PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064363

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064363

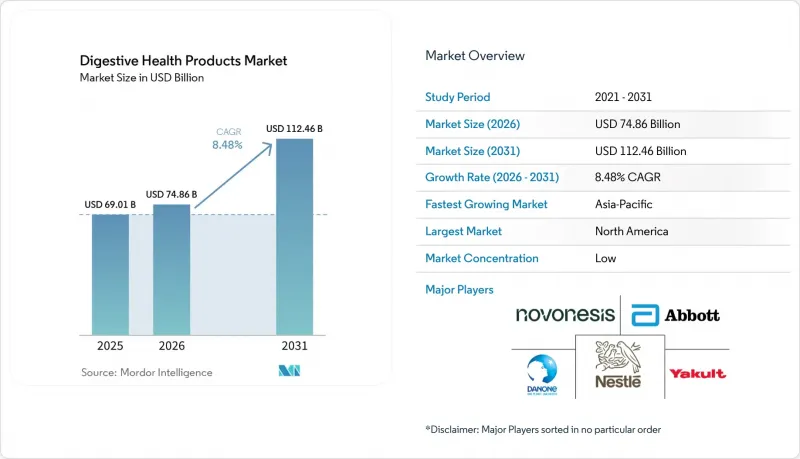

Digestive Health Products - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the global digestive health products market size is expected to grow from USD 69.01 billion in 2025 to USD 74.86 billion in 2026, and is forecast to reach USD 112.46 billion by 2031, at an 8.48% CAGR over 2026-2031.

This report is Segmented by Product Type (Functional Foods and Beverages, Supplements, and Other), Distribution Channel (Supermarkets/Hypermarkets, Convenience/Grocery Stores, Online Retail Stores, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Digestive Health Products Market Trends and Insights

Rising prevalence of digestive disorders

Propelled by the increasing prevalence of digestive disorders, the global market for digestive health products has established a strong and sustainable demand for both preventive and supportive solutions. As gastrointestinal diseases are increasingly recognized as significant contributors to global health challenges, consumers and healthcare systems are progressively adopting nutritional interventions to mitigate strain and improve health outcomes. According to the World Health Organization (WHO) in 2024, diarrhoeal disease ranks as the third leading cause of death among children aged 1-59 months. Each year, it results in approximately 443,832 fatalities among children under five and an additional 50,851 deaths among those aged 5 to 9. This alarming reality, despite the preventable and treatable nature of the disease, highlights the critical need for digestive health solutions. These solutions play a pivotal role not only in managing chronic conditions but also in addressing preventable risks through enhanced nutrition, access to safe water, and improved hygiene practices. Collectively, these factors underscore the shifting dynamics of the digestive health category, positioning these products as indispensable tools in modern wellness strategies and public health frameworks.

Growing consumer awareness of the gut-brain axis connection

As consumer awareness of the gut-brain connection increases, the digestive health products market is undergoing a significant transformation, extending its relevance beyond traditional digestive health. What began as an interest in the relationship between gut health and mental well-being has evolved into a consumer expectation. Customers are now actively seeking products that not only support digestive balance but also address stress management, enhance sleep quality, and improve cognitive performance. This shift is legitimizing digestive health claims across adjacent wellness categories. Companies with clinically substantiated claims are leveraging this trend to secure premium market positioning. For example, Yakult's Yakult 1000 series, which incorporates the Lacticaseibacillus paracasei strain Shirota, includes functional claims for stress relief and improved sleep quality. By the fiscal year 2025 (FY2025), the product is expected to achieve daily sales of 3.12 million bottles in Japan. This highlights how clinically validated gut-brain claims can drive both high sales volumes and a strong willingness to pay a premium. Simultaneously, structural dietary deficiencies, such as widespread fiber insufficiency, exacerbate the risks of gut imbalances, thereby expanding the market for fiber-based solutions. Overall, the growing emphasis on the gut-brain axis is driving a significant evolution, embedding digestive health products more deeply into holistic wellness strategies.

Stringent and inconsistent regulatory frameworks

The global digestive health products market faces a significant challenge in the form of a fragmented and stringent regulatory environment, which not only increases operational costs but also hampers innovation. Companies, particularly those operating in the probiotics and botanicals segments, encounter substantial hurdles due to the absence of harmonized global standards. This regulatory inconsistency forces businesses to navigate varying regional requirements, resulting in considerable compliance expenses. For instance, in the European Union (EU), fewer than half of the member states permit the use of the term "probiotic" on product labels. This regulatory disparity necessitates costly, region-specific packaging and customized claims strategies. Furthermore, the differing regulatory frameworks in the United States (United States), European Union (EU), and India exacerbate the complexity of cross-border product launches, often delaying market entry and reducing the return on research and development (research and development) investments. Lengthy approval processes, such as those required for multi-strain synbiotic formulations in the European Union (EU), further strain working capital and extend the time required to generate revenue. While incremental progress has been observed, such as the approval of new claims for specific ingredients and ongoing consultations regarding botanicals, achieving full regulatory harmonization remains a distant objective. These regulatory inconsistencies act as a structural barrier to market growth, disproportionately affecting mid-sized manufacturers and increasing the baseline investment necessary to compete effectively.

Other drivers and restraints analyzed in the detailed report include:

- Shift toward preventive healthcare and wellness

- Rapid expansion of e-commerce and direct-to-consumer channels: structural re-routing of consumer spending

- Consumer skepticism and lack of product standardization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, functional foods and beverages dominated the global digestive health products market, capturing 72.84% of total revenue. This dominance is supported by the extensive penetration of probiotic dairy products, particularly yogurt and fermented milk, across Europe and the Asia-Pacific region. In these markets, such products have transitioned from niche functional offerings to essential health staples. The segment is undergoing rapid diversification, with younger consumer demographics increasingly favoring kombucha, prebiotic sodas, and fiber-infused beverages, driven more by the emerging gut-brain axis narrative than by traditional digestive symptom relief. While dairy remains the leading category, significant growth opportunities exist in underpenetrated areas such as cereals, snacks, and baked goods, especially considering the widespread fiber intake deficiency highlighted by the 2025 Dietary Guidelines Advisory Committee.

In contrast, supplements represent the fastest-growing category, with a projected CAGR of 9.46% from 2026 to 2031. This growth trajectory is driven by advancements in clinical research, enabling brands to utilize strain-specific probiotic evidence for more precise differentiation compared to broadly marketed food products. Probiotics lead this segment, followed by prebiotics and enzymes, while postbiotics are emerging as a disruptive sub-category due to their inherent stability and simplified supply chain logistics. Clinical trials demonstrating measurable improvements in gut barrier integrity and immune system markers are strengthening consumer trust and gaining regulatory approval. Additionally, adherence to compliance frameworks such as International Organization for Standardization (ISO) 22000, Good Manufacturing Practices (GMP) certification, and United States Pharmacopeia (USP) verification is becoming a baseline expectation. These standards position supplements as the segment most aligned with scientific rigor and the demands of premium consumer markets.

Geography Analysis

In 2025, North America dominated the global digestive health products market, capturing a 36.78% share. This dominance was driven by high per-capita healthcare expenditure, a well-established functional food segment, and heightened consumer awareness of probiotics and dietary fiber. The region's diverse distribution channels, spanning mass retail, pharmacies, specialty stores, and digital-first subscription brands, have facilitated the coexistence of multiple value tiers, thereby driving revenue growth. Brand-led innovation and marketing strategies centered on storytelling continue to strengthen the category. For example, campaigns for products such as Tums Gummy Bites and Benefiber demonstrate how investments in consumer engagement can secure market share, even in a highly competitive environment. Additionally, increasing clinical demand, particularly in Canada, where the prevalence of inflammatory bowel disease (IBD) is rising, is expanding the market's scope from lifestyle supplements to medically oriented nutritional solutions.

Asia-Pacific is experiencing rapid growth and is projected to expand at a CAGR of 10.41% from 2026 to 2031. This growth is driven by China's market scale, Japan's aging population, the expanding urban middle class in India, and the rapid penetration of e-commerce in Southeast Asia. China's large population affected by gastrointestinal diseases, coupled with a high prevalence of functional dyspepsia, underscores the structural demand for both food-based and supplement formats. Japan's demographic profile, with one-third of its population aged 65 or older, sustains demand for digestive enzymes and probiotics designed to address age-related gastrointestinal slowdown. Meanwhile, the rise of digital-first distribution channels in Southeast Asia is accelerating product trials and adoption, positioning the region as a critical growth driver for global market players.

Europe represents a high-value yet structurally complex market, characterized by the highest global prevalence of digestive disorders and a substantial consumer base seeking functional solutions. Germany and Italy lead in terms of market size, with probiotics holding a significant share in both dietary supplements and food formats. Regulatory oversight continues to play a pivotal role, with the European Food Safety Authority's (EFSA) health claim authorizations and timelines for novel food approvals influencing product development cycles and investment strategies. While compliance costs remain substantial, the region's sophisticated consumers, who are willing to pay a premium for clinically validated products, make Europe a strategically important geography. The challenge lies in balancing regulatory complexities with the region's premium market potential.

- Nestle S.A.

- Danone S.A.

- Procter & Gamble

- Unilever

- Abbott Laboratories

- Bayer AG

- Reckitt Benckiser

- GSK (Haleon)

- BASF SE

- Novonesis

- Kraft Heinz

- BioGaia AB

- Herbalife

- Sanofi

- Zydus Wellness

- DuPont

- Arla Foods

- Yakult Honsha

- Meiji Holdings

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Digestive Disorders

- 4.2.2 Growing Consumer Awareness of Gut-Brain Axis Connection

- 4.2.3 Aging Global Population Driving Demand for Digestive Support

- 4.2.4 Shift Toward Preventive Healthcare and Wellness

- 4.2.5 Growing Popularity of Plant-Based and Clean-Label Products

- 4.2.6 Rapid Expansion of E-Commerce and Direct-to-Consumer Channels

- 4.3 Market Restraints

- 4.3.1 Stringent and Inconsistent Regulatory Frameworks

- 4.3.2 Consumer Skepticism and Lack of Product Standardization

- 4.3.3 Misleading Health Claims Eroding Consumer Trust

- 4.3.4 High Product Development and Clinical Validation Costs

- 4.4 Consumer Behavior Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Product Type

- 5.1.1 Functional Foods and Beverages

- 5.1.1.1 Dairy and Dairy-based Products

- 5.1.1.2 Functional Beverages

- 5.1.1.3 Cereals, Snacks and Bakery

- 5.1.1.4 Other Functional Food and Beverages Product

- 5.1.2 Supplements

- 5.1.2.1 Probiotics

- 5.1.2.2 Prebiotics

- 5.1.2.3 Enzymes

- 5.1.2.4 Botanicals

- 5.1.2.5 Other Supplement Type

- 5.1.3 Other Product Type

- 5.1.1 Functional Foods and Beverages

- 5.2 By Distribution Channel

- 5.2.1 Supermarkets/Hypermarkets

- 5.2.2 Convenience/Grocery Stores

- 5.2.3 Specialty and Health Stores

- 5.2.4 Online Retail Stores

- 5.2.5 Other Distribution Channels

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 Italy

- 5.3.2.4 France

- 5.3.2.5 Spain

- 5.3.2.6 Netherlands

- 5.3.2.7 Poland

- 5.3.2.8 Belgium

- 5.3.2.9 Sweden

- 5.3.2.10 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 Indonesia

- 5.3.3.6 South Korea

- 5.3.3.7 Thailand

- 5.3.3.8 Singapore

- 5.3.3.9 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Columbia

- 5.3.4.4 Chile

- 5.3.4.5 Peru

- 5.3.4.6 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 Morocco

- 5.3.5.7 Turkey

- 5.3.5.8 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nestle S.A.

- 6.4.2 Danone S.A.

- 6.4.3 Procter & Gamble

- 6.4.4 Unilever

- 6.4.5 Abbott Laboratories

- 6.4.6 Bayer AG

- 6.4.7 Reckitt Benckiser

- 6.4.8 GSK (Haleon)

- 6.4.9 BASF SE

- 6.4.10 Novonesis

- 6.4.11 Kraft Heinz

- 6.4.12 BioGaia AB

- 6.4.13 Herbalife

- 6.4.14 Sanofi

- 6.4.15 Zydus Wellness

- 6.4.16 DuPont

- 6.4.17 Arla Foods

- 6.4.18 Yakult Honsha

- 6.4.19 Meiji Holdings

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK