PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064023

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064023

North America Automotive LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

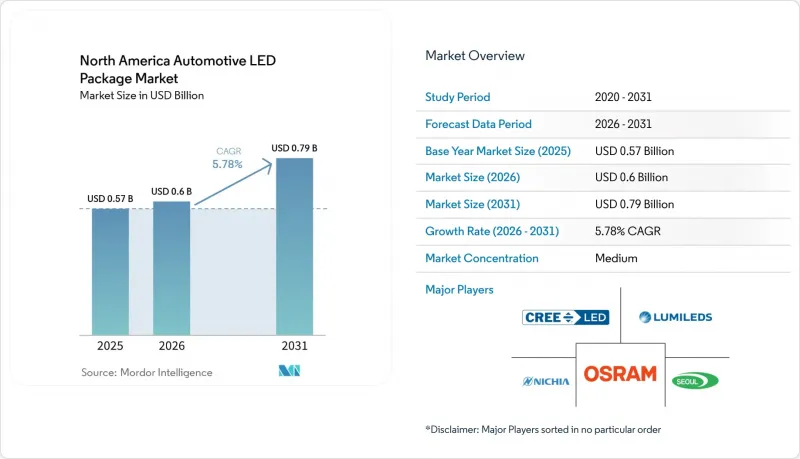

According to Mordor Intelligence, the north america automotive LED package market size is projected to expand from USD 0.57 billion in 2025 and USD 0.60 billion in 2026 to USD 0.79 billion by 2031, registering a CAGR of 5.78% between 2026 to 2031.

This report is Segmented by Package Architecture (SMD, CSP, Flip-Chip LED Packages, and COB), Power Class (Low Power, Mid Power, and High Power), Application (Exterior Lighting, Interior Lighting, Sensing/IR Applications, and Other Applications), Vehicle Type (Passenger Vehicles and Commercial Vehicles), and Country. The Market Forecasts are Provided in Terms of Value (USD).

North America Automotive LED Package Market Trends and Insights

Surge in EV Headlamp Adoption for Adaptive Driving Beams

Adaptive driving-beam headlamps are proliferating as EV platforms migrate to 48-volt architectures that simplify high-current LED driver design. Tesla activated glare-free high beams across its North American fleet in April 2025, following amendments to FMVSS 108 that cleared the last regulatory hurdle. ams OSRAM's EVIYOS HD25 entered series production on NIO's ET9 with 25,600 addressable pixels, demonstrating that automakers are willing to pay a 30-40% price premium for safety-driven differentiation. Rivian brought 480-pixel arrays to volume production in the R1T and R1S, signaling the convergence of commercial-grade lighting standards with passenger-car expectations. Because pixel density demands sub-2 mm package pitch, many tier-ones are now specifying flip-chip CSPs that slash thermal resistance while enabling thinner optics. As a result, the North America automotive LED package market is capturing incremental value from both upgraded hardware and the software licenses that orchestrate beam patterns.

Integration of µLED Arrays for Advanced ADAS Sensors

Micro-LED arrays provide uniform infrared illumination for driver-monitoring cameras and high-resolution visible light for road-scene projection. Nichia's µPLS platform, with 16,384 micro-LEDs on a 256 X 64 matrix, entered mass production for occupant-detection modules in 2025. Sony's AEC-Q100-qualified IMX775 pairs with compact 940 nm LED arrays to deliver privacy-friendly cabin monitoring beginning in spring 2026. VueReal and Flex-N-Gate are co-developing brake-light modules that embed vehicle-to-vehicle messages directly in dynamic LED pixels, blurring lines between lighting and data connectivity. These sensor-integrated packages push the North America automotive LED package market toward co-fabricated emitter-detector stacks on common substrates, an architecture that incumbents and start-ups alike are racing to patent.

Thermal Management Limits for High-Power CSP Packages

High-power chip-scale packages dissipate up to 80% of input energy as heat, and junction temperatures can climb beyond 125 °C during prolonged high-beam use. At that threshold, luminous flux can drop by 15-20% within 5,000 hours, jeopardizing the 10,000-hour warranty many automakers promise. Lumileds' LUXEON Altilon SMD-A reduces thermal resistance to 2.5 °C/W with a copper lead frame, but often still requires active cooling, which adds module mass. Flip-chip configurations improve heat paths yet require costly wafer-level underfill; early production runs have reported yield losses that raise per-die costs. These constraints limit how aggressively the North America automotive LED package market can pivot to ultra-dense headlamp arrays without parallel advances in heat-sink design or phosphor stability.

Other drivers and restraints analyzed in the detailed report include:

- OEM Shift Toward Dynamic Exterior Styling Elements

- Light-on-Demand Features Enabling New In-Cabin HMI

- Supply-Chain Exposure to Sapphire Substrate Shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Chip-scale packages increased their slice of the North America automotive LED package market to 6.42% CAGR, while surface-mount devices retained a 43.78% lead in 2025. CSPs eliminate wire bonds and shrink the footprint to within 20% of the die size, carving direct thermal paths that cut junction-to-board resistance by 30-40%. Flip-chip CSPs also support pixel pitches below 2 mm, critical for ≥400-pixel headlamp modules. However, intellectual-property disputes-Everlight sued Lumileds and Seoul Semiconductor in February 2026 over flip-chip patent US 7,554,126-inject adoption risk. SMD architectures remain preferred for cost-sensitive commercial vehicles, especially after ams OSRAM's Oslon Compact PL reached 395 lumens at 1 A, showing that incremental efficiency gains can extend the life of conventional packages.

Bridgelux's CSP line now delivers 209 lm/W at 350 mA, allowing automakers to meet brightness targets with 20-30% fewer LEDs, which trims driver-circuit and optics costs. Chip-on-board solutions achieve peak lumen density but require replacing the entire module if one die fails, limiting uptake to premium headlamps where design flexibility outweighs serviceability. Across 2026-2031, CSP shipments are forecast to close half the unit-share gap with SMDs, reinforcing their status as the fastest-advancing category in the North America automotive LED package market.

High-power LEDs above 1 W delivered 57.31% revenue in 2025 and will post a 6.55% CAGR to 2031 as adaptive-beam systems target per-package outputs beyond 400 lumens. Seoul Semiconductor's WICOP architecture in the 2024 Genesis GV80 doubled luminance compared with legacy packages and reduced heat-sink bulk by 40%, demonstrating the thermal headroom created by removing substrates. Mid-power devices occupy ambient lighting and secondary exterior signals, while low-power LEDs remain relegated to switch backlights and small indicators.

Yet micro-LED arrays blur these classes by aggregating tens of thousands of sub-0.1 W pixels into modules that draw more than 5 W. Managing heat across such dense layouts will shape power-class definitions in the North America automotive LED package market over the decade. Suppliers that integrate thermal vias and on-substrate heat spreaders are poised to capture incremental share as luminance ceilings rise.

List of Companies Covered in this Report:

- Nichia Corporation

- ams OSRAM AG

- Lumileds Holding B.V.

- Seoul Semiconductor Co., Ltd.

- CreeLED, Inc.

- Samsung Electronics Co., Ltd.

- Everlight Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Dominant Opto Technologies Sdn. Bhd.

- LITE-ON Technology Corporation

- Toyoda Gosei Co., Ltd.

- Stanley Electric Co., Ltd.

- Rohm Co., Ltd.

- Vishay Intertechnology, Inc.

- Harvatek Corporation

- Nationstar Optoelectronics Co., Ltd.

- MLS Co., Ltd. (Forest Lighting)

- Brightek Optoelectronic Co., Ltd.

- Luminus Devices, Inc.

- Epistar Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in EV Headlamp Adoption for Adaptive Driving Beams

- 4.2.2 OEM Shift Toward Dynamic Exterior Styling Elements

- 4.2.3 Light-on-Demand Features Enabling New In-Cabin HMI

- 4.2.4 Integration of µLED Arrays for Advanced ADAS Sensors

- 4.2.5 U.S. Regulatory Push for Daytime Running Lights Standardization

- 4.2.6 Mexico's Near-Shore LED Packaging Incentives Post-USMCA

- 4.3 Market Restraints

- 4.3.1 Thermal Management Limits for High-Power CSP Packages

- 4.3.2 Supply Chain Exposure to Sapphire Substrate Shortages

- 4.3.3 Passenger Vehicle LED Penetration Plateau in Canada

- 4.3.4 IP Litigation Risk in Flip-Chip Wafer-Level Packaging

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Impact of Macroeconomic Factors on the Market

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Package Architecture

- 5.1.1 SMD (Surface Mount Device)

- 5.1.2 CSP (Chip Scale Package)

- 5.1.3 Flip-Chip LED Packages

- 5.1.4 COB (Chip-on-Board)

- 5.2 By Power Class

- 5.2.1 Low Power (Less than 0.5 W)

- 5.2.2 Mid Power (0.5-1 W)

- 5.2.3 High Power (More than 1 W)

- 5.3 By Application

- 5.3.1 Exterior Lighting

- 5.3.2 Interior Lighting

- 5.3.3 Sensing / IR Applications

- 5.3.4 Other Applications

- 5.4 By Vehicle Type

- 5.4.1 Passenger Vehicles

- 5.4.2 Commercial Vehicles

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 ams OSRAM AG

- 6.4.3 Lumileds Holding B.V.

- 6.4.4 Seoul Semiconductor Co., Ltd.

- 6.4.5 CreeLED, Inc.

- 6.4.6 Samsung Electronics Co., Ltd.

- 6.4.7 Everlight Electronics Co., Ltd.

- 6.4.8 LG Innotek Co., Ltd.

- 6.4.9 Dominant Opto Technologies Sdn. Bhd.

- 6.4.10 LITE-ON Technology Corporation

- 6.4.11 Toyoda Gosei Co., Ltd.

- 6.4.12 Stanley Electric Co., Ltd.

- 6.4.13 Rohm Co., Ltd.

- 6.4.14 Vishay Intertechnology, Inc.

- 6.4.15 Harvatek Corporation

- 6.4.16 Nationstar Optoelectronics Co., Ltd.

- 6.4.17 MLS Co., Ltd. (Forest Lighting)

- 6.4.18 Brightek Optoelectronic Co., Ltd.

- 6.4.19 Luminus Devices, Inc.

- 6.4.20 Epistar Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment