PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064503

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064503

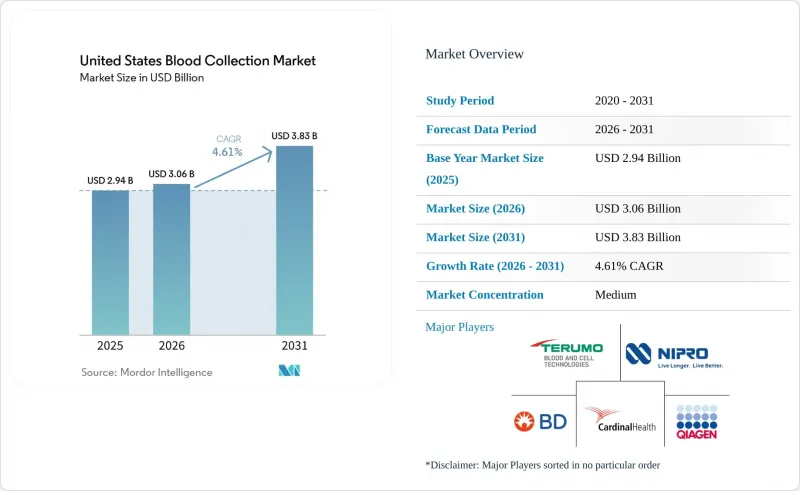

United States Blood Collection - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states blood collection market size is expected to grow from USD 2.94 billion in 2025 to USD 3.06 billion in 2026 and is forecast to reach USD 3.83 billion by 2031 at 4.61% CAGR over 2026-2031.

This report is Segmented by Product Type (Tubes, Needles and Sets, Blood Bags, Lancets, Collection Systems), Site of Collection (Venous, Capillary), Method (Manual, Automated), Application (Diagnostics, Transfusion Support, Research), End Use (Hospitals, Laboratories, Blood Banks, Physician Offices), and Geography (United States). The Market Forecasts are Provided in Terms of Value (USD).

United States Blood Collection Market Trends and Insights

Rising Chronic Disease Diagnostic Volumes

The strongest long-cycle demand support for the blood collection market comes from the continued burden of chronic disease across the adult population. CDC reporting showed that multiple chronic conditions remained widespread among U.S. adults and that the rise extended into younger age groups, which means diagnostic monitoring begins earlier and continues for longer periods across the care journey. That shift matters because patients with diabetes, obesity, cardiovascular risk, and mental health conditions often move into recurring laboratory schedules that require specimen collection across primary care, specialist visits, and ambulatory settings. The blood collection market, therefore, benefits from volume durability rather than one-time spikes, since every additional monitored condition raises the likelihood of repeated blood draws during routine care. Cancer care adds another layer of recurring need because blood products are heavily used in oncology treatment pathways and supportive care. This demand pattern gives suppliers a stable base for tubes, needles, lancets, collection sets, and related consumables, even when broader healthcare spending conditions become less predictable.

Sustained Blood Donation and Transfusion Support Needs

The blood collection market also draws support from the ongoing need to maintain a functioning national blood supply. America's Blood Centers reported that more than 15 million blood products were transfused in the United States and that transfusions continue at a very high daily rate, which keeps collection activity essential for hospitals and community blood networks. AABB findings also showed that collection mix is moving toward apheresis-based component collection, with platelet distribution now heavily dependent on apheresis formats and related disposable sets. That shift changes the economics of procurement because automated component collection uses specialized hardware, software, and high-value consumables rather than lower-value whole-blood supplies alone. Low donor participation continues to keep the system tight, which means blood centers need dependable collection infrastructure and strong donor throughput to meet hospital demand. As a result, the blood collection market gains support not only from diagnostic testing but also from the persistent operational need to secure enough donated blood and blood components for clinical use.

Phlebotomy and Laboratory Staffing Shortages

Workforce limitations remain a material constraint on how much collection capacity the blood collection market can convert into realized volume. The U.S. Bureau of Labor Statistics expects phlebotomist employment to grow 6% from 2024 to 2034, which signals that demand for draw capacity is rising faster than many providers can staff today. The Medical and Public Health Laboratory Workforce Coalition also reported a training pipeline that remains well below the level needed to fill projected annual openings across the laboratory workforce. When staffing stays tight, facilities face slower throughput, delayed specimen processing, and less flexibility to absorb peaks in diagnostic demand or donor center traffic. That pushes some institutions toward automation and workflow redesign, but it does not fully remove the near-term capacity pressure created by too few trained workers. The result is that the blood collection market has strong underlying demand, yet parts of that demand remain operationally constrained by labor availability in hospitals, laboratories, and mobile services.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Safety-Engineered Collection Devices

- At-Home and Decentralized Microsampling Expansion

- Intermittent Collection-Container Supply Disruptions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Blood collection tubes held 34.78% of the blood collection market share in 2025, which reflected their central role in routine venipuncture across hospitals, clinics, and laboratories. Serum separation and plain serum tubes continued to support a large share of everyday chemistry and immunoassay workflows, while EDTA tubes remained important for hematology and selected molecular applications. Citrate tubes also stayed relevant in coagulation testing, especially in cardiovascular and thrombosis care pathways where repeat monitoring remains common. Heparin and plasma-oriented formats gained support in testing environments where plasma stability and turnaround efficiency matter for clinical decision making. This broad utility keeps tubes at the core of the blood collection market because they serve the largest installed base of collection and laboratory workflows.

Lancets and capillary micro-collection are projected to grow at 5.47% CAGR through 2031, making them the fastest-expanding product sub-segment in the United States blood collection market. Their growth is tied to safety lancets, micro-containers, and dried blood spot kits that fit self-collection, outpatient convenience, and decentralized programs. Truvian's 2025 FDA clearance showed that small-volume capillary samples can support a wider menu of testing in compact settings, which strengthens the case for broader adult adoption of microsampling devices. Tasso's 2025 collaboration with ARUP Laboratories also supported assay validation from capillary microsamples, which helps move capillary collection from limited-use cases toward more routine workflows. As this product mix broadens, tubes are likely to retain scale leadership, while capillary formats supply much of the incremental growth in the blood collection market.

Venous collection accounted for 40.57% of revenue in 2025, which kept it as the leading site of collection across the United States blood collection market. That position reflects the continued need for larger specimen volumes in inpatient diagnostics, outpatient testing, donor collection, and apheresis procedures. Venous workflows remain deeply embedded in clinical operations because they support broad analyte menus, high-throughput phlebotomy, and compatibility with established laboratory instruments. OSHA rules and the Needlestick Safety and Prevention Act also support recurring replacement of venous access hardware with safer designs, which sustains procurement activity around needles and winged sets. For large hospitals and diagnostic networks, venous collection remains the default route wherever volume, standardization, and menu breadth outweigh convenience considerations.

Capillary collection is expected to grow at 5.28% CAGR through 2031, making it the fastest-rising site sub-segment in the blood collection market size outlook. Its growth reflects stronger acceptance of fingerstick and pediatric home collection in settings where venipuncture is less practical or less desirable. The 2026 RedDrop ONE study showed that parent-administered capillary collection can work across varied geographies with overnight ambient shipping to a CLIA-certified lab, which gives the model real operational relevance beyond pilot settings. Tasso and ARUP Laboratories also demonstrated broader assay validation potential for decentralized microsampling, which improves confidence in capillary workflows for research and monitored care use cases. Capillary collection is unlikely to displace venous methods at scale in the near term, but it is reshaping how the United States blood collection market reaches patients outside traditional draw sites.

List of Companies Covered in this Report:

- Beckton Dickinson

- Greiner Bio One International

- Terumo Blood and Cell Technologies

- Fresenius

- Cardinal Health

- Haemonetics

- Nipro

- Sarstedt

- QIAGEN

- Streck, Inc.

- Tasso, Inc.

- Magnolia Medical Technologies

- Medline Industries

- Drawbridge Health, Inc.

- Trajan Scientific and Medical

- Thermo Fisher Scientific

- ICU Medical

- Retractable Technologies

- Exel International, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Chronic Disease Diagnostic Volumes

- 4.2.2 High Blood Testing Intensity Across Hospitals and Labs

- 4.2.3 Sustained Blood Donation and Transfusion Support Needs

- 4.2.4 Shift Toward Safety-Engineered Collection Devices

- 4.2.5 Adult Fingertip Collection Moving into Routine Testing

- 4.2.6 At-Home and Decentralized Microsampling Expansion

- 4.3 Market Restraints

- 4.3.1 Donor Participation and Deferral Limitations

- 4.3.2 Specimen Contamination and Pre-Analytical Error Risk

- 4.3.3 Phlebotomy and Laboratory Staffing Shortages

- 4.3.4 Intermittent Collection-Container Supply Disruptions

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Blood collection tubes

- 5.1.1.1 Serum separation and plain serum tubes

- 5.1.1.2 Plasma and heparin tubes

- 5.1.1.3 EDTA tubes

- 5.1.1.4 Citrate and coagulation tubes

- 5.1.1.5 ESR and specialty analyte-preservation tubes

- 5.1.2 Blood collection needles and sets

- 5.1.2.1 Multi-sample needles

- 5.1.2.2 Winged blood collection sets

- 5.1.2.3 Holders and luer adapters

- 5.1.3 Blood bags and whole-blood collection disposables

- 5.1.3.1 Whole-blood bag systems

- 5.1.3.2 Leukoreduction and sampling accessories

- 5.1.4 Lancets and capillary micro-collection

- 5.1.4.1 Safety lancets

- 5.1.4.2 Micro-containers and micro-hematocrit tubes

- 5.1.4.3 Dried blood spot and microsampling kits

- 5.1.5 Collection systems and accessories

- 5.1.5.1 Blood transfer devices

- 5.1.5.2 Specimen-diversion and blood-culture collection systems

- 5.1.5.3 Manual collection monitors and mixers

- 5.1.5.4 Automated apheresis and component-collection systems

- 5.1.1 Blood collection tubes

- 5.2 By Site of Collection

- 5.2.1 Venous

- 5.2.1.1 Diagnostic venipuncture

- 5.2.1.2 Donor whole-blood and component collection

- 5.2.2 Capillary

- 5.2.2.1 Fingerstick sampling

- 5.2.2.2 Heelstick and pediatric sampling

- 5.2.1 Venous

- 5.3 By Method

- 5.3.1 Manual blood collection

- 5.3.1.1 Standard venipuncture workflows

- 5.3.1.2 Manual donor whole-blood collection

- 5.3.2 Automated blood collection

- 5.3.2.1 Apheresis and component collection

- 5.3.2.2 Assisted automated sample-preparation workflows

- 5.3.1 Manual blood collection

- 5.4 By Application

- 5.4.1 Diagnostics

- 5.4.1.1 Clinical chemistry and immunoassay testing

- 5.4.1.2 Hematology and coagulation testing

- 5.4.1.3 Infectious disease testing

- 5.4.1.4 Molecular, genomic, and liquid biopsy testing

- 5.4.2 Treatment and transfusion support

- 5.4.2.1 Whole-blood donation

- 5.4.2.2 Component collection and transfusion support

- 5.4.3 Research and clinical trials

- 5.4.3.1 Biobanking and translational research

- 5.4.3.2 Decentralized sample-collection studies

- 5.4.1 Diagnostics

- 5.5 By End Use

- 5.5.1 Hospitals

- 5.5.2 Clinical and diagnostic laboratories

- 5.5.3 Blood banks and blood centers

- 5.5.4 Physician offices and ambulatory care centers

- 5.5.5 Emergency departments and mobile services

- 5.5.6 Academic and research institutes

- 5.5.7 Home and decentralized collection programs

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Becton, Dickinson and Company

- 6.3.2 Greiner Bio-One International GmbH

- 6.3.3 Terumo Blood and Cell Technologies

- 6.3.4 Fresenius Kabi AG

- 6.3.5 Cardinal Health, Inc.

- 6.3.6 Haemonetics Corporation

- 6.3.7 Nipro Medical Corporation

- 6.3.8 SARSTEDT AG & Co. KG

- 6.3.9 QIAGEN N.V.

- 6.3.10 Streck, Inc.

- 6.3.11 Tasso, Inc.

- 6.3.12 Magnolia Medical Technologies

- 6.3.13 Medline Industries, LP

- 6.3.14 Drawbridge Health, Inc.

- 6.3.15 Trajan Scientific and Medical

- 6.3.16 Thermo Fisher Scientific Inc.

- 6.3.17 ICU Medical, Inc.

- 6.3.18 Retractable Technologies, Inc.

- 6.3.19 Exel International, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment