PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064471

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064471

U.S. Medical Tapes And Bandages - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

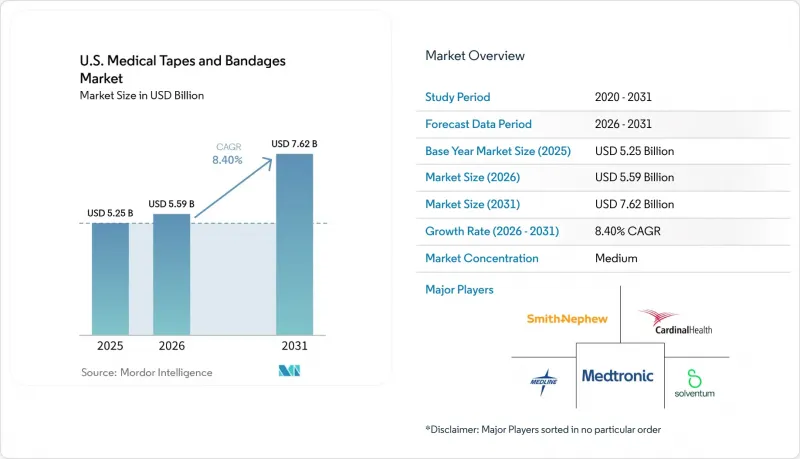

According to Mordor Intelligence, the u.S. medical tapes and bandages market size is expected to grow from USD 5.25 billion in 2025 to USD 5.59 billion in 2026 and is forecast to reach USD 7.62 billion by 2031 at 8.40% CAGR over 2026-2031.

This report is Segmented by Product (Medical Tapes, Dressings, Bandages), Application (Surgical Wounds, Traumatic Wounds, Ulcers, Sports Injuries, Burns, Others), End User (Hospitals, Ascs, Clinics, Home Healthcare, LTC/SNFs, Retail, Military), and Distribution Channel (Distributors, Direct Sales, and More). The Market Forecasts are Provided in Terms of Value (USD).

U.S. Medical Tapes And Bandages Market Trends and Insights

Chronic Wound and Diabetes Burden Creating Persistent Volume Demand

The United States medical tapes and bandages market experiences steady demand due to the high prevalence of chronic wounds and diabetes. In 2025, chronic wounds impacted 10.5 million Medicare beneficiaries, generating USD 22.5 billion in annual care costs, with wound dressings comprising a significant share. Additionally, 53.1 million Americans with diabetes faced a 15%-34% lifetime risk of diabetic foot ulcers, driving recurring demand for securement tapes, bordered dressings, and bandage systems. These products are consumed over extended treatment cycles, ensuring consistent demand despite reimbursement challenges.

High Surgical and ASC Procedure Volumes Sustaining Core Tape and Bandage Demand

The United States medical tapes and bandages market benefits from the growing shift of procedures to ambulatory surgery centers (ASCs). In 2024, 6,436 Medicare-certified ASCs performed 6.4 million fee-for-service Medicare procedures, with a 3.5% year-over-year increase in procedure volume per 1,000 beneficiaries. Rising total knee and hip arthroplasty volumes, along with the 2026 ASC Covered Procedure List expansion adding 560 procedures, further boost demand for wound covering and securement products in outpatient settings.

2026 CMS Payment Reset Reshaping Office Wound Care Economics

The United States medical tapes and bandages market is experiencing a major payment shift in office-based wound care. Under the CY 2026 Physician Fee Schedule final rule, CMS reclassified several skin substitutes as "incident-to" supplies and introduced a flat national payment rate of USD 127.28 per square centimeter, replacing the previous ASP+6% structure that allowed reimbursements exceeding USD 2,000 per square centimeter. This change is expected to reduce gross Medicare fee-for-service spending on skin substitute services by USD 19.6 billion in 2026, significantly altering advanced wound treatment economics. While physician offices may shift toward conventional wound products, the disruption could delay product decisions as workflows adjust, creating short-term uncertainty in purchasing behavior.

Other drivers and restraints analyzed in the detailed report include:

- Wearable Medical Devices Redefining Adhesive Tape Specifications

- Payer-Driven Home Care Migration Expanding Alternate-Site Product Needs

- GPO Consolidation Compressing Institutional Tape and Bandage Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Medical Bandages accounted for 38.45% of revenue, leading the United States medical tapes and bandages market. Their dominance stems from extensive use in post-operative care, compression support, first-aid treatment, and routine wound covering across hospitals, ASCs, physician offices, retail stores, and homes. Serving both institutional and consumer needs, bandages maintain stable demand across clinical and over-the-counter channels.

Medical Tapes, the fastest-growing segment, is projected to achieve an 8.25% CAGR from 2026 to 2031. Growth is driven by increased adoption of CGMs, insulin pumps, and advanced tape formats like transparent film securement and silicone tapes. Enhanced focus on adhesion, skin tolerance, and removal comfort is driving innovation in this segment.

Surgical wounds contributed 35.66% of revenue in 2025, making them the largest application in the United States medical tapes and bandages market. This is linked to the high volume of outpatient and ambulatory procedures requiring post-treatment care, creating consistent demand for tapes, dressings, and bandages.

Ulcer Treatment, the fastest-growing application, is expected to post a 7.95% CAGR from 2026 to 2031. Growth is fueled by the diabetic population and demand for conventional wound care in managing diabetic, pressure, and venous ulcers. CMS payment changes in 2026 are further driving demand for foam dressings and securement tapes.

List of Companies Covered in this Report:

- AERO Healthcare

- B. Braun

- Cardinal Health

- Coloplast

- Convatec Group plc

- DeRoyal Industries

- Dukal

- Dynarex

- Essity Health & Medical

- HALYARD

- Hartmann Group

- Integra LifeSciences

- Kenvue Brands LLC

- Mckesson

- Medline Industries

- Medtronic

- Molnlycke Health Care

- Smiths Group

- Solventum Corporation

- Urgo Medical North America LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Chronic Wound and Diabetes Burden

- 4.2.2 High Surgical and ASC Procedure Volumes

- 4.2.3 Aging Patient Mix and Pressure Injury Risk

- 4.2.4 Shift Toward Home and Alternate-Site Wound Care

- 4.2.5 Adhesive Securement Demand from CGMs, Insulin Pumps, and Other Wearables

- 4.2.6 CMS Site-of-Care and Supply Reimbursement Mechanics Favor Efficient, Easy-Apply Products

- 4.3 Market Restraints

- 4.3.1 MARSI and Skin Irritation Risk

- 4.3.2 Pricing Pressure from GPOS and Distributor Consolidation

- 4.3.3 2026 Skin-Substitute Payment Reset Disrupting Office Wound-Care Purchasing

- 4.3.4 Routine-Vs-Nonroutine Supply Reimbursement Complexity in Home Care

- 4.4 Supply/Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Medical Tapes

- 5.1.1.1 Paper Tapes

- 5.1.1.2 Fabric Tapes

- 5.1.1.3 Plastic Tapes

- 5.1.1.4 Silicone / Acrylic / Rubber Tapes

- 5.1.1.5 Transparent Film / Dressing Retention Tapes

- 5.1.1.6 Elastic / Waterproof / Specialty Tapes

- 5.1.2 Dressings

- 5.1.2.1 Foam Dressings

- 5.1.2.2 Hydrocolloid Dressings

- 5.1.2.3 Film Dressings

- 5.1.2.4 Alginate Dressings

- 5.1.2.5 Hydrogel Dressings

- 5.1.2.6 Collagen Dressings

- 5.1.2.7 Superabsorbent Dressings

- 5.1.2.8 Antimicrobial Dressings

- 5.1.2.9 Other Advanced Dressings

- 5.1.3 Medical Bandages

- 5.1.3.1 Adhesive Bandages / First Aid Bandages

- 5.1.3.2 Gauze Bandage Rolls

- 5.1.3.3 Elastic Bandage Rolls

- 5.1.3.4 Cohesive / Self-Adherent Bandages

- 5.1.3.5 Conforming Bandages

- 5.1.3.6 Triangular Bandages

- 5.1.3.7 Orthopedic / Cast Bandages

- 5.1.3.8 Others

- 5.1.1 Medical Tapes

- 5.2 By Application

- 5.2.1 Surgical Wounds

- 5.2.2 Traumatic Wounds

- 5.2.3 Ulcers Treatment

- 5.2.4 Sports Injuries

- 5.2.5 Burn Injuries

- 5.2.6 Sport Injuries

- 5.2.7 Others

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgery Centers

- 5.3.3 Clinics and Physician Offices

- 5.3.4 Home Healthcare

- 5.3.5 Long-Term Care and Skilled Nursing Facilities

- 5.3.6 Retail / Consumer Self-Care

- 5.3.7 Military and Emergency Care

- 5.4 By Distribution Channel

- 5.4.1 Distributors

- 5.4.2 Direct Sales / Enterprise Contracts

- 5.4.3 Retail Pharmacies

- 5.4.4 E-commerce / Online Medical Supply

- 5.4.5 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AERO Healthcare

- 6.3.2 B. Braun SE

- 6.3.3 Cardinal Health Inc.

- 6.3.4 Coloplast A/S

- 6.3.5 Convatec Group plc

- 6.3.6 DeRoyal Industries Inc.

- 6.3.7 Dukal

- 6.3.8 Dynarex

- 6.3.9 Essity Health & Medical

- 6.3.10 HALYARD

- 6.3.11 HARTMANN USA, Inc.

- 6.3.12 Integra LifeSciences Holdings Corporation

- 6.3.13 Kenvue Brands LLC

- 6.3.14 McKesson Corporation

- 6.3.15 Medline Industries Inc.

- 6.3.16 Medtronic plc

- 6.3.17 Molnlycke Health Care AB

- 6.3.18 Smith & Nephew plc

- 6.3.19 Solventum Corporation

- 6.3.20 Urgo Medical North America LLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment