PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065568

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065568

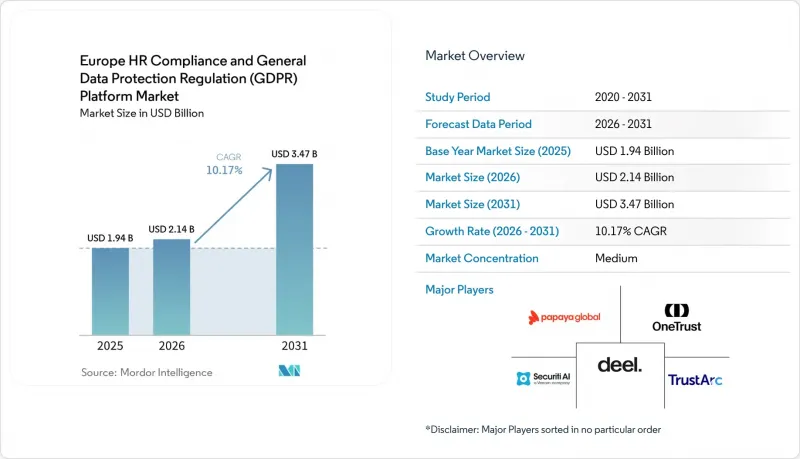

Europe HR Compliance And General Data Protection Regulation (GDPR) Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the europe hR compliance and General Data Protection Regulation (GDPR) platform market size was valued at USD 1.94 billion in 2025 and is projected to reach USD 3.47 billion by 2031, expanding at a CAGR of 10.17% from 2026 to 2031.

This report is Segmented by Functionality (Policy and Procedure Management, and More), Deployment Mode (On-Premises, and More), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (Banking, Financial Services and Insurance, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe HR Compliance And General Data Protection Regulation (GDPR) Platform Market Trends and Insights

Stringent GDPR Enforcement and Rising Non-Compliance Penalties

National data protection authorities across Europe imposed EUR 1.14 billion (USD 1.28 billion) in GDPR fines in 2025, keeping enforcement risk at a level few employers could ignore. The same annual report recorded 414 new cross-border cases and 1,299 One-Stop-Shop procedures in 2025, indicating that enforcement activity is broad and costly. This environment pushed the Europe HR compliance and General Data Protection Regulation (GDPR) platform market toward tools that can document controls, decisions, and audit trails at the workflow level rather than only in policy files. Vendors also had stronger reasons to tighten security design, contractual safeguards, and evidence management, as customers increasingly evaluated products through the lens of regulatory scrutiny. The result was a buying pattern that favored platforms able to show continuous governance, cleaner records of processing, and easier proof of technical and organizational measures. That shift supported adoption even in organizations that had already completed an earlier round of privacy tooling and now needed something more integrated.

Multi-Country Labor-Law and Payroll Localization Complexity

Managing compliance across 27 EU member states remained a major reason employers invested in broader platforms instead of single-country tools. This pressure went beyond GDPR because labor laws, payroll rules, collective agreements, and employee data expectations varied widely across jurisdictions and changed at different paces. The Europe HR compliance and General Data Protection Regulation (GDPR) platform market, therefore, rewarded vendors that could maintain country-level legislative content and deliver updates without long customer-side deployment cycles. SD Worx reinforced this direction in April 2026 when it launched Legal Watch, an AI-based monitoring platform initially covering Germany, Luxembourg, Spain, Sweden, and the Netherlands. Buyers increasingly treated regulatory depth as a primary product feature because weak localization creates exposure across payroll, leave management, compensation reporting, and worker documentation. That dynamic helped multi-country platforms defend higher pricing and stronger retention than narrower alternatives.

High Integration Costs Across Legacy HRIS, Payroll, and ERP Stacks

Integration remained the clearest near-term brake on adoption because many employers still ran mixed estates of HRIS, payroll, ERP, and time systems from different generations. That problem was especially evident in multi-country rollouts, where compliance data had to be consistently moved across legacy payroll engines, local attendance tools, and central reporting layers. The Europe HR compliance and General Data Protection Regulation (GDPR) platform market, therefore, favored vendors with stronger native connectors, pre-built country packs, and simpler implementation paths. Buyers were also more cautious after the May 2025 ruling by the German Federal Labor Court, which awarded an employee EUR 200 (USD 224.6) in non-material damages for a cloud-based HR system that transferred personal data beyond the scope of an applicable works agreement. The case reinforced that integration is not only a technical issue because weak governance around transfers can create direct legal risk during deployment. That kept purchasing interest strong, but it also slowed the pace at which projects could move from contract signing to full operation.

Other drivers and restraints analyzed in the detailed report include:

- Cloud Migration and Digitization of HR and Privacy Workflows

- Rising Data Subject Access Request and Consent-Management Volumes

- Shortage of Privacy, Payroll, and Compliance Specialists

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

HR Compliance and Regulatory Management held 37.05% of the Europe HR compliance and General Data Protection Regulation (GDPR) market share in 2025, making it the largest functional category. That position reflected the fact that labor-law tracking, employee recordkeeping, and GDPR accountability are baseline requirements for nearly every employer in the region. The Europe HR compliance and General Data Protection Regulation (GDPR) platform market continued to direct first-time platform budgets toward this category, as one license can support multiple statutory obligations simultaneously. That breadth gave the segment an advantage over narrower tools that solve only one issue in isolation.

Time and Attendance Compliance is projected to grow at a 11.38% CAGR from 2026 to 2031, making it the fastest-growing functionality during this period. Growth came from working-time documentation needs, more detailed leave governance, and rising pressure to keep auditable records across countries with different rules. Vendors increasingly added locally compliant leave configuration and gender pay gap analytics templates, demonstrating how attendance, compensation, and reporting requirements are starting to overlap within the same workflow. GDPR Data Privacy Management, Policy, and Procedure Management also continued to attract replacement demand as employers consolidated single-point tools into broader suites. Pay Transparency and Compensation Compliance remained smaller in current revenue terms, but the June 2027 reporting cycle for employers with 150 or more employees kept near-term buying interest firm.

Cloud deployment accounted for 68.11% of the Europe HR compliance and General Data Protection Regulation (GDPR) market size in 2025, which kept it as the leading delivery model. This reflected the clear operating advantage of subscription SaaS platforms, where vendors can push regulatory content updates without waiting for customer-side IT release cycles. The Europe HR compliance and General Data Protection Regulation (GDPR) platform market also benefited from a better sovereign-cloud foundation, which reduced a long-standing obstacle around data residency. Workday EU Sovereign Cloud and the AWS European Sovereign Cloud both helped shift the discussion from whether cloud could meet compliance expectations to how cloud should be structured for regulated HR workloads.

Hybrid deployment is forecast to grow at an 11.71% CAGR from 2026 to 2031, which made it the fastest-growing mode. This pattern fit employers in financial services and healthcare that wanted cloud flexibility for newer compliance modules while retaining tighter control over their most sensitive data layers. Hybrid is also suited to organizations subject to country-level scrutiny of employee data transfers, especially where local review bodies expect more detailed governance of processing arrangements. On-premises demand continued to decline as a standalone preference, even though it remained relevant in the most tightly controlled environments. Security certifications such as ISO 27001 and SOC 2 Type II also became stronger procurement filters, narrowing the field to vendors that could evidence infrastructure controls and application features.

List of Companies Covered in this Report:

- OneTrust, LLC

- Personio SE & Co. KG

- SD Worx People Solutions NV

- Deel Inc.

- Hi Bob Limited

- BambooHR LLC

- Papaya Global Ltd.

- TrustArc Inc.

- Securiti, Inc.

- BigID, Inc.

- Remote Technology, Inc.

- Employment Hero Pty Ltd

- DataGrail, Inc.

- Transcend, Inc.

- Ketch Kloud, Inc.

- IRIS Software Group Limited

- Osano, Inc.

- Didomi SAS

- Syrenis Limited

- consentmanager AB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent GDPR Enforcement and Rising Non-Compliance Penalties

- 4.2.2 Multi-Country Labor-Law and Payroll Localization Complexity

- 4.2.3 Cloud Migration and Digitization of HR and Privacy Workflows

- 4.2.4 Rising Data Subject Access Request and Consent-Management Volumes

- 4.2.5 EU Pay Transparency Directive Expanding Audit-Ready HR Data Requirements

- 4.2.6 EU AI Act Obligations for Recruitment and Worker-Management Systems

- 4.3 Market Restraints

- 4.3.1 High Integration Costs Across Legacy HRIS, Payroll, and ERP Stacks

- 4.3.2 Shortage of Privacy, Payroll, and Compliance Specialists

- 4.3.3 NIS2 and DORA Vendor-Assurance Burdens Raising Proof-and-Control Costs

- 4.3.4 German Works Council and Employee-Data Transfer Scrutiny Slowing Rollouts

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Functionality

- 5.1.1 HR Compliance and Regulatory Management

- 5.1.2 Time and Attendance Compliance

- 5.1.3 Policy and Procedure Management

- 5.1.4 GDPR Data Privacy Management

- 5.1.5 Pay Transparency and Compensation Compliance

- 5.1.6 Other Functionalities

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By End-User Industry

- 5.4.1 Banking, Financial Services and Insurance

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Information Technology and Telecommunications

- 5.4.4 Manufacturing

- 5.4.5 Retail and E-commerce

- 5.4.6 Government and Public Sector

- 5.4.7 Other End-User Industries

- 5.5 By Geography

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Russia

- 5.5.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 OneTrust, LLC

- 6.4.2 Personio SE & Co. KG

- 6.4.3 SD Worx People Solutions NV

- 6.4.4 Deel Inc.

- 6.4.5 Hi Bob Limited

- 6.4.6 BambooHR LLC

- 6.4.7 Papaya Global Ltd.

- 6.4.8 TrustArc Inc.

- 6.4.9 Securiti, Inc.

- 6.4.10 BigID, Inc.

- 6.4.11 Remote Technology, Inc.

- 6.4.12 Employment Hero Pty Ltd

- 6.4.13 DataGrail, Inc.

- 6.4.14 Transcend, Inc.

- 6.4.15 Ketch Kloud, Inc.

- 6.4.16 IRIS Software Group Limited

- 6.4.17 Osano, Inc.

- 6.4.18 Didomi SAS

- 6.4.19 Syrenis Limited

- 6.4.20 consentmanager AB

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment