PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066598

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066598

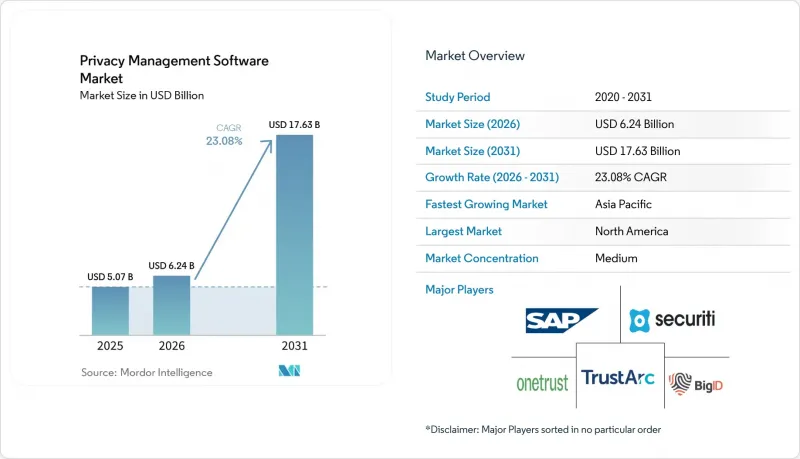

Privacy Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the privacy management software market size is expected to grow from USD 5.07 billion in 2025 to USD 6.24 billion in 2026 and is forecast to reach USD 17.63 billion by 2031 at 23.08% CAGR over 2026-2031.

This report is Segmented by Component (Solutions, Services), Deployment Type (On-Premises, and More), Organization Size (Small and Medium Enterprises, and More), Size Functionality (Consent and Preference Management and More), End-User Vertical Industry (BFSI, Healthcare and Life Sciences and More) and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD) for all the Segments.

Global Privacy Management Software Market Trends and Insights

Escalating Global Privacy Regulations Drive Market Acceleration

The widening net of data-protection statutes is reshaping governance roadmaps. India's Digital Personal Data Protection Act 2023, which tightens rules on model storage and cross-border data transfers, obliges companies to deploy platforms that can choreograph multiple regulatory workflows simultaneously. Brazil and several African nations are following suit, causing multinationals to favor solutions that update once and syndicate rule changes to every business unit. Regulators are also moving beyond personal-data rights into algorithmic transparency, reinforcing the need for unified software that can monitor AI pipeline activities in lockstep with classic privacy tasks.

Cloud and SaaS Delivery Models Transform Market Dynamics

Cloud-native rollouts answer the demand for rapid rule updates, cross-border performance, and elastic scaling. With 67% share in 2024, cloud deployment became the baseline rather than an alternative. Shared-compliance infrastructure lowers entry costs and delivers instant access to new controls when laws change. Nevertheless, cloud reliance forces firms to weigh sovereignty constraints; hybrid topologies are therefore rising where data-localization laws require in-country processing yet the enterprise still wants the efficiency of centralized orchestration.

Complex Multi-Jurisdiction Compliance Creates Implementation Barriers

Divergent rules on cross-border transfers and storage force enterprises to bolt together localized and global instances, inflating project timelines and costs. In markets such as Indonesia, strict localization mandates clash with the appeal of centralized SaaS, pushing firms toward hybrid deployments that are harder to maintain. The burden is heavier for mid-market companies that lack in-house legal and engineering talent.

Other drivers and restraints analyzed in the detailed report include:

- SMB Market Expansion in Emerging Digital Economies

- AI Governance Integration Reshapes Privacy Management Architecture

- Budget Constraints in SMB Segment Limit Market Penetration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Privacy management software market size for solutions commanded 71.20% of revenue in 2025, underscoring the indispensable role of centralized orchestration suites. Growth now pivots toward configuration and optimization expertise, evidenced by professional and managed services expanding 24.3% annually as enterprises fine-tune rule engines and integrate adjacent governance modules. The services curve steepens in regions introducing first-time privacy laws, where local firms rely on external specialists to navigate unfamiliar frameworks.

The up-market shift in service demand reflects a maturing customer base that has moved from basic deployment to continuous-improvement cycles. Managed-service packages are winning contracts by bundling regulatory monitoring, policy updates, and runtime analytics, easing internal head-count constraints. Providers that combine deep legal knowledge with automation toolkits are securing multi-year retainer agreements, strengthening switching barriers

Cloud implementations represented 66.30% of the privacy management software market in 2025 and are expanding at a 26.1% CAGR as firms chase instant upgrades and elastic compute. Private-cloud configurations appeal to highly regulated verticals that need isolation yet still want orchestration benefits. On-premise estates persist in pockets where data cannot exit national borders, but the pattern is shifting toward hybrid overlays that sync local vaults with global policy engines.

Innovation is clustering around micro-services and API extensions that let privacy controls embed directly into DevSecOps pipelines. Vendors promoting infrastructure-agnostic clusters-deploy-once, run-anywhere-lower exit barriers and help customers comply with evolving localization clauses without rewriting code, accelerating time-to-value.

Geography Analysis

North America captured 37.60% of global revenue in 2025, propelled by California's evolving privacy statutes, sector-specific rules, and escalating federal discourse on a national privacy bill. Large enterprises in technology, retail, and healthcare continue to recalibrate data-monetization models by using privacy credentials to differentiate products, reinforcing vendor demand for integrated orchestration suites. State-level advances in algorithmic accountability are steering investment toward platforms that can govern AI training data and inference outputs side by side with conventional record repositories.

Europe held 28.80% share in 2025 on the back of GDPR's continued influence and the bloc's strict approach to cross-border transfer adequacy. Corporate buyers prioritize privacy-by-design capabilities and favor suppliers that pass rigorous data-protection-impact-assessment benchmarks. Divergence between EU rules and post-Brexit UK provisions adds complexity, stimulating interest in multi-regime policy engines that maintain end-to-end audit trails without duplicating infrastructure. Fines issued under GDPR have sharpened board-level focus, translating into sustained budget protection for compliance modernisation projects.

Asia-Pacific is expanding at a 27.2% CAGR, underpinned by India's DPDP Act, Indonesia's localization mandates, and broad digitization across Southeast Asian consumer markets. Governments are layering AI ethics guidelines onto existing privacy norms, accelerating spending on platforms that can adapt rule sets dynamically. Hybrid deployment strategies satisfy sovereignty clauses while giving companies the flexibility of scale-out SaaS. Rising e-commerce penetration and multinational hyperscale cloud investments are further amplifying demand, positioning the region to narrow the revenue gap with North America over the next five years.

- OneTrust LLC

- TrustArc Inc.

- Securiti Inc.

- SAI360 (Pty Ltd)

- SAP SE

- Syrenis Ltd

- Crownpeak Technology Inc.

- Exterro Inc.

- WireWheel Inc.

- BigID Inc.

- Smart Global Governance

- Privacy Company

- Nymity (by TrustArc)

- Collibra NV

- IBM Corporation

- Microsoft Corporation

- Cisco Systems Inc.

- Informatica LLC

- DataGuard GmbH

- 2B Advice GmbH

- Privacera Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Core Privacy Requirements and Functions of a Privacy Management Offering

- 4.3 Market Drivers

- 4.3.1 Escalating global privacy regulations (GDPR, CCPA, LGPD, DPDP Act 2023)

- 4.3.2 Need to avoid heavy non-compliance penalties

- 4.3.3 Shift to cloud and SaaS delivery models

- 4.3.4 Rapid SaaS adoption by SMBs in emerging digital economies

- 4.3.5 Country-level data-localization mandates (India, Indonesia, Nigeria)

- 4.3.6 Integration of privacy tooling with Gen-AI governance frameworks

- 4.4 Market Restraints

- 4.4.1 Complex multi-jurisdiction compliance requirements

- 4.4.2 Budget constraints for SMB segment during tech-spend pullbacks

- 4.4.3 Platform fatigue due to overlap with broader GRC suites

- 4.4.4 Shortage of experienced privacy engineers and DPO talent

- 4.5 Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Intensity of Competitive Rivalry

- 4.8.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud / SaaS

- 5.2.2 On-Premise

- 5.3 By Organization Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By Functionality

- 5.4.1 Consent and Preference Management

- 5.4.2 Data Discovery and Mapping

- 5.4.3 DSAR / Rights-Request Automation

- 5.4.4 PIA / DPIA and Risk Assessment

- 5.4.5 Incident Response Workflow

- 5.5 By End-User Vertical Industry

- 5.5.1 BFSI

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 IT and Telecom

- 5.5.4 Retail and e-Commerce

- 5.5.5 Government and Public Sector

- 5.5.6 Other End-User Vertical Industries (Media, Education, etc.)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 GCC

- 5.6.5.2 South Africa

- 5.6.5.3 Rest of Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 OneTrust LLC

- 6.4.2 TrustArc Inc.

- 6.4.3 Securiti Inc.

- 6.4.4 SAI360 (Pty Ltd)

- 6.4.5 SAP SE

- 6.4.6 Syrenis Ltd

- 6.4.7 Crownpeak Technology Inc.

- 6.4.8 Exterro Inc.

- 6.4.9 WireWheel Inc.

- 6.4.10 BigID Inc.

- 6.4.11 Smart Global Governance

- 6.4.12 Privacy Company

- 6.4.13 Nymity (by TrustArc)

- 6.4.14 Collibra NV

- 6.4.15 IBM Corporation

- 6.4.16 Microsoft Corporation

- 6.4.17 Cisco Systems Inc.

- 6.4.18 Informatica LLC

- 6.4.19 DataGuard GmbH

- 6.4.20 2B Advice GmbH

- 6.4.21 Privacera Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment