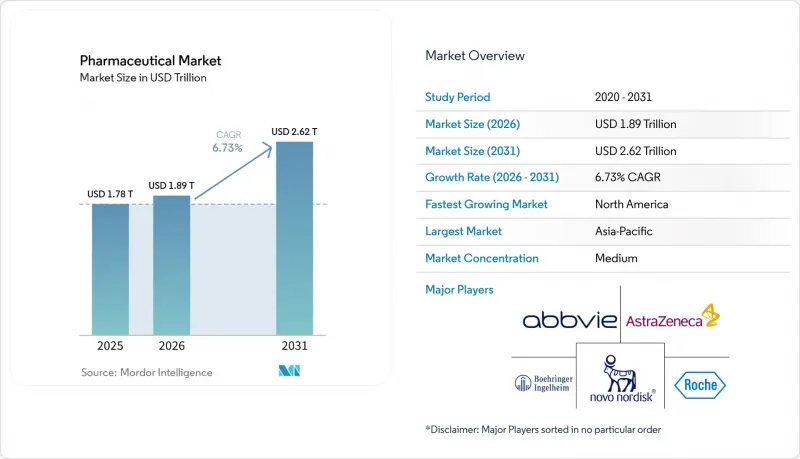

Pharmaceutical - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the pharmaceutical market size is expected to grow from USD 1.78 trillion in 2025 to USD 1.89 trillion in 2026 and is forecast to reach USD 2.62 trillion by 2031 at 6.73% CAGR over 2026-2031.

This report is Segmented by Molecule Type (Biologics/Biosimilars, Conventional Drugs), Product Type (Branded, Generic), Type (Prescription, OTC), Indication (Oncology, Cardiovascular, Endocrinology, Immunology, and More), Distribution Channel (Hospital, Retail, Online Pharmacies), and Geography (North America, Europe, Asia-Pacific, MEA, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Pharmaceutical Market Trends and Insights

Rising Burden of Chronic and Specialty Diseases

Chronic disease prevalence remains the strongest structural demand driver for the pharmaceutical market because treatment needs continue even when wider economic conditions soften. Oncology sales reached USD 288 billion in 2025, while solid tumors generated USD 194 billion and grew 13%, which keeps cancer therapies at the center of value expansion across the pharmaceutical market. Newer modalities are adding to that shift, with antibody-drug conjugates generating USD 18.8 billion in 2025 and expected to reach USD 36 billion by 2030. The dispensing model is changing as well, because cancer and Alzheimer's therapies are moving more heavily into hospital settings where higher-cost biologics can be administered with clinical oversight. This is widening the gap between commodity therapies and specialty portfolios, and that gap is pushing large manufacturers toward more focused therapeutic exposure in the pharmaceutical market.

Biologics, Biosimilars, and Precision Medicine Expansion

The shift from small molecules to biologic therapies is changing the revenue mix across the pharmaceutical market and raising the weight of products tied to complex manufacturing, premium pricing, and specialist prescribing. Bispecific antibodies generated USD 4.9 billion in 2025, and CAR-T therapies generated USD 5.8 billion, with both categories expected to continue expanding through 2030. Biosimilars are widening access at the same time, because they lower cost barriers for patients and payers that could not previously support broad biologic use. Semaglutide patent expiry in China, India, and Canada during 2026 may open a broader private-pay tier for obesity treatment across markets that contain a large share of the world's adults living with obesity. The pace of uptake will still depend on how regulators and reimbursement systems handle interchangeability, approval pathways, and formulary decisions for complex biologics.

Patent Cliffs and Branded Revenue Erosion

Loss of exclusivity remains a major restraint on the pharmaceutical market because revenue from leading brands can weaken before replacement products are fully scaled. This cycle is harder to manage because more exposed assets are biologics, where competition comes from biosimilars rather than simple small-molecule copies. First-year erosion is usually slower than in traditional generic events, but branded cash flow still comes under pressure as payers prepare formularies and physicians start switching patients. Companies with heavy dependence on a narrow set of blockbuster products face the sharpest reset, which makes launch timing and late-stage pipeline depth more important across the pharmaceutical market. The effect is uneven, because firms with strong oncology, immunology, or rare-disease launches can offset erosion faster than peers that lack near-term replacement assets.

Other drivers and restraints analyzed in the detailed report include:

- AI-Led Drug Discovery and Development Productivity Gains

- Aging Population and Longer Treatment Duration

- Pricing Pressure from Payers, PBMs, and Government Reform

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conventional drugs held 54.21% share in 2025, which means they still formed the largest volume and revenue base in the pharmaceutical market despite the strong growth of specialty therapies. Biologics and biosimilars are forecast to grow at an 8.23% CAGR through 2031, which is well above the overall pace of the pharmaceutical market and keeps the forward mix tilted toward high-value modalities. That growth is supported by monoclonal antibodies, antibody-drug conjugates, bispecific antibodies, and next-generation cell therapies that are moving into broader clinical use. Even so, conventional drugs still matter because generics, mature oral brands, and standard chronic therapies continue to supply a large share of everyday treatment volumes across the pharmaceutical market.

China's move from a generics-heavy base toward innovative biologics is now influencing how this split develops in the pharmaceutical market. Chinese innovative molecules represented 33% of all new innovative molecules in global pipelines in 2026, up from 4% in 2014, while Asia accounted for 48% of innovative pipelines and 90% of global growth in innovative molecules. This means the conventional and biologic mix will be shaped not only by demand trends, but also by where new pipelines are being built. For the pharmaceutical market, that points to a future where conventional drugs continue to anchor scale, while biologics capture a larger share of incremental value and strategic investment.

Branded drugs held 67.83% share in 2025, reflecting the pricing power of specialty biologics and the continuing relevance of established brand portfolios across major therapeutic areas. Generic drugs are projected to grow at a 7.28% CAGR through 2031, which places them ahead of the overall pharmaceutical market and positions them to benefit from wider loss-of-exclusivity activity. This setup is bringing fresh opportunities to large generic manufacturers and to Indian CDMOs and API suppliers that support rapid launch timelines. Payer pressure is also encouraging substitution before some patents expire, especially in categories where lower-cost therapeutic alternatives are already available. The pharmaceutical industry is therefore entering a phase where brand durability depends more heavily on differentiation than on legacy scale alone.

There is still an important limit to how fast the generic share can expand. A larger part of the current exclusivity cycle involves biologic products, and biosimilar conversion is slower because physician engagement and formulary approval matter more than automatic substitution at the pharmacy counter. That means share gains may arrive over several years rather than in a single step. For the pharmaceutical market, the product-type split is likely to keep shifting toward generics and biosimilars, but the speed of that transition will vary widely by therapy class and by reimbursement system.

Complete Report Scope:

- By Molecule Type

- Biologics and Biosimilars

- Conventional Drugs

- By Product Type

- Branded

- Generic

- By Type

- Prescription Drugs

- Over-the-Counter Drugs

- By Indication

- Oncology

- Cardiovascular Disease

- Endocrinology

- Immunology

- Neurology

- Infectious Diseases

- Respiratory Diseases

- Other Indications

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 41.23% share in 2025, giving it the largest regional position in the pharmaceutical market. The U.S. market is also expected to contribute more five-year absolute growth than the rest of the world combined, which keeps North America at the center of value creation. Mexico adds a smaller regional contribution, but the upcoming GLP-1 patent expiry gives it a visible near-term opening for generic expansion. This leaves North America with strong demand fundamentals, but also with the heaviest pricing and reimbursement pressure inside the pharmaceutical market.

Germany's pharmaceutical revenue rose nearly 6% to EUR 67.9 billion, or USD 72 billion, in 2025, while unit volumes declined 0.7%, showing that value growth is coming more from mix and pricing than from broader access. The EU's Critical Medicines Act has sped up manufacturing approvals for products that depend on Chinese supply chains, which shows how supply security is now affecting industrial policy. Europe's medium-term challenge is that its share of innovative pipelines is slipping while clinical trial setup remains slower than in the United States and China, which weakens its competitive position in the pharmaceutical market.

Asia-Pacific is the fastest-growing regional segment with an 8.92% CAGR through 2031, and that makes it the strongest growth engine in the pharmaceutical market outside North America. China is consolidating its place as the world's second-largest pharmaceutical market, while India is gaining relevance as a dual-sourcing and API alternative, with API imports of USD 4.35 billion in FY25 and China still supplying 73.7% of that total. The region's role is therefore expanding on both demand and supply, which gives Asia-Pacific a larger influence on pipeline formation, manufacturing strategy, and the future pharmaceutical market size. The Middle East and Africa also recorded 18% year-on-year growth in 2025, which shows that access-led expansion in the Gulf is creating a new growth tier beyond the APAC core.

- Abbvie

- Amgen

- AstraZeneca

- Bayer

- Boehringer Ingelheim

- Bristol-Myers Squibb

- Eli Lilly and Company

- Roche

- GlaxoSmithKline

- Hikma Pharmaceuticals

- Johnson & Johnson

- Merck

- Novartis

- Novo Nordisk

- Pfizer

- Sanofi

- Takeda Pharmaceuticals

- Teva Pharmaceutical Industries

- UCB

- Viatris

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Burden of Chronic and Specialty Diseases

- 4.2.2 Aging Population and Longer Treatment Duration

- 4.2.3 Biologics, Biosimilars, and Precision Medicine Expansion

- 4.2.4 AI-Led Drug Discovery and Development Productivity Gains

- 4.2.5 API Supply Chain Diversification and Dual Sourcing Imperative

- 4.2.6 Rare Disease and Ultra-Specialty Therapy Commercialization

- 4.3 Market Restraints

- 4.3.1 Patent Cliffs and Branded Revenue Erosion

- 4.3.2 Pricing Pressure from Payers, PBMs, and Government Reform

- 4.3.3 High R and D Cost and Clinical Failure Risk

- 4.3.4 Supply Concentration and Cold-Chain Dependency

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Molecule Type

- 5.1.1 Biologics and Biosimilars

- 5.1.2 Conventional Drugs

- 5.2 By Product Type

- 5.2.1 Branded

- 5.2.2 Generic

- 5.3 By Type

- 5.3.1 Prescription Drugs

- 5.3.2 Over-the-Counter Drugs

- 5.4 By Indication

- 5.4.1 Oncology

- 5.4.2 Cardiovascular Disease

- 5.4.3 Endocrinology

- 5.4.4 Immunology

- 5.4.5 Neurology

- 5.4.6 Infectious Diseases

- 5.4.7 Respiratory Diseases

- 5.4.8 Other Indications

- 5.5 By Distribution Channel

- 5.5.1 Hospital Pharmacies

- 5.5.2 Retail Pharmacies

- 5.5.3 Online Pharmacies

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 Amgen Inc.

- 6.3.3 AstraZeneca PLC

- 6.3.4 Bayer AG

- 6.3.5 Boehringer Ingelheim International GmbH

- 6.3.6 Bristol-Myers Squibb Company

- 6.3.7 Eli Lilly and Company

- 6.3.8 F. Hoffmann-La Roche Ltd

- 6.3.9 GSK plc

- 6.3.10 Hikma Pharmaceuticals PLC

- 6.3.11 Johnson & Johnson

- 6.3.12 Merck & Co., Inc.

- 6.3.13 Novartis AG

- 6.3.14 Novo Nordisk A/S

- 6.3.15 Pfizer Inc.

- 6.3.16 Sanofi

- 6.3.17 Takeda Pharmaceutical Company Limited

- 6.3.18 Teva Pharmaceutical Industries Ltd

- 6.3.19 UCB SA

- 6.3.20 Viatris Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment