PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064379

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064379

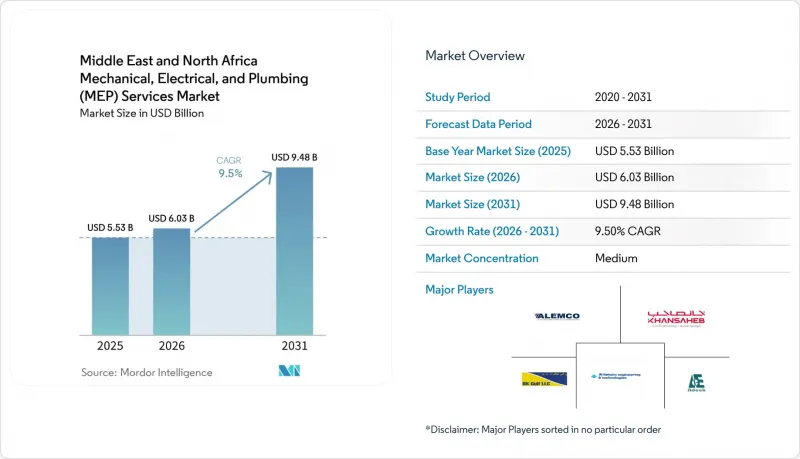

Middle East And North Africa Mechanical, Electrical, And Plumbing (MEP) Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the middle east and north africa mechanical, electrical, and plumbing services market size is projected to be USD 5.53 billion in 2025, USD 6.03 billion in 2026, and reach USD 9.48 billion by 2031, growing at a CAGR of 9.5% from 2026 to 2031.

This report is Segmented by Type (Mechanical, Electrical, Plumbing, Integrated MEP Services), Service Type (Design & Engineering, Installation Testing & Commissioning, Maintenance & Repair, Other), End-User Industry (Residential, Commercial, Infrastructure), and Geography (Saudi Arabia, UAE, Egypt, Turkey, Morocco, Rest of MENA). The Market Forecasts are Provided in Terms of Value (USD).

Middle East And North Africa Mechanical, Electrical, And Plumbing (MEP) Services Market Trends and Insights

Saudi Giga-Projects and UAE Mixed-Use Expansion

Saudi giga-project activity remains the largest demand engine in the MENA MEP services market, even as project owners apply tighter sequencing and feasibility checks across very large programs. Expo 2030 Riyadh and the 2034 FIFA World Cup keep near-term packages tied to visible delivery milestones, which makes the active pipeline more execution-led than headline-led. In the UAE, mixed-use and destination projects keep the MENA MEP services market broad across commercial, leisure, hospitality, and residential formats, which reduces dependence on a single project class. Saudi clients are also applying in-country value requirements more actively, and that is shifting competition toward contractors with local manufacturing, training capacity, and delivery depth inside the Kingdom. Scale still matters in this part of the market, but execution credibility now matters more than announced project value.

Data-Center, District-Cooling, and Mission-Critical Demand

Data-center, district-cooling, and other mission-critical projects are changing the mix of work in the MENA MEP services market because they require deeper system integration from the first design stage. Higher rack densities are pushing designers toward more complex power redundancy, liquid-cooling strategies, and backup systems than conventional commercial buildings usually require. This shifts value toward engineers and contractors that can coordinate mechanical and electrical scopes early, rather than rely on late installation fixes after procurement decisions are already locked in. District-cooling plants and network pipework also keep the MENA MEP services market tied to master-planned urban developments where large mechanical packages move in parallel with utilities and public infrastructure. These demand streams are less exposed to short-term real estate sentiment because they are linked to digital infrastructure, utility planning, and urban service platforms.

Skilled-Labor and Engineering Talent Shortages

Skilled labor and engineering shortages remain a structural limit on the MENA MEP services market because project volume is rising faster than the supply of trained people who can manage and install complex systems. The regional pipeline needs more supervisors, project managers, commissioning specialists, and certified installers, but that workforce takes time to build and is not easily replaced once project schedules compress. When MEP subcontractors cannot staff work fronts on time, main contractors absorb schedule slippage and wider claims exposure across the full project chain. Skill inconsistency is also a quality issue because some markets still lack fully standardized installer qualification requirements across HVAC and related trades. Companies that invest in internal training centers and repeatable site processes are better protected, but the workforce gap remains material across the MENA MEP services market.

Other drivers and restraints analyzed in the detailed report include:

- Energy-Efficiency Retrofits in Cooling-Intensive Buildings

- BIM-Led Design Coordination and Modular MEP Uptake

- Material Lead Times and Aggressive Price Competition

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mechanical Services held 48.3% of the MENA MEP services market share in 2025, which made it the largest type segment by a wide margin. The region's sustained cooling load keeps HVAC-related work essential across commercial buildings, residential compounds, hotels, transport assets, and public facilities, which supports large mechanical packages through both new build and retrofit cycles. Electrical Services remained the second-largest segment because data centers, smart-building systems, backup power architecture, and low-voltage networks are expanding overall system complexity in new projects. Plumbing Services stayed steady, with demand supported by desalination-linked networks, water-efficiency mandates, and wider adoption of treated-water reuse in built assets.

Integrated MEP Services is projected to grow at a 12.1% CAGR from 2026 to 2031, the fastest pace among type segments in the MENA MEP services industry. Master developers increasingly prefer single-contract accountability across mechanical, electrical, and plumbing scopes on mixed-use, hospitality, infrastructure, and giga-project programs, because coordination failures on one system can delay several others at handover. Providers with specialist teams across mission-critical systems, intelligent low-voltage work, and fast-track delivery are well positioned to benefit from this shift, particularly where project owners want fewer interfaces and tighter schedule control. Integrated delivery also aligns with stricter energy-performance expectations because cross-system modeling, testing, and commissioning are easier to manage under one lead contractor.

List of Companies Covered in this Report:

- BK Gulf

- ALEMCO

- Al-Futtaim Engineering & Technologies

- Khansaheb MEP

- Adeeb Group

- AG Engineering

- Al Shafar United

- Menasco Mechanical Contracting

- Voltas Limited

- Orascom Construction

- International Electromechanical Services

- Drake & Scull Engineering

- ETA Engineering

- KEO International Consultants

- Dar Al-Handasah

- Jacobs

- AECOM

- WSP Global

- AtkinsRealis

- Cundall

- Buro Happold

- Khatib & Alami

- Johnson Controls Arabia

- JLW Middle East

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Saudi Giga-Projects and UAE Mixed-Use Expansion

- 4.2.2 Data-Center, District-Cooling, and Mission-Critical Demand

- 4.2.3 Energy-Efficiency Retrofits in Cooling-Intensive Buildings

- 4.2.4 BIM-Led Design Coordination and Modular MEP Uptake

- 4.2.5 Airport, Tourism, and New-City Build-Outs in North Africa

- 4.2.6 Water Reuse, Desalination Linkage, and High-Efficiency Plumbing Needs

- 4.3 Market Restraints

- 4.3.1 Skilled-Labor and Engineering Talent Shortages

- 4.3.2 Material Lead Times and Aggressive Price Competition

- 4.3.3 Payment-Certification Delays and Claims-Management Risk

- 4.3.4 Geopolitical and Security Volatility in Select Markets

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Cost Structure Analysis

5 Market Size & Growth Forecasts (Value, in USD)

- 5.1 By Type

- 5.1.1 Mechanical Services

- 5.1.2 Electrical Services

- 5.1.3 Plumbing Services

- 5.1.4 Integrated MEP Services

- 5.2 By Service Type

- 5.2.1 Design & Engineering

- 5.2.2 Installation, Testing, and Commissioning

- 5.2.3 Maintenance & Repair

- 5.2.4 Other Services

- 5.3 By End-User Industry

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Infrastructure

- 5.4 By Geography

- 5.4.1 Saudi Arabia

- 5.4.2 United Arab Emirates

- 5.4.3 Egypt

- 5.4.4 Turkey

- 5.4.5 Morocco

- 5.4.6 Rest of Middle East and North Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 BK Gulf

- 6.4.2 ALEMCO

- 6.4.3 Al-Futtaim Engineering & Technologies

- 6.4.4 Khansaheb MEP

- 6.4.5 Adeeb Group

- 6.4.6 AG Engineering

- 6.4.7 Al Shafar United

- 6.4.8 Menasco Mechanical Contracting

- 6.4.9 Voltas Limited

- 6.4.10 Orascom Construction

- 6.4.11 International Electromechanical Services

- 6.4.12 Drake & Scull Engineering

- 6.4.13 ETA Engineering

- 6.4.14 KEO International Consultants

- 6.4.15 Dar Al-Handasah

- 6.4.16 Jacobs

- 6.4.17 AECOM

- 6.4.18 WSP Global

- 6.4.19 AtkinsRealis

- 6.4.20 Cundall

- 6.4.21 Buro Happold

- 6.4.22 Khatib & Alami

- 6.4.23 Johnson Controls Arabia

- 6.4.24 JLW Middle East

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment