PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064522

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064522

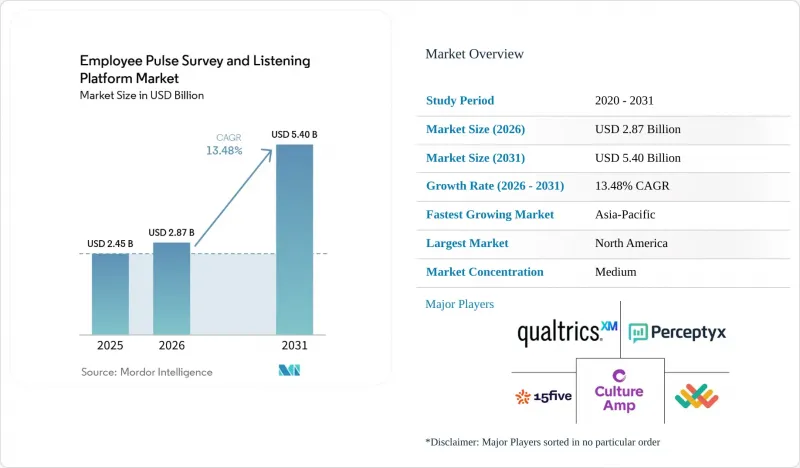

Employee Pulse Survey And Listening Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the employee pulse survey and listening platform market size is projected to be USD 2.45 billion in 2025, USD 2.87 billion in 2026, and reach USD 5.40 billion by 2031, growing at a CAGR of 13.48% from 2026 to 2031.

This report is Segmented by Component (Platform/Software and Services), Deployment Mode (Cloud-Based, and More), Enterprise Size (Large Enterprises and Small and Medium-Sized Enterprises), Capability (Engagement and Pulse Surveys, and More), End-User Industry (BFSI, Healthcare and Life Sciences and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Employee Pulse Survey And Listening Platform Market Trends and Insights

Ai-Powered Sentiment Analytics And Predictive Insights

Large language models are changing the employee pulse survey and listening platform market from a passive collection layer into a more active workforce intelligence system. Open-text analysis now helps vendors flag burnout signals, attrition risk, and manager-specific next steps without relying on manual interpretation at every step. That change matters because shorter pulse formats can still produce useful themes, reducing dependence on long surveys and helping counter survey fatigue. In the employee pulse survey and listening platform market, AI is also becoming a key metric, as employee sentiment around automation now affects trust, readiness, and adoption. Gallup reported in April 2026 that manager support for AI tools was the strongest predictor of employee AI adoption, which tied listening capability more closely to broader productivity agendas.

Expansion Of Hybrid And Remote Work Models

Hybrid and remote work now function as a structural part of workforce design rather than a temporary operating model. That shift has made technology-mediated listening much more important because distributed teams lose many of the informal signals that managers once picked up in person. Annual engagement surveys don't fit well in this setting because team composition, workload levels, and manager relationships change too often for a single annual snapshot to remain useful. The employee pulse survey and listening platform market is benefiting from this pattern because buyers increasingly want mobile-first, asynchronous delivery that reaches people inside collaboration tools instead of asking them to log in to a separate system. ManpowerGroup Deutschland reported in January 2026 that 58% of German employees showed burnout symptoms, while 65% planned to stay with their employer and 54% were still searching for new roles, underscoring the need for continuous listening to become more operationally relevant.

Data Privacy, Anonymity, And Cross-Border Compliance Concerns

Privacy regulation remains one of the hardest operating constraints in the employee pulse survey and listening platform market. GDPR can impose fines of up to EUR 20 million (USD 22.6 million) or 4% of global annual turnover for violations of core processing rules, so vendors and employers need much tighter controls around employee feedback data. The practical challenge is that surveys marketed as anonymous can still become re-identifiable when teams are small or when demographic filters and timestamp data are combined. In March 2026, it was noted that employee survey programs have to address consent, demographics, processors, and anonymity thresholds carefully under GDPR, which shows how governance has become part of product design rather than just legal review. The result is longer buying cycles, tighter vendor scrutiny, and stronger demand for regional hosting, threshold controls, and configurable data retention rules.

Other drivers and restraints analyzed in the detailed report include:

- Rising Enterprise Focus On Employee Engagement And Retention

- Growth Of Cloud-Native Hr Technology Stacks

- Survey Fatigue And Declining Response Quality

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Platform/software held 71.20% of the employee pulse survey and listening platform market size in 2025, while services are forecast to expand at a 15.23% CAGR through 2031. Software remained the core layer of spending because it manages survey delivery, dashboarding, benchmarking, and analytics at scale. It also serves as the daily system through which employees and managers interact, so most initial buying decisions still center on the platform itself. Even so, services are growing faster because many HR teams lack the time or in-house capability to translate listening data into manager-ready actions across large organizations.

Services demand is being pulled by implementation work, analytics consulting, action-planning support, and ongoing program management. These revenue streams are also stickier than software-only subscriptions because the vendor relationship extends into governance, interpretation, and change execution. In the employee pulse survey and listening platform market, that matters because buyers increasingly want help closing the gap between measurement and visible manager response. Leapsome's May 2026 move to a broader HRIS model followed the same logic, tying engagement data to payroll, absence management, and performance records within a single operating environment. The employee pulse survey and listening platform industry is therefore placing greater value on services that convert data into workflow changes rather than just producing another reporting layer.

Cloud-based deployment commanded a 68.45% share in 2025, while hybrid deployment is expected to grow at a 14.89% CAGR through 2031. Cloud remained the default choice because it supports rapid provisioning, continuous updates, lower maintenance burden, and easier access for distributed teams. It also aligns with the delivery model of most SaaS-based HR software, which makes procurement and rollout simpler for many employers. These advantages kept the cloud at the center of new deployments across multinational and mid-market accounts.

Hybrid deployment is growing because large regulated employers need cloud analytics and modern interfaces without sacrificing control over sensitive employee data. In the employee pulse survey and listening platform market, hybrid is not just a bridge toward full cloud adoption. It is a stable destination for BFSI, healthcare, public sector, and other organizations dealing with overlapping data residency and internal security rules. On-premises still matters when workforce data cannot be processed by third-party clouds under existing policy or security controls. As the employee pulse survey and listening platform market matures, deployment flexibility is becoming a buying criterion in its own right because switching costs rise once governance and infrastructure are set.

Geography Analysis

North America held 40.05% of the employee pulse survey and listening platform market size in 2025, while Asia-Pacific is forecast to grow at a 16.89% CAGR through 2031. North America remained the largest revenue pool because HR technology adoption is mature and many large employers already operate dedicated people analytics functions. Employee engagement in the United States and Canada stood at 31% in 2025, the highest among measured regions, but daily stress also reached 50%, which keeps demand for better listening infrastructure elevated. Canada and Mexico are also adding demand as adoption becomes more locally driven and less dependent on U.S. headquarters-led rollouts. The employee pulse survey and listening platform market in North America benefits from both scale and a stronger tendency to connect people data with business performance.

Europe remains strategically important in the employee pulse survey and listening platform market because compliance rules and buying decisions are closely linked. Workforce disclosure pressure under CSRD is making well-governed listening data more valuable for public companies that need repeatable reporting across multiple entities. Employee engagement in Europe was 12% in 2025 for the fifth straight year, which left the region with the lowest engagement level globally and a large improvement opportunity for well-executed platforms. EU-based vendors can hold an advantage when employers prioritize regional hosting, works council familiarity, and GDPR-aligned configuration.

Asia-Pacific is the fastest-growing geography in the employee pulse survey and listening platform market, supported by HR digitization in India, China, Japan, South Korea, and Australia. Multinational expansion across linguistically diverse workforces is also raising demand for multilingual delivery and centralized oversight. South America, the Middle East, and Africa remain smaller but increasingly relevant as domestic groups and multinational subsidiaries standardize workforce systems and adopt smartphone-first survey channels. Within this broader expansion, the employee pulse survey and listening platform market is gaining traction in regions where mobile delivery solves earlier access barriers and where workforce formalization is still progressing.

- Qualtrics, LLC

- Culture Amp Pty Ltd

- 15Five, Inc.

- Degree, Inc. d/b/a Lattice

- Perceptyx, Inc.

- Quantum Workplace, Inc.

- Leapsome GmbH

- WorkTango, Inc.

- Energage, LLC

- Effectory B.V.

- Explorance Inc.

- EngageRocket Pte. Ltd.

- CultureMonkey Private Limited

- Workleap Software Inc.

- Achievers Solutions Inc.

- SurveySparrow Inc.

- Betterworks System Inc.

- Synergita Software Private Limited

- LutherOne a.s.

- Bargain Technologies Private Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Hybrid and Remote Work Models

- 4.2.2 Rising Enterprise Focus on Employee Engagement and Retention

- 4.2.3 AI-Powered Sentiment Analytics and Predictive Insights

- 4.2.4 Growth of Cloud-Native HR Technology Stacks

- 4.2.5 Multilingual and Frontline-Friendly Survey Delivery

- 4.2.6 Human Capital Disclosure and Well-Being Governance Requirements

- 4.3 Market Restraints

- 4.3.1 Data Privacy, Anonymity, and Cross-Border Compliance Concerns

- 4.3.2 Survey Fatigue and Declining Response Quality

- 4.3.3 Manager Actionability Gap After Survey Cycles

- 4.3.4 Bundling Pressure from HCM Suites and Price Compression

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Platform/Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By End User Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-sized Enterprises

- 5.4 By Capability

- 5.4.1 Engagement and Pulse Surveys

- 5.4.2 Lifecycle Listening

- 5.4.3 Sentiment Analytics and Text Intelligence

- 5.4.4 Action Planning and Manager Enablement

- 5.4.5 Other Capabilities

- 5.5 By End User Industry

- 5.5.1 BFSI

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Information Technology and Telecom

- 5.5.4 Retail and E-commerce

- 5.5.5 Industrial Manufacturing

- 5.5.6 Government and Public Sector

- 5.5.7 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Netherlands

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Qualtrics, LLC

- 6.4.2 Culture Amp Pty Ltd

- 6.4.3 15Five, Inc.

- 6.4.4 Degree, Inc. d/b/a Lattice

- 6.4.5 Perceptyx, Inc.

- 6.4.6 Quantum Workplace, Inc.

- 6.4.7 Leapsome GmbH

- 6.4.8 WorkTango, Inc.

- 6.4.9 Energage, LLC

- 6.4.10 Effectory B.V.

- 6.4.11 Explorance Inc.

- 6.4.12 EngageRocket Pte. Ltd.

- 6.4.13 CultureMonkey Private Limited

- 6.4.14 Workleap Software Inc.

- 6.4.15 Achievers Solutions Inc.

- 6.4.16 SurveySparrow Inc.

- 6.4.17 Betterworks System Inc.

- 6.4.18 Synergita Software Private Limited

- 6.4.19 LutherOne a.s.

- 6.4.20 Bargain Technologies Private Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment