PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065506

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065506

Ajinomoto Build-Up Film (ABF) Substrate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

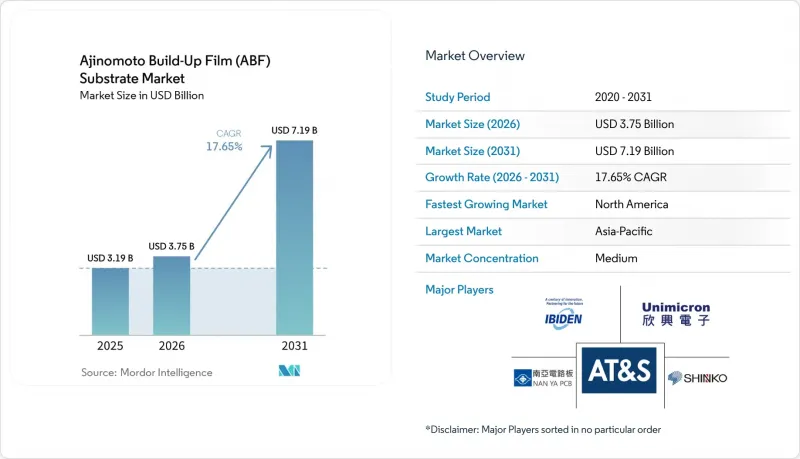

According to Mordor Intelligence, the ajinomoto build-Up film substrate market size is projected to expand from USD 3.19 billion in 2025 and USD 3.75 billion in 2026 to USD 7.19 billion by 2031, registering a 17.65% CAGR between 2026 and 2031.

This report is Segmented by Package Type (Flip-Chip BGA, and Flip-Chip CSP), Application (AI GPUs, Cpus, AI Accelerators, and Networking ICs), End-User Industry (Data Centers, Consumer Electronics, Automotive, and Telecom), and Geography (North America, Europe, Asia-Pacific, and Rest of the World). Market Forecasts are Provided in Terms of Value (USD).

Global Ajinomoto Build-Up Film (ABF) Substrate Market Trends and Insights

Rising Adoption Of ABF Substrates In AI GPU Packages

Next-generation AI GPUs such as NVIDIA H200 and AMD MI300 require 12-to-20 build-up layers, sub-15 µm lines and spaces, and coefficient of thermal expansion (CTE) matching within 2 ppm / °C to mitigate warpage, pushing Ajinomoto Build-Up Film substrate market demand to record highs. Ibiden earmarked JPY 500 billion (USD 3.3 billion) for two Japanese fabs that will begin sequential ramp in fiscal 2027, explicitly aimed at these GPUs. Multi-chiplet layouts double the substrate area per package, and Ajinomoto, which controls over 95% of the ABF dielectric film supply, has announced a 50% capacity increase by 2030 to keep pace. With qualification lead times longer than a year, supply stays tight through at least 2027, granting early movers pricing power.

Shift Toward Chiplet Architectures Requiring Large-Area Substrates

Disaggregated compute tiles in AMD Bergamo or Intel Meteor Lake significantly increase substrate real estate by 40-60%, creating a need for routing densities of 2,000 nets/mm2 and up to 24 layers. This increase in design complexity has driven manufacturers like Nan Ya Printed Circuit Board to develop 24-plus-layer substrates that aim to achieve sub-15 µm geometries by 2026. However, as multiple high-value dice are integrated onto a single laminate, the economic risk associated with a single killer defect rises substantially. To mitigate this risk, suppliers are adopting advanced technologies such as feed-forward adaptive lithography and high-speed optical inspection systems. These measures are designed to detect and address issues like particles or residue early in the production process, specifically before the lamination stage, ensuring higher yields and improved reliability.

High Capital Intensity And Long Equipment Lead Times

Greenfield fabs require investments ranging from USD 800 million to USD 1.2 billion and face a 12-18 month wait to procure essential equipment, such as laser drillers or vacuum laminators. These high costs and extended timelines effectively exclude smaller entrants from competing in the market. A case in point is Amkor's Arizona plant, where construction commenced in late 2025. Despite receiving USD 407 million in CHIPS funding, the facility only began generating revenue in the first half of 2028, highlighting the lengthy lead times associated with such projects. Additionally, tool vendors, which operate as oligopolies, tend to prioritize their established customers. This practice creates high cost and supply chain challenges for new market entrants, further solidifying the barriers to entry in this space.

Other drivers and restraints analyzed in the detailed report include:

- Capacity Expansion Of Leading Substrate Makers In Taiwan And Japan

- Advanced Lithography Integration For Sub-10 µm Lines And Spaces

- Process Yield Challenges Above 10 Build-Up Layers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Ajinomoto Build-Up Film market size for FC-BGA accounted for 88% in 2025 and is expected to grow at a 18.05% CAGR alongside the overall segment. FC-BGA enables direct solder bump interconnects that minimize inductance and support >10,000 signals, indispensable for AI accelerators and server CPUs. Ibiden's Kawama and Ohno plants are fully dedicated to FC-BGA lines aimed at AI servers. Automotive-qualified versions passed AEC-Q100 in 2025, positioning Samsung Electro-Mechanics to capture rising zonal ECU demand.

FC-CSP held the remaining share, primarily catering to mobiles and wearables, where physical height constraints take precedence over raw bandwidth capabilities. The growth in FC-CSP volume is limited as semiconductor capital investments increasingly shift focus toward data centers, which demand higher performance and bandwidth. However, FC-CSP continues to play a significant role in supporting edge AI SOCs with TDPs under 20 W. Suppliers in this segment capitalize on well-established, mature 15-20 µm design rules, enabling them to maintain a competitive edge in cost efficiency while addressing the specific needs of these applications.

Geography Analysis

Asia-Pacific is expected to dominate the market, accounting for 58% of the 2025 value. Taiwan's Unimicron, Nan Ya PCB, and Kinsus are strategically clustered around TSMC CoWoS lines, driving regional growth. Despite Kinsus' USD 744 million expansion efforts, the near-term supply gap persists, leaving the region vulnerable to disruptions. Any geopolitical tensions or natural disasters, such as earthquakes, could potentially erase 6-12 months of supply. Japan is also a key player in the region, with Ibiden and Shinko investing a combined JPY 560 billion (USD 3.75 billion) to maintain high-layer technology expertise locally. Meanwhile, South Korea's Samsung Electro-Mechanics and LG Innotek are channeling investments into Vietnam to leverage lower labor costs, although they continue to act as technology gatekeepers.

North America, although starting from a smaller base, is projected to experience the fastest growth with a compound annual growth rate (CAGR) of 18.65%. The CHIPS Act has provided significant grants, including USD 407 million to Amkor and USD 75 million to Absolics, signaling strong governmental support for the sector. However, the long payback period for greenfield projects remains a challenge. Companies like TTM Technologies are poised to benefit once domestic substrate lines achieve qualification. Additionally, hyperscalers are increasingly incorporating North American suppliers into their dual-sourcing strategies, further boosting the region's potential for growth.

Europe maintains a niche position in the market, led by AT&S's EUR 500 million (USD 540 million) competence center in Austria. The region benefits from the demand for high-quality standards such as ISO 26262 and IATF 16949, particularly from automotive OEMs and industrial automation players. These stringent requirements help shield local suppliers from competition with low-cost Asian manufacturers. Elsewhere, Vietnam is emerging as a significant assembly hub, driven by investments from companies like Samsung and Meiko. In contrast, South America and the Middle East currently hold negligible positions in the market, with limited activity in these regions.

- Ibiden Co., Ltd.

- Unimicron Technology Corp.

- Nan Ya Printed Circuit Board Corporation

- Shinko Electric Industries Co., Ltd.

- Kinsus Interconnect Technology Corp.

- AT&S Austria Technologie & Systemtechnik AG

- Kyocera Corporation

- LG Innotek Co., Ltd.

- Samsung Electro-Mechanics Co., Ltd.

- TTM Technologies, Inc.

- Shennan Circuits Co., Ltd.

- Zhen Ding Technology Holding Limited

- DSBJ Co., Ltd.

- Isu Petasys Co., Ltd.

- NCAB Group AB

- Meiko Electronics Co., Ltd.

- Wus Printed Circuit Company Limited

- Yokowo Co., Ltd.

- Daeduck Electronics Co., Ltd.

- Ebina Denka Kogyo Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of ABF Substrates in AI GPU Packages

- 4.2.2 Shift Toward Chiplet Architectures Requiring Large-Area Substrates

- 4.2.3 Capacity Expansion of Leading Substrate Makers in Taiwan and Japan

- 4.2.4 Advanced Lithography Integration for Sub-10 µm Lines and Spaces

- 4.2.5 Strategic Long-Term Supply Agreements With Hyperscalers

- 4.2.6 Localization Incentives Under CHIPS and Similar Acts

- 4.3 Market Restraints

- 4.3.1 High Capital Intensity and Long Equipment Lead Times

- 4.3.2 Process Yield Challenges Above 10 Build-Up Layers

- 4.3.3 Short-Term Oversupply Risk From Aggressive Capacity Adds

- 4.3.4 Emergence of Alternative Glass and RDL-First Substrate Technologies

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Package Type

- 5.1.1 Flip-chip BGA

- 5.1.2 Flip-chip CSP

- 5.2 By Application

- 5.2.1 AI GPUs

- 5.2.2 CPUs (Server and Desktop)

- 5.2.3 AI Accelerators (TPUs, NPUs, Custom ASICs)

- 5.2.4 Networking / Data Center ICs

- 5.3 By End-user Industry

- 5.3.1 Data Centers / Cloud

- 5.3.2 Consumer Electronics

- 5.3.3 Automotive (ADAS, Autonomous Compute)

- 5.3.4 Telecom and Networking

- 5.4 By Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia-Pacific

- 5.4.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Ibiden Co., Ltd.

- 6.4.2 Unimicron Technology Corp.

- 6.4.3 Nan Ya Printed Circuit Board Corporation

- 6.4.4 Shinko Electric Industries Co., Ltd.

- 6.4.5 Kinsus Interconnect Technology Corp.

- 6.4.6 AT&S Austria Technologie & Systemtechnik AG

- 6.4.7 Kyocera Corporation

- 6.4.8 LG Innotek Co., Ltd.

- 6.4.9 Samsung Electro-Mechanics Co., Ltd.

- 6.4.10 TTM Technologies, Inc.

- 6.4.11 Shennan Circuits Co., Ltd.

- 6.4.12 Zhen Ding Technology Holding Limited

- 6.4.13 DSBJ Co., Ltd.

- 6.4.14 Isu Petasys Co., Ltd.

- 6.4.15 NCAB Group AB

- 6.4.16 Meiko Electronics Co., Ltd.

- 6.4.17 Wus Printed Circuit Company Limited

- 6.4.18 Yokowo Co., Ltd.

- 6.4.19 Daeduck Electronics Co., Ltd.

- 6.4.20 Ebina Denka Kogyo Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment