PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063940

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063940

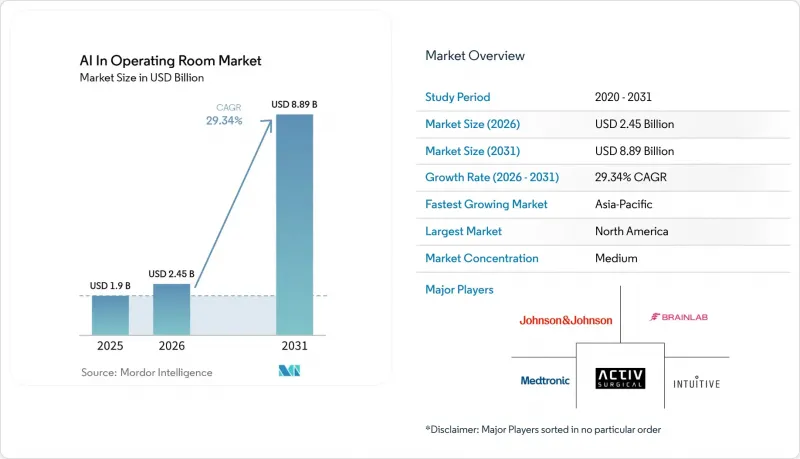

AI In Operating Room - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the aI in operating room market size is expected to increase from USD 1.9 billion in 2025 to USD 2.45 billion in 2026 and reach USD 8.89 billion by 2031, growing at a CAGR of 29.34% over 2026-2031.

This report is Segmented by Offering (Software, Hardware, Services), Technology (ML and Deep Learning, and More), Application (Guidance and Navigation, and More), Surgical Specialty (General Surgery, and More), Deployment Mode (Cloud-Based, and More), End User (Hospitals, Ascs, Clinics, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global AI In Operating Room Market Trends and Insights

Rising Demand for Minimally Invasive and Robotic-Assisted Surgeries

The growing demand for minimally invasive surgeries is driving the AI in operating room market, as these procedures rely on imaging, precision, and workflow consistency. A 2025 study revealed that AI-robotic systems reduced operative times by 25%, intraoperative complications by 30%, and improved procedural precision by 40% compared to traditional methods. In 2024, the UK performed 36,209 robotic surgeries, indicating a shift from pilot programs to widespread adoption. As more procedures are conducted, annotated surgical data enhances AI models, creating a feedback loop that simplifies robotic system use and expands adoption.

AI-Driven Intraoperative Decision Support and Real-Time Imaging Advancements

Real-time AI decision support is emerging as a key growth driver for the AI in operating room market. A validated AI system for laparoscopic liver surgery processed video at 19.2 frames per second with 89% phase recognition accuracy and 91% phase classification. Another study demonstrated AI's ability to predict perfusion during colorectal surgery with 0.98 recall within 13 seconds. In head and neck tumor surgeries, hyperspectral imaging with deep learning achieved 0.98 classification accuracy in under 10 minutes. These advancements enable standardized image interpretation and faster decision-making, reducing reliance on slower methods in critical cases.

Elevated Capital Expenditures and Overall System Ownership Costs

Acquisition costs remain a significant barrier to AI adoption in operating rooms, particularly in smaller facilities. Robotic surgery platforms are 1.5 to 2 times more expensive per procedure than laparoscopic alternatives, with da Vinci system hardware costing between USD 0.5 million and USD 2.5 million per installation. Return on investment can take 3 to 5 years for high-volume centers and over 7 years for smaller hospitals. These costs, including software licensing, integration, validation, and training, slow adoption in community hospitals. Larger health systems with higher case volumes and multi-department usage are better positioned to absorb these expenses, driving faster market growth.

Other drivers and restraints analyzed in the detailed report include:

- Global Surge in Surgical Volume Amidst Specialist Surgeon Shortages

- Imperatives for Optimizing OR Workflow and Enhancing Operational Efficiency

- Challenges in Data Privacy, Cybersecurity, and System Interoperability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, hardware contributed 45.25% of segment revenue, maintaining its position as the leading offering in the AI-driven operating room market. This was driven by investments in robotic surgical consoles, imaging systems, and edge computing units essential for intraoperative AI functions. Hospitals prioritize these purchases as foundational for digital surgery programs, with many software tools relying on installed hardware. While software adoption is growing, hardware remains critical due to its role in enabling integrated workflow solutions.

Software is projected to grow at a 32.45% CAGR through 2031, signaling a shift in value creation. Vendor-neutral software layers are gaining traction, enabling integration across diverse equipment fleets and reducing upfront costs. Software also allows vendors to update models, add workflow modules, and enhance performance through continuous learning. As hospitals demand implementation support, services like integration and training are expanding, driving a transition toward recurring software and service contracts.

Machine learning and deep learning held 48.56% of the technology segment in 2025, leading the AI-driven operating room market. Their dominance reflects advancements in surgical phase recognition, anatomy segmentation, and intraoperative risk prediction. These technologies are well-suited for operating room tasks and have demonstrated measurable clinical and operational benefits, supporting their adoption in hospital procurement.

Foundation models are redefining capabilities in this segment, with purpose-built surgical data enhancing performance. Augmented reality and virtual reality are forecast to grow at a 33.24% CAGR through 2031, driven by navigation overlays and simulation tools. The market is evolving, with machine learning driving current revenues while foundation models and AR/VR tools shape future differentiation, expanding competition beyond hardware.

Geography Analysis

In 2025, North America commanded a dominant 42.17% share of the AI in operating room market, solidifying its position as the leading regional segment. This leadership stems from a large installed base of robotic systems, strong hospital technology budgets, and consistent regulatory approvals enabling commercial rollouts. The U.S. drives growth with expanding robotic procedure adoption across specialties and hospitals' ability to integrate connected surgical platforms. Canada and Mexico, though smaller markets, benefit from modernization efforts and growing cross-border clinical collaborations.

Asia-Pacific is set to outpace all regions, boasting a projected CAGR of 34.50% through 2031. Growth is driven by hospital modernization, a widening specialist shortage, and pressure to enhance surgical productivity. China leverages high procedural volumes and supportive policies for local platform development. India sees rapid adoption of surgical robotics and AI tools in urban hospitals, while Japan and South Korea contribute with advanced digitalization and investments in precision technologies.

Europe holds strategic importance in the AI in operating room market, but adoption faces challenges from stringent regulatory requirements. The EU AI Act and medical device rules increase documentation standards, affecting time to market. Despite this, Germany, France, the U.K., Italy, and Spain lead regional demand through surgical digitization and strong clinical interest. The Middle East, Africa, and South America, though in early stages, offer growth potential as health systems aim to improve access, training, and operating room efficiency.

- Activ Surgical, Inc.

- Asensus Surgical, Inc.

- Augmedics Ltd.

- Brain Lab

- Caresyntax GmbH

- CMR Surgical Ltd.

- DeepOR S.A.S.

- ExplORer Surgical Corp.

- GE Healthcare

- Holo Surgical Inc.

- Hypervision Surgical

- Intuitive Surgical, Inc.

- Johnson & Johnson (Ethicon / Auris Health)

- Karl Storz

- LeanTaaS, Inc.

- Medtronic

- Moon Surgical

- Noah Medical

- Oath Surgical

- Proximie Ltd.

- See All AI

- Siemens Healthineers

- Stryker

- Theator, Inc.

- Zimmer Biomet

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Minimally Invasive & Robotic-Assisted Surgeries

- 4.2.2 AI-Driven Intraoperative Decision Support & Real-Time Imaging Advancements

- 4.2.3 Global Surge in Surgical Volume Amidst Surgeon Shortages

- 4.2.4 Imperatives for Optimizing OR Workflow & Enhancing Operational Efficiency

- 4.2.5 Broadened Reimbursement Policies for AI-Enhanced Medical Procedures

- 4.3 Market Restraints

- 4.3.1 Elevated Capital Expenditures and Overall Ownership Costs

- 4.3.2 Challenges in Data Privacy, Cybersecurity & System Interoperability

- 4.3.3 Navigating Regulatory Complexities & Validating AI Devices (EU AI Act, FDA SaMD)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Offering

- 5.1.1 Software

- 5.1.2 Hardware

- 5.1.3 Services

- 5.2 By Technology

- 5.2.1 Machine Learning and Deep Learning

- 5.2.2 Generative AI and Foundation Models

- 5.2.3 Natural Language Processing and Knowledge Graphs

- 5.2.4 Computer Vision and Image Recognition

- 5.2.5 Utilization of Augmented Reality (AR) / Virtual Reality (VR)

- 5.2.6 Surgery's Edge AI & IoT Integration

- 5.2.7 Robotic Process Automation (RPA) in Medical Settings

- 5.3 By Application

- 5.3.1 Guidance & Navigation During Surgery

- 5.3.2 Planning & Risk Assessment Before Surgery

- 5.3.3 Monitoring Outcomes Post-Surgery

- 5.3.4 Enhancing Surgical Workflow & Efficiency

- 5.3.5 Training & Simulation for Surgeons

- 5.4 By Surgical Speciality

- 5.4.1 General Surgical Practices

- 5.4.2 Orthopedic & Spine Procedures

- 5.4.3 Urological Surgeries

- 5.4.4 Cardiac & Cardiothoracic Operations

- 5.4.5 Neurosurgical Interventions

- 5.4.6 Gastrointestinal & Colorectal Procedures

- 5.4.7 Gynecological Surgeries

- 5.4.8 ENT & Eye Operations

- 5.4.9 Others

- 5.5 By Deployment Mode

- 5.5.1 Cloud-Based

- 5.5.2 Hybrid

- 5.5.3 On-Premises

- 5.6 By End User

- 5.6.1 Hospitals & Surgical Facilities

- 5.6.2 Centers for Ambulatory Surgery (ASCs)

- 5.6.3 Specialized Medical Clinics

- 5.6.4 Academic Institutions & Research Bodies

- 5.6.5 Facilities for Surgical Training & AI Health Technology Centers

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 Australia

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East and Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East and Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Activ Surgical, Inc.

- 6.4.2 Asensus Surgical, Inc.

- 6.4.3 Augmedics Ltd.

- 6.4.4 Brainlab AG

- 6.4.5 Caresyntax GmbH

- 6.4.6 CMR Surgical Ltd.

- 6.4.7 DeepOR S.A.S.

- 6.4.8 ExplORer Surgical Corp.

- 6.4.9 GE HealthCare

- 6.4.10 Holo Surgical Inc.

- 6.4.11 Hypervision Surgical

- 6.4.12 Intuitive Surgical, Inc.

- 6.4.13 Johnson & Johnson (Ethicon / Auris Health)

- 6.4.14 Karl Storz SE & Co. KG

- 6.4.15 LeanTaaS, Inc.

- 6.4.16 Medtronic plc

- 6.4.17 Moon Surgical

- 6.4.18 Noah Medical

- 6.4.19 Oath Surgical

- 6.4.20 Proximie Ltd.

- 6.4.21 See All AI

- 6.4.22 Siemens Healthineers AG

- 6.4.23 Stryker Corporation

- 6.4.24 Theator, Inc.

- 6.4.25 Zimmer Biomet Holdings, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space and unmet-need assessment