PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064411

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064411

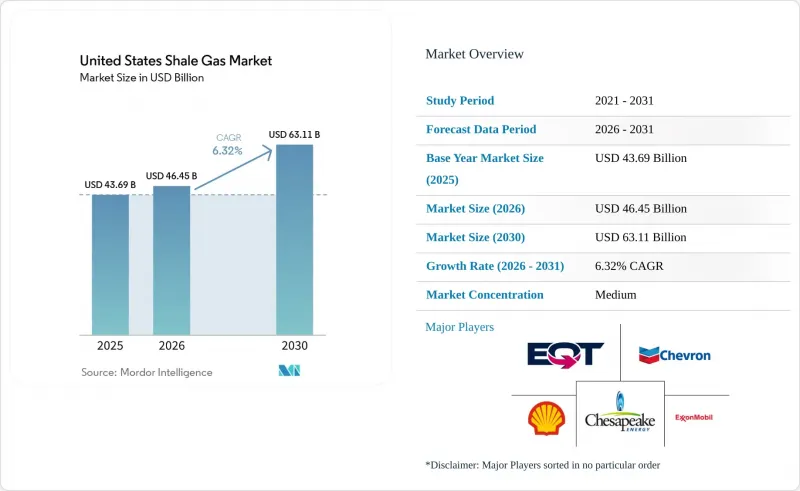

United States Shale Gas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states shale gas market size was valued at USD 43.69 billion in 2025 and is estimated to grow from USD 46.45 billion in 2026 to reach USD 63.11 billion by 2030, at a CAGR of 6.32% during the forecast period (2026-2030).

This report is Segmented by Hydrocarbon Type (Shale Gas, Shale Oil), Extraction Technology (Horizontal Drilling Only, Hydraulic Fracturing Only, Combined Horizontal and Hydraulic Fracturing), and Application (Power Generation, Industrial and Petrochemical Feedstock, Residential and Commercial Heating, Transportation). The Market Forecasts are Provided in Terms of Value (USD).

United States Shale Gas Market Trends and Insights

Robust LNG Export Capacity Additions Post-2026

Golden Pass LNG began service in early 2026 with 2.3 Bcf/d, while Cheniere's Corpus Christi Stage 3 expansion adds 2.7 Bcf/d by 2029. Together with Plaquemines and Calcasieu Pass, these projects absorb 7-8 Bcf/d of incremental supply, tightening balances and lifting Henry Hub from USD 2.21/MMBtu in 2024 to USD 3.52/MMBtu in 2025. The Federal Energy Regulatory Commission trimmed pre-construction timelines by up to 18 months, enabling faster final-investment decisions.

Rising Demand from Blue-Hydrogen Projects

Chevron's USD 5 billion Project Labrador in Baytown will consume 0.3 Bcf/d of gas when it reaches 1.2 million t/yr of low-carbon hydrogen capacity in 2027. Air Products' Louisiana complex follows a comparable scale. The Inflation Reduction Act's 45V credit of up to USD 3/kg steers investors toward gas-fed projects where pipeline CO2 storage is available.

Federal Leasing Pauses on Public Lands

BLM's Instruction Memorandum IM-2025-028 shortened parcel reviews to six months and reinstated quarterly sales, reversing an 80% decline in lease volumes between 2021 and 2024. The One Big Beautiful Bill Act locked in a 12.5% royalty floor, unlocking inventory in New Mexico and Wyoming for United States shale gas market participants.

Other drivers and restraints analyzed in the detailed report include:

- Depletion-Driven Shift from Conventional to Shale

- Growth in Data-Center Power-Purchase Agreements

- Escalating EPA Waste Emissions Charge

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Shale gas retained a 78.8% United States shale gas market share in 2025, but shale oil is expanding at a 6.8% CAGR through 2031 as Permian operators chase liquids-rich zones where breakevens sit below USD 40 per barrel. Devon Energy told investors in February 2026 that it would "stay as oily as we can," a stance that redirected rigs from the Haynesville to the Delaware Basin even though associated gas output still climbed 11% year over year to 27.7 Bcf/d. This pivot compressed the basin's gas-to-oil drilling ratio to 1:5 by early 2026, yet it did not erode total gas supply because liquids development inevitably lifts methane volumes. Appalachia's Marcellus and Utica formations remain almost entirely dry gas; EQT produced 6.2 Bcf/d in mid-2025 and locked 4.5 MTPA into long-term LNG contracts that hedge one-third of its output against spot volatility.

The liquids premium also influences capital flows outside the Permian. Chevron's USD 6.5 billion divestiture of Canadian oil sands and Duvernay shale assets in October 2024 freed cash for U.S. Permian drilling where infrastructure is ready and regulatory timelines are short. In contrast, Haynesville operators drilled deeper, higher-cost intervals only after Henry Hub recovered to USD 3.52/MMBtu in 2025, proving commodity prices still steer activity despite corporate statements about "disciplined growth". Even so, liquids-rich drilling narrows but does not eliminate the volume gap; dry-gas provinces continue to anchor the United States shale gas market size because of their low finding costs and existing pipeline networks. The result is a bifurcated supply stack in which dry-gas basins provide price stability while liquids-heavy plays offer margin upside during oil rallies.

List of Companies Covered in this Report:

- Exxon Mobil Corporation

- EQT Corporation

- Chesapeake Energy Corp.

- Chevron Corporation

- Shell plc

- ConocoPhillips Company

- Coterra Energy Inc.

- Southwestern Energy Co.

- Pioneer Natural Resources Co.

- Devon Energy Corporation

- EOG Resources Inc.

- Range Resources Corp.

- Antero Resources Corp.

- Continental Resources Inc.

- Marathon Oil Corporation

- Cabot Oil & Gas (now Coterra)

- Murphy Oil Corporation

- TotalEnergies SE

- Baker Hughes Company

- Schlumberger NV

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Robust LNG export capacity additions post-2026

- 4.2.2 Rising demand from blue-hydrogen projects

- 4.2.3 Depletion-driven shift from conventional to shale resources

- 4.2.4 Methane-intensity certification premiums

- 4.2.5 Digital twin-enabled well optimization

- 4.2.6 CO2-based fracturing gaining regulatory support

- 4.3 Market Restraints

- 4.3.1 Federal leasing pauses on public lands

- 4.3.2 Growing ESG-led capital flight

- 4.3.3 Persistent sand & water logistics bottlenecks

- 4.3.4 Community opposition in Appalachia

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Hydrocarbon Type

- 5.1.1 Shale Gas

- 5.1.2 Shale Oil

- 5.2 By Extraction Technology

- 5.2.1 Horizontal Drilling Only

- 5.2.2 Hydraulic Fracturing Only

- 5.2.3 Combined Horizontal and Hydraulic Fracturing

- 5.3 By Application

- 5.3.1 Power Generation

- 5.3.2 Industrial and Petrochemical Feedstock

- 5.3.3 Residential and Commercial Heating

- 5.3.4 Transportation (LNG and CNG)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Exxon Mobil Corporation

- 6.4.2 EQT Corporation

- 6.4.3 Chesapeake Energy Corp.

- 6.4.4 Chevron Corporation

- 6.4.5 Shell plc

- 6.4.6 ConocoPhillips Company

- 6.4.7 Coterra Energy Inc.

- 6.4.8 Southwestern Energy Co.

- 6.4.9 Pioneer Natural Resources Co.

- 6.4.10 Devon Energy Corporation

- 6.4.11 EOG Resources Inc.

- 6.4.12 Range Resources Corp.

- 6.4.13 Antero Resources Corp.

- 6.4.14 Continental Resources Inc.

- 6.4.15 Marathon Oil Corporation

- 6.4.16 Cabot Oil & Gas (now Coterra)

- 6.4.17 Murphy Oil Corporation

- 6.4.18 TotalEnergies SE

- 6.4.19 Baker Hughes Company

- 6.4.20 Schlumberger NV

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment