PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064463

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064463

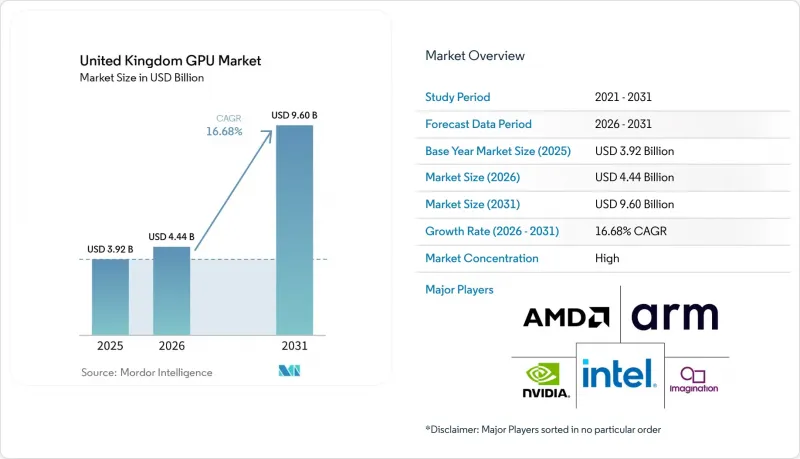

United Kingdom GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united kingdom gPU market size expanded from USD 3.92 billion in 2025 to USD 4.44 billion in 2026 and is projected to reach USD 9.60 billion by 2031, registering a 16.68% CAGR over 2026-2031.

This report is Segmented by Integration Type (Integrated GPUs, Discrete GPUs) and Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive/ADAS, Other Embedded and Edge Devices). The Market Forecasts are Provided in Terms of Value (USD).

United Kingdom GPU Market Trends and Insights

Surging demand for AI Training Accelerators in UK Data Centers

Hyperscale operators have booked up to 120,000 Blackwell-generation GPUs for United Kingdom facilities by late 2026, with one provider alone targeting 60,000 Grace Blackwell units. Public-sector projects such as Isambard-AI and Dawn upgrades illustrate the government's resolve to anchor sovereign compute domestically, while economic studies suggest even modest capacity additions could inject billions of pounds into annual GDP.

UK Sovereign-AI Initiatives Fueling domestic GPU Clusters

The 2025 AI Growth Zones Initiative streamlines planning approvals and grid connections, pairing fiscal incentives with a GBP 1 billion public investment and a GBP 1.5 billion industry pledge from the Sovereign AI Industry Forum. These measures shorten project lead times, steer workloads to regions rich in renewable potential, and create a policy backstop that underwrites long-cycle capital commitments.

Persistent Global GPU Supply Chain Constraints and Elevated Pricing

High-bandwidth memory shortages and year-long advanced-node lead times force enterprises to lock in allocations far ahead of deployment, inflate street prices of flagship cards to USD 3,500-4,000, and delay AI projects across finance and healthcare by several quarters.

Other drivers and restraints analyzed in the detailed report include:

- Enterprise adoption of GPU-Accelerated Analytics and HPC

- Growth of Cloud Gaming and Esports Ecosystem

- High Power and Cooling Costs In UK Data Centers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Discrete accelerators captured 62.73% of the total value in 2025 as enterprises gravitated toward modular architectures suited for large-scale transformer training. The segment benefits from continual core-count increases, higher bandwidth memory, and software ecosystems tightly coupled to proprietary toolchains, effectively making the United Kingdom GPU market the proving ground for efficiency-ranked datacenter designs.

Integrated graphics continue to climb in mobile devices, strengthened by next-generation system-on-chips from Apple and AMD. While these embedded units will not displace discrete cards in multi-petaflop clusters, they satisfy everyday productivity and 1080p gaming, thereby lengthening consumer replacement cycles. The shift tempers unit volume for entry-level boards but raises the premium-tier average selling price, sustaining overall revenue momentum within the United Kingdom GPU market.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Imagination Technologies Limited

- Arm Limited

- Qualcomm Technologies, Inc.

- Samsung Electronics Co., Ltd.

- Apple Inc.

- Graphcore Limited

- Tenstorrent Inc.

- Sapphire Technology Limited

- ASUStek Computer Inc.

- Micro-Star International Co., Ltd.

- Gigabyte Technology Co., Ltd.

- Palit Microsystems Ltd.

- Zotac International (MCO) Ltd.

- Gainward Co., Ltd.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for AI Training Accelerators in UK Data Centers

- 4.2.2 Growth of Cloud Gaming and eSports Ecosystem

- 4.2.3 Enterprise Adoption of GPU-Accelerated Analytics and HPC

- 4.2.4 Expansion of Autonomous Vehicle R&D and ADAS Programs

- 4.2.5 UK Sovereign-AI Initiatives Fueling Domestic GPU Clusters

- 4.2.6 Shift Toward On-Device Inference for Privacy Compliance

- 4.3 Market Restraints

- 4.3.1 Persistent Global GPU Supply Chain Constraints and Elevated Pricing

- 4.3.2 High Power and Cooling Costs in UK Data Centers

- 4.3.3 Talent Shortage in GPU Programming and CUDA Expertise

- 4.3.4 Regulatory Scrutiny on AI Energy Use and Carbon Emissions

- 4.4 Industry Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Integration Type

- 5.1.1 Integrated GPUs (iGPU)

- 5.1.2 Discrete GPUs (dGPU)

- 5.2 By Device Application

- 5.2.1 Mobile Devices and Tablets

- 5.2.2 PCs and Workstations

- 5.2.3 Servers and Datacenter Accelerators

- 5.2.4 Gaming Consoles and Handhelds

- 5.2.5 Automotive / ADAS

- 5.2.6 Other Embedded and Edge Devices

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Imagination Technologies Limited

- 6.4.5 Arm Limited

- 6.4.6 Qualcomm Technologies, Inc.

- 6.4.7 Samsung Electronics Co., Ltd.

- 6.4.8 Apple Inc.

- 6.4.9 Graphcore Limited

- 6.4.10 Tenstorrent Inc.

- 6.4.11 Sapphire Technology Limited

- 6.4.12 ASUStek Computer Inc.

- 6.4.13 Micro-Star International Co., Ltd.

- 6.4.14 Gigabyte Technology Co., Ltd.

- 6.4.15 Palit Microsystems Ltd.

- 6.4.16 Zotac International (MCO) Ltd.

- 6.4.17 Gainward Co., Ltd.

- 6.4.18 Dell Technologies Inc.

- 6.4.19 Hewlett Packard Enterprise Company

7 MARKET OPPORTUNITIES & FUTURE OUTLOOK

- 7.1 White-space & Unmet-Need Assessment