PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064538

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064538

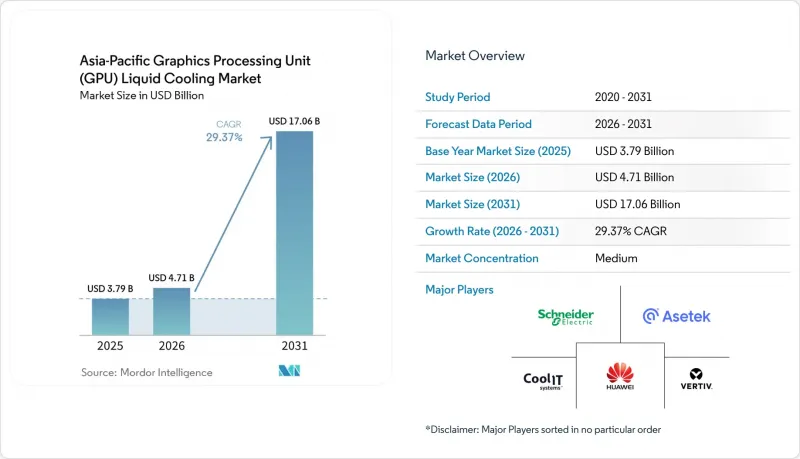

Asia-Pacific Graphics Processing Unit (GPU) Liquid Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the asia-Pacific graphics processing unit (GPU) liquid cooling market size is expected to grow from USD 3.79 billion in 2025 to USD 4.71 billion in 2026 and is forecast to reach USD 17.06 billion by 2031 at 29.37% CAGR over 2026-2031.

This report is Segmented by Cooling Type (Single-Phase Liquid Cooling, and Two-Phase Liquid Cooling), Cooling Level (Component-Level Cooling, and Server/Rack-Level Cooling), Deployment (Hyperscale/Cloud, Enterprise, Edge AI, and More), GPU Power Density (Below 300W, 300W-700W, and Above 700W), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Graphics Processing Unit (GPU) Liquid Cooling Market Trends and Insights

Mainstream AI-Led Hyperscale Expansions Drive Liquid-Cooling Adoption

Alibaba, Samsung SDS, OpenAI, and Global Switch are commissioning facilities where racks surpass 100 kilowatts, and GPUs draw up to 1,200 watts, a regime that renders air cooling uneconomic. Alibaba's Feitian platform already operates more than 100,000 GPUs in immersion tanks at PUE 1.09, cutting facility energy bills by roughly one-half. Samsung SDS broke ground on a 60 megawatt AI campus in Gumi in March 2026 that allocates KRW 427.3 billion (USD 320 million) to hybrid liquid infrastructure, underscoring long-term confidence in direct-to-chip systems. Global Switch Hong Kong added 30 megawatts of liquid-cooled capacity, while Nxera's DC Tuas in Singapore installed 58 megawatts of warm-water loops for sovereign AI workloads. The Asia-Pacific GPU liquid cooling market, therefore, follows hyperscalers' cadence: as model sizes inflate, cooling budgets shift from optimization to outright replacement of air systems.

Mandatory Energy-Efficiency Regulations Across East and South-East Asia

Japan's Ministry of Economy, Trade, and Industry requires PUE 1.4 by 2030 and PUE 1.3 for new builds from 2029, effectively outlawing traditional chillers in humid climates. China's energy labeling for chillers and its provincial power-quota regime likewise favor facilities that remove heat at the chip rather than at the room level. Lenovo's Neptune operates at 45 °C inlets, letting operators reuse waste heat, bypass chillers that consume up to 40% of facility power, and meet emerging carbon budgets. Singapore's Green Data Center Roadmap adds further pressure by tying new electricity allotments to demonstrated PUE improvements. Consequently, the Asia-Pacific GPU liquid cooling market benefits from a policy that makes efficiency a prerequisite for power and land access.

High Up-Front Capex and Retrofit Complexity for Brownfield Facilities

Direct-to-chip retrofits cost USD 500-USD 800 per kilowatt, more than double air-cooling upgrades, and demand phased cutovers that must preserve uptime. Operators often need structural reinforcement for pipes, electrical upgrades for pumps, and revised fire suppression, stretching payback to three to five years and deterring sites with rack densities below 50 kilowatts. Custom engineering erodes economies of scale, so many legacy owners wait until thermal ceilings force a wholesale move rather than incremental retrofits.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Growth of Edge-AI Inference Nodes in 5G Networks

- Data-Center Land Constraints in Tier-1 Cities Boost Rack-Level Density

- Limited Skilled Workforce for Liquid-Cooling O&M Across Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Single-phase solutions accounted for 74.51% of the Asia-Pacific GPU liquid cooling market share in 2025, a position built on mature water loops that integrate with standard facility infrastructure. Lenovo Neptune and HPE ProLiant XD685 operate at 45 °C inlets, achieve a PUE of near 1.1, and provide a familiar maintenance model for staff already versed in chilled-water plants. Two-phase systems, although only 25.49% in 2025, are racing ahead at 32.17% CAGR as ZutaCore and Mitsubishi Heavy Industries prove rack-level partial PUE near 1.01 and remove facility water from the white space.

Chips such as the NVIDIA GB200 and AMD MI300X are pushing past the 1,000-watt mark. At this threshold, water's thermal headroom becomes limited, and the required flow rates demand significant pump power, making traditional cooling methods less efficient. This has led to increased interest in alternative cooling solutions, particularly two-phase cooling systems. Carrier's investment in ZutaCore, coupled with Trane's acquisition of LiquidStack, underscores a pivotal shift in the industry. These strategic moves by HVAC behemoths highlight their confidence in two-phase cooling roadmaps, which offer enhanced efficiency and scalability. As a result, the Asia-Pacific GPU liquid cooling market is expected to pivot towards dielectric fluids by 2028, marking a significant transformation in cooling technologies.

In 2025, component-level cold plates accounted for 55.72% of the Asia-Pacific GPU liquid cooling market, aligning with hyperscalers' focus on optimizing individual chips. These cold plates are designed to provide per-chip cooling, which is critical for managing the high heat output of GPUs in hyperscale environments. Supermicro's DLC-2, a prominent solution in this space, boasts the ability to extract 92% of server heat. This capability allows operators to seamlessly integrate GPU and CPU nodes without requiring extensive rack modifications. On the other hand, colocation operators are increasingly adopting rack-level coolant distribution units (CDUs) to streamline heat removal processes. These units treat heat removal as a shared service, offering a centralized approach to cooling that simplifies operations and enhances efficiency.

Rack-level solutions, such as ZutaCore's 2 megawatt end-of-row CDU and CoolIT's CHx500 stack, are becoming integral to retrofits by major players like Equinix and STT GDC. These solutions enable landlords to maintain control over critical aspects such as metering, maintenance, and service level agreements (SLAs). With rack-level offerings growing at a 31.60% CAGR, the market is witnessing a significant shift in cooling strategies. Tenants are moving away from individually plumbing racks and are instead subscribing to cooling as a service. This model aligns with the market's transition toward multi-tenant AI clusters, which demand scalable and efficient cooling solutions to support their high-performance computing needs.

List of Companies Covered in this Report:

- CoolIT Systems Inc.

- Asetek A/S

- Vertiv Holdings Co.

- Schneider Electric SE

- Huawei Technologies Co., Ltd.

- Iceotope Technologies Limited

- Submer Technologies Sl.

- LiquidStack Holdings, Inc.

- ZutaCore Ltd.

- JetCool Technologies Inc.

- Boyd Corporation

- Fujitsu Limited

- Inspur Electronic Information Industry Co., Ltd.

- Mitsubishi Electric Corporation

- Sugon Information Industry Co., Ltd.

- Rittal GmbH & Co. KG

- Green Revolution Cooling Inc.

- Lenovo Group Limited

- Hewlett Packard Enterprise Company

- Alibaba Cloud (Alibaba Group Holding Limited)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mainstream AI-led Hyperscale Expansions Drive Liquid-Cooling Adoption

- 4.2.2 Mandatory Energy-Efficiency Regulations Across East and South-East Asia

- 4.2.3 Rapid Growth of Edge-AI Inference Nodes in 5G Networks

- 4.2.4 Data-Center Land Constraints in Tier-1 Cities Boost Rack-Level Density

- 4.2.5 Availability of Turn-key Liquid-Ready Colocation Capacity

- 4.2.6 Advancements in Coolant Chemistry Enabling Non-Conductive Two-Phase Designs

- 4.3 Market Restraints

- 4.3.1 High Up-Front Capex and Retrofit Complexity for Brownfield Facilities

- 4.3.2 Limited Skilled Workforce for Liquid-Cooling O&M Across Emerging Markets

- 4.3.3 Supply-Chain Bottlenecks in Precision Cold Plates and Quick Disconnects

- 4.3.4 PFAS Regulatory Uncertainty for Two-Phase Dielectric Fluids

- 4.4 Industry Value / Supply-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Cooling Type

- 5.1.1 Single-Phase Liquid Cooling

- 5.1.2 Two-Phase Liquid Cooling

- 5.2 By Cooling Level

- 5.2.1 Component-Level Cooling

- 5.2.2 Server / Rack-Level Cooling

- 5.3 By Deployment

- 5.3.1 Hyperscale / Cloud

- 5.3.2 Enterprise

- 5.3.3 Government and Research (HPC)

- 5.3.4 Edge AI

- 5.4 By GPU Power Density

- 5.4.1 Below 300W

- 5.4.2 300W - 700W

- 5.4.3 Above 700W

- 5.5 By Geography

- 5.5.1 China

- 5.5.2 Japan

- 5.5.3 South Korea

- 5.5.4 India

- 5.5.5 Southeast Asia

- 5.5.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 CoolIT Systems Inc.

- 6.4.2 Asetek A/S

- 6.4.3 Vertiv Holdings Co.

- 6.4.4 Schneider Electric SE

- 6.4.5 Huawei Technologies Co., Ltd.

- 6.4.6 Iceotope Technologies Limited

- 6.4.7 Submer Technologies Sl.

- 6.4.8 LiquidStack Holdings, Inc.

- 6.4.9 ZutaCore Ltd.

- 6.4.10 JetCool Technologies Inc.

- 6.4.11 Boyd Corporation

- 6.4.12 Fujitsu Limited

- 6.4.13 Inspur Electronic Information Industry Co., Ltd.

- 6.4.14 Mitsubishi Electric Corporation

- 6.4.15 Sugon Information Industry Co., Ltd.

- 6.4.16 Rittal GmbH & Co. KG

- 6.4.17 Green Revolution Cooling Inc.

- 6.4.18 Lenovo Group Limited

- 6.4.19 Hewlett Packard Enterprise Company

- 6.4.20 Alibaba Cloud (Alibaba Group Holding Limited)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment