PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065495

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065495

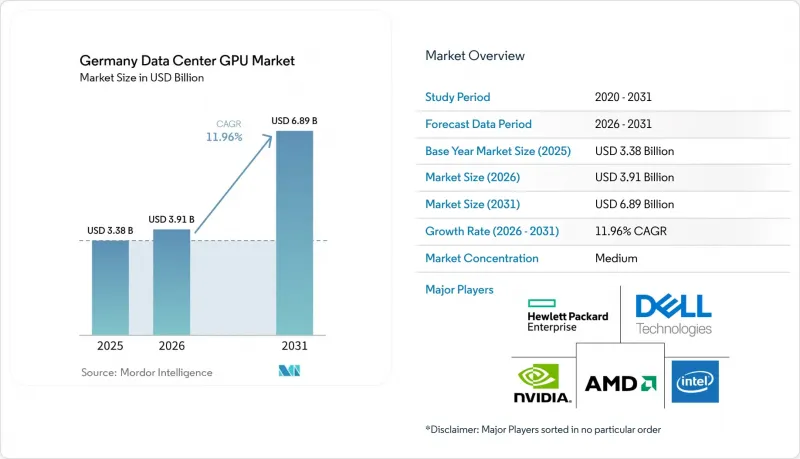

Germany Data Center GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the germany data center GPU market size is expected to increase from USD 3.38 billion in 2025 to USD 3.91 billion in 2026 and reach USD 6.89 billion by 2031, growing at a CAGR of 11.96% over 2026-2031.

This report is Segmented by Deployment Type (Cloud Data Centers, Enterprise / Private Data Centers, and More), GPU Type (Training GPUs and Inference GPUs), Interconnect (PCIe-Based GPUs and High-Bandwidth Interconnect GPUs), Workload Type (AI and ML, HPC, Data Analytics, and More), and End-User (Hyperscalers/CSPs, Enterprises, and More). The Market Forecasts are Provided in Value (USD).

Germany Data Center GPU Market Trends and Insights

Growing Adoption of AI Workloads in German Enterprises

SAP's Industrial AI Cloud signed over 100 manufacturers in 2025, shifting mid-market buyers from capital purchases toward consumption-based GPU contracts. By Q4 2025, Northern Data revealed that its H100 and H200 GPUs were secured under reserved or on-demand agreements, highlighting a shift from speculative interest to firm enterprise commitments. BMW harnessed DGX Hopper clusters to produce synthetic driving images, slashing the training time for perception models. While financial services continue to test fraud-detection models, the rollout is delayed by transparency requirements under the EU AI Act.

Expansion of Hyperscaler Cloud Regions in Frankfurt and Berlin

AWS spent EUR 8.8 billion (USD 9.9 billion) expanding Frankfurt zones, yet new entrants must now fund 100% of substation upgrades under revised grid rules. Google countered with a EUR 5.5 billion (USD 6.2 billion) Dietzenbach campus that bypasses inner-city transformer congestion. AWS's EUR 7.8 billion (USD 8.8 billion) Brandenburg sovereign cloud, targeting federal workloads, shows operators are geographically splitting latency-sensitive inference and batch training.

High Electricity Costs and Grid Constraints in Major German Data Center Hubs

In 2024, medium-voltage users in Frankfurt faced network fees. With pending grid requests in Berlin totaling 2.8 GW, operators are now tasked with financing comprehensive substation upgrades. These upgrades extend the construction timeline by 18 to 36 months.

Other drivers and restraints analyzed in the detailed report include:

- Emergence of Sovereign Cloud Initiatives Driving Local GPU Capacity

- Rising Demand for Energy-Efficient GPU Servers Amid ESG Regulations

- Supply Chain Dependence on Non-EU GPU Manufacturers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Edge facilities are forecast to record a 12.78% CAGR through 2031, underpinned by automotive OEMs that install local GPU clusters to keep perception latency below 10 ms. BMW's Munich research hub used DGX Hopper nodes to achieve an 8-fold increase in synthetic-image generation, underscoring why private edge racks are proliferating.

Cloud data centers still accounted for 58.76% of revenue in 2025, but Frankfurt's grid caps and Baukostenzuschusse now slow further construction. SAP's sovereign AI Cloud straddles private and public models, letting manufacturers retain data locality while offloading operations.

Training GPUs accounted for 55.72% of 2025 spending, as hyperscalers snapped up H100 and H200 inventory for foundation-model runs. Intel's Gaudi 3, offered in IBM Cloud's Frankfurt region, claims 50% lower inference costs than the H100, promoting Ethernet fabrics over InfiniBand.

Inference demand is rising most sharply at the edge, where slot power and form-factor efficiency matter more than peak FLOPS. AMD's MI300 roadmap doubles HBM per GPU, appealing to memory-bound inference tasks in sovereign clouds.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Cerebras Systems Inc.

- Huawei Technologies Co. Ltd.

- Giga Computing Technology Co. Ltd.

- AsusTek Computer Inc.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Lenovo Group Limited

- Deutsche Telekom AG

- T-Systems International GmbH

- Hetzner Online GmbH

- SAP SE

- Atos SE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption of AI Workloads in German Enterprises

- 4.2.2 Rising Demand for Energy-Efficient GPU Servers Amid ESG Regulations

- 4.2.3 Expansion of Hyperscaler Cloud Regions in Frankfurt and Berlin

- 4.2.4 Government Funding for HPC and Quantum Research Facilities

- 4.2.5 Increasing Edge Computing Needs for Autonomous Manufacturing

- 4.2.6 Emergence of Sovereign Cloud Initiatives Driving Local GPU Capacity

- 4.3 Market Restraints

- 4.3.1 High Electricity Costs and Grid Constraints in Major German Data Center Hubs

- 4.3.2 Supply Chain Dependence on Non-EU GPU Manufacturers

- 4.3.3 Stringent Data Protection and Residency Regulations Limiting Cross-Border Workloads

- 4.3.4 Skilled GPU Programming Talent Shortage

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 Cloud Data Centers

- 5.1.2 Enterprise / Private Data Centers

- 5.1.3 Edge Data Centers

- 5.2 By GPU Type

- 5.2.1 Training GPUs

- 5.2.2 Inference GPUs

- 5.3 By Interconnect

- 5.3.1 PCIe-Based GPUs

- 5.3.2 High-Bandwidth Interconnect GPUs

- 5.4 By Workload Type

- 5.4.1 Artificial Intelligence (AI) and Machine Learning (ML)

- 5.4.2 High-Performance Computing (HPC) (non-AI scientific computing)

- 5.4.3 Data Analytics (database acceleration, query processing)

- 5.4.4 Graphics and Visualization (VDI, rendering, digital twins)

- 5.5 By End-User

- 5.5.1 Hyperscalers / Cloud Service Providers

- 5.5.2 Enterprises

- 5.5.3 Government and Research Institutions

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Cerebras Systems Inc.

- 6.4.5 Huawei Technologies Co. Ltd.

- 6.4.6 Giga Computing Technology Co. Ltd.

- 6.4.7 AsusTek Computer Inc.

- 6.4.8 Dell Technologies Inc.

- 6.4.9 Hewlett Packard Enterprise Company

- 6.4.10 Lenovo Group Limited

- 6.4.11 Deutsche Telekom AG

- 6.4.12 T-Systems International GmbH

- 6.4.13 Hetzner Online GmbH

- 6.4.14 SAP SE

- 6.4.15 Atos SE

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment