PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065508

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065508

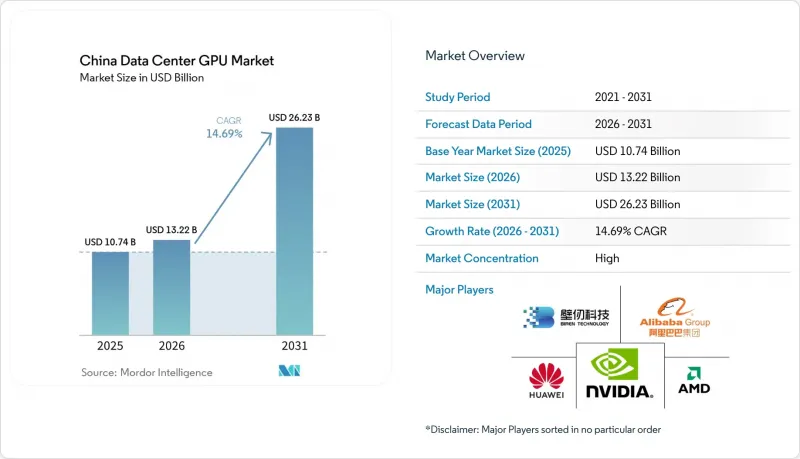

China Data Center GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the china data center GPU market size is projected to be USD 10.74 billion in 2025, USD 13.22 billion in 2026, and reach USD 26.23 billion by 2031, growing at a CAGR of 14.69% from 2026 to 2031.

This report is Segmented by Deployment Type (Cloud Data Centers, Enterprise/Private Data Centers, Edge Data Centers), GPU Type (Training GPUs, Inference GPUs), Interconnect (PCIe-Based GPUs, High-Bandwidth Interconnect GPUs), Workload Type (AI and ML, HPC, and More), and End-User (Hyperscalers/CSPs, Enterprises, Government and Research Institutions). Market Forecasts are Provided in Terms of Value (USD).

China Data Center GPU Market Trends and Insights

Rising Hyperscaler Capex for AI Clusters

ByteDance set aside CNY 160 billion (USD 23 billion) for 2026 capital expenditure and devoted half of that sum to GPU purchases, while Alibaba discussed raising infrastructure investment to RMB 480 billion over three years.Tencent doubled its annual AI budget to roughly USD 5 billion in 2026, although earlier supply tightness kept its 2025 spending to RMB 79.2 billion. Hangzhou's USD 3.7 billion procurement package illustrates municipal co-investment that compounds corporate outlays. United States export licenses allowed limited H200 imports with a 25% tariff and 50% volume cap, nudging hyperscalers toward Huawei Ascend alternatives. Activity centers on the Yangtze River Delta and the Greater Bay Area, where sub-10-millisecond latency and 300 watts per rack of power headroom accommodate multi-card clusters.

Export-Control-Driven Substitution Toward Local GPUs

The block on advanced NVIDIA and AMD accelerators since mid-2025 stimulated Huawei shipments that topped 50,000 Ascend 910B units by year-end 2025 and planned 750,000 Ascend 950PR chips for 2026. The 910C and 950PR deliver 60-80% of H100 throughput and ride SMIC's N+3 process, shrinking reliance on TSMC packaging capacity. Cambricon's 2024 revenue surged 67.4% to RMB 1.28 billion, and investment banks see domestic self-sufficiency reaching 50% by 2027. Mandates favoring indigenous tech speed adoption in public-sector and military workloads. Even private hyperscalers add domestic cards to hedge license risk.

Advanced Packaging (CoWoS/HBM) Capacity Bottlenecks

TSMC quadrupled CoWoS output to about 120,000 wafers per month by early 2026, yet NVIDIA locks down close to 60% of that allocation. HBM3e remains tight with a 30% global shortfall even after SK Hynix and Samsung expansions. Domestic vendors tap 7-nanometer nodes with LPDDR memory to avoid the queue, but high-end training chips still need CoWoS, delaying deliveries by more than 50 weeks. The bottleneck forces Chinese buyers to stretch training schedules or pay premiums for scarce imports, clipping near-term upside for the China data center GPU market.

Other drivers and restraints analyzed in the detailed report include:

- Government Vouchers Incentivizing Domestic AI Compute

- Liquid-Cooling Adoption Enabling 80 kW+ Racks

- Rapid Price Declines in GPU Cloud Leasing

- Persistent Software Ecosystem Gap vs CUDA

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Edge facilities represented the fastest-growing slice of the China data center GPU market during 2025 and are forecast to post a 20.3% CAGR through 2031. Cloud data centers still dominate with 62.84% of China's data center GPU market share in 2025, thanks to hyperscalers that run 100,000-GPU clusters to achieve economies of scale.

China Mobile and China Unicom staged 5G MEC pilots that use GPUs for cloud gaming and real-time video, proving that sub-15-millisecond round-trip is achievable when compute sits within the city core. Lower leasing prices weaken the business case for small private halls, so many mid-sized firms burst workloads into public cloud but keep sensitive data on on-premise edge nodes. Liquid-cooled micro-modules shipping from ZTE help solve space and power limitations in retail and factory environments.

Inference accelerators held 59.21% of the China data center GPU market size in 2025 and are projected to grow at a 16.8% CAGR, making them both the largest and fastest segment. Training GPUs, while indispensable for new foundation models, expand more slowly as major clusters already exist and inference drives near-term revenue.

Alibaba Cloud's TensorRT-LLM and vLLM services can answer billions of daily calls on mid-tier GPUs paired with LPDDR memory, cutting chip costs by 30-40% against HBM-based alternatives. Huawei's 950PR sold to ByteDance focuses on inference throughput with 1.56 PFLOPS FP4 rather than peak FP16 performance. Domestic designers choose 6- or 7-nanometer nodes to dodge CoWoS queues, aligning with price-sensitive inference deployments.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Huawei Technologies Co., Ltd.

- Alibaba Group Holding Limited (Alibaba Cloud)

- Baidu, Inc.

- Tencent Holdings Ltd.

- Inspur Electronic Information Industry Co., Ltd.

- Lenovo Group Limited

- Intel Corporation

- Biren Technology Co., Ltd.

- Moore Threads Technology Co., Ltd.

- Cambricon Technologies Corp. Ltd.

- Hygon Information Technology Co., Ltd.

- Dawning Information Industry Co., Ltd. (Sugon)

- Enflame Technology Co., Ltd.

- MetaX Technology Inc.

- Iluvatar CoreX (Shanghai) Inc.

- JINGJIA Microelectronics Co., Ltd.

- China Telecom Corporation Limited

- ByteDance Ltd. (Volcengine)

- Shanghai Zhaoxin Semiconductor Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Hyperscaler Capex for AI Clusters

- 4.2.2 Government Vouchers Incentivizing Domestic AI Compute

- 4.2.3 Export-Control-Driven Substitution Toward Local GPUs

- 4.2.4 Rapid Price Declines in GPU Cloud Leasing

- 4.2.5 Liquid-Cooling Adoption Enabling 80 kW+ Racks

- 4.2.6 East-Data West-Compute Policy Unlocking Low-Cost Power

- 4.3 Market Restraints

- 4.3.1 Advanced Packaging (CoWoS/HBM) Capacity Bottlenecks

- 4.3.2 Persistent Software Ecosystem Gap vs CUDA

- 4.3.3 Low Utilization Rates in Newly Built AI Centers

- 4.3.4 Grid-Connection Delays in Remote Western Hubs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 Cloud Data Centers

- 5.1.2 Enterprise / Private Data Centers

- 5.1.3 Edge Data Centers

- 5.2 By GPU Type

- 5.2.1 Training GPUs

- 5.2.2 Inference GPUs

- 5.3 By Interconnect

- 5.3.1 PCIe-Based GPUs

- 5.3.2 High-Bandwidth Interconnect GPUs

- 5.4 By Workload Type

- 5.4.1 Artificial Intelligence (AI) and Machine Learning (ML)

- 5.4.2 High-Performance Computing (HPC) (non-AI scientific computing)

- 5.4.3 Data Analytics (database acceleration, query processing)

- 5.4.4 Graphics and Visualization (VDI, rendering, digital twins)

- 5.5 By End-User

- 5.5.1 Hyperscalers / Cloud Service Providers

- 5.5.2 Enterprises

- 5.5.3 Government and Research Institutions

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Huawei Technologies Co., Ltd.

- 6.4.4 Alibaba Group Holding Limited (Alibaba Cloud)

- 6.4.5 Baidu, Inc.

- 6.4.6 Tencent Holdings Ltd.

- 6.4.7 Inspur Electronic Information Industry Co., Ltd.

- 6.4.8 Lenovo Group Limited

- 6.4.9 Intel Corporation

- 6.4.10 Biren Technology Co., Ltd.

- 6.4.11 Moore Threads Technology Co., Ltd.

- 6.4.12 Cambricon Technologies Corp. Ltd.

- 6.4.13 Hygon Information Technology Co., Ltd.

- 6.4.14 Dawning Information Industry Co., Ltd. (Sugon)

- 6.4.15 Enflame Technology Co., Ltd.

- 6.4.16 MetaX Technology Inc.

- 6.4.17 Iluvatar CoreX (Shanghai) Inc.

- 6.4.18 JINGJIA Microelectronics Co., Ltd.

- 6.4.19 China Telecom Corporation Limited

- 6.4.20 ByteDance Ltd. (Volcengine)

- 6.4.21 Shanghai Zhaoxin Semiconductor Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment