PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065573

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065573

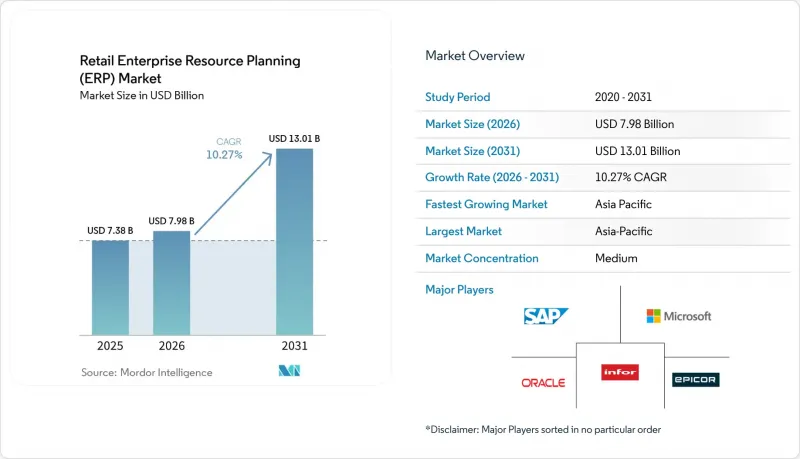

Retail Enterprise Resource Planning (ERP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the retail enterprise resource planning market size is projected to expand from USD 7.38 billion in 2025 and USD 7.98 billion in 2026 to USD 13.01 billion by 2031, registering a CAGR of 10.27% between 2026 to 2031.

This report is Segmented by Deployment Type (Cloud-Based, On-Premise, and Hybrid), Organization Size (SMEs and Large Enterprises), Component (Finance and Accounting, Inventory and Warehouse Management, Sales and CRM, HR Management, and More), Retail Format (Supermarkets and Hypermarkets, Specialty Stores, Department Stores, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Retail Enterprise Resource Planning (ERP) Market Trends and Insights

Accelerating Shift to Cloud-Based ERP In Retail

Cloud subscriptions represented most new installs in 2025 because retailers want automatic upgrades, elastic compute, and lower infrastructure costs. Hybrid strategies are catching on as chains keep sensitive customer data on local servers to meet data-residency laws, while stream analytics workloads run in public clouds for scale. Mid-sized specialty retailers gain the most because per-store pricing now replaces six-figure perpetual licenses, slashing up-front costs and shrinking implementation windows to under 18 months. The transition also unlocks embedded AI features, such as dynamic pricing, that depend on scalable compute unavailable in legacy data centers.

Growing Omnichannel Retail Complexity

Click-and-collect, ship-from-store, and endless aisle services drive demand for real-time order-management engines. Split-shipment costs drop and fulfillment decisions are optimized when inventory, pricing, and loyalty data live in a single ledger that spans stores, websites, and social-commerce feeds. Modern ERP suites eliminate overnight batch transfers, so a markdown decision propagates in minutes across all locations where the product appears. Social-commerce integrations raise the bar further, compelling retailers to surface products, process payments, and resolve service tickets on external platforms that their legacy systems never contemplated.

High Implementation Costs and Budget Overruns

Nearly three-quarters of recent projects ran over budget, with overruns due to scope creep, messy data migrations, and underestimated change management inflate service hours. Mid-market retailers feel the crunch most because they lack deep IT benches and discover too late that canned templates still need customization. Hidden costs such as third-party integration licenses, dual-running old and new systems, and per-user SaaS fees that spike during peak seasons can drive total ownership above a decade of perpetual-license spend.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Real-Time Inventory Visibility

- Government Mandates for E-Invoicing and Digital Tax Compliance

- Data Security and Privacy Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid deployments are gaining ground in the retail enterprise resource planning market as chains mix on-premises data stores with cloud analytics to comply with local regulations while still tapping elastic compute. The retail enterprise resource planning market size for hybrid solutions is advancing alongside edge servers that keep point-of-sale running during network outages, then synchronize later for central reporting. Multinationals operating in China or the European Union prefer this setup because customer data never leaves national borders, while aggregate insights roll into a global dashboard. Edge modules running on compact servers extend uptime in rural stores where broadband is shaky, ensuring every sale posts even during outages.

Hybrid adoption also supports phased migration paths. Retailers move finance and HR to SaaS first, test integrations, then tackle inventory and order workflows once data cleanliness improves. Azure Stack and similar platforms provide a unified management plane, so IT teams can monitor on-premises and cloud workloads from a single console, reducing admin effort. While on-premise still survives in high-control environments such as luxury or pharmacy, the operational burden of patches and hardware refresh cycles continues to erode its share.

SMEs accounted for 62.4% of deployments in 2025 and will continue to expand faster than their larger peers because per-resource pricing eliminates six-figure entry fees. Subscription bundles that include infrastructure, support, and future upgrades compress implementation to fewer than 90 days, allowing small chains to focus on merchandising rather than server upkeep. Vendors now ship pre-configured chart-of-accounts and promotional engines that drop into a new tenant without coding, shaving consultant hours, and accelerating value capture. The retail enterprise resource planning industry nevertheless faces a skills gap, as SMEs rarely employ full-time ERP administrators and must rely on vendor-managed services for troubleshooting.

Large enterprises buy deeper functionality such as multi-entity consolidations, global tax engines, and advanced supply-chain planning, which boosts average deal size. Yet complexity stretches deployments well beyond a year and inflates customization budgets, especially where franchise or joint-venture accounting demands unique data models. As a result, total enterprise license revenue outweighs sheer SME volume, and system integrators still build sizable practices around big-chain projects.

Geography Analysis

Asia-Pacific anchors the retail enterprise resource planning market, driven by stringent e-invoicing laws and exploding mobile commerce volume. Government portals in India processed billions of invoices in fiscal 2025, making automated tax reconciliation a must-have rather than a future wish. In China, over two-thirds of sizable retail chains already run cloud ERP, integrating local payment gateways directly into back-office ledgers to accelerate cash settlement. Southeast Asian sellers on regional marketplaces must meet 24-hour fulfillment promises, which requires ERP-driven inventory accuracy at the seller level rather than the warehouse level.

North America is a mature yet innovative landscape, shifting its focus from migration to optimization. Retailers fine-tune buy-online-pick-up-in-store workflows, trim split-shipment costs, and pilot AI recommendations inside store apps. Stringent state privacy laws drive granular role-based access controls and tokenization of customer identifiers inside ERP databases. Canada shows parallel trends, though bilingual requirements add another layer of design complexity.

Europe balances modernization with compliance. GDPR audits add months to cloud-vendor selection, but the upcoming VAT-in-the-Digital-Age program is already prompting chains to centralize onto platforms that can deliver continuous transaction reporting across 27 jurisdictions. Nordic retailers push early into composable microservices, swapping modules without full re-platforming, while Southern European chains focus on cost control through SaaS subscriptions that replace aging on-premise systems.

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor, Inc.

- Epicor Software Corporation

- The Sage Group plc

- Acumatica, Inc.

- LS Retail ehf.

- Odoo SA

- Brightpearl Limited

- Lightspeed Commerce Inc.

- IFS AB

- Blue Yonder Group, Inc.

- Aptos, LLC

- Cegid Group SA

- Retail Pro International, LLC

- CitiXsys India Private Limited

- Marg ERP Limited

- Logic ERP Solutions Private Limited

- Erply Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Shift to Cloud-Based ERP in Retail

- 4.2.2 Growing Omnichannel Retail Complexity

- 4.2.3 Rising Demand for Real-Time Inventory Visibility

- 4.2.4 Government Mandates for E-Invoicing and Digital Tax Compliance

- 4.2.5 AI-Driven Demand Forecasting Reduces Stockouts and Markdowns

- 4.2.6 Integration of Embedded Payments within Retail ERP Ecosystems

- 4.3 Market Restraints

- 4.3.1 High Implementation Costs and Budget Overruns

- 4.3.2 Data Security and Privacy Concerns

- 4.3.3 Shortage of Retail-Specific ERP Implementation Talent

- 4.3.4 Disruption Risk from Composable Microservices Architectures

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 Cloud-Based

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Organization Size

- 5.2.1 Small and Medium-Sized Enterprises

- 5.2.2 Large Enterprises

- 5.3 By Component

- 5.3.1 Finance and Accounting

- 5.3.2 Inventory and Warehouse Management

- 5.3.3 Sales and Customer Relationship Management

- 5.3.4 Human Resource Management

- 5.3.5 Supply Chain Management

- 5.3.6 Reporting and Analytics

- 5.3.7 Other Components

- 5.4 By Retail Format

- 5.4.1 Supermarkets and Hypermarkets

- 5.4.2 Specialty Stores

- 5.4.3 Department Stores

- 5.4.4 Convenience Stores

- 5.4.5 E-Commerce and Omnichannel Retailers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Australia

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Kenya

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Infor, Inc.

- 6.4.5 Epicor Software Corporation

- 6.4.6 The Sage Group plc

- 6.4.7 Acumatica, Inc.

- 6.4.8 LS Retail ehf.

- 6.4.9 Odoo SA

- 6.4.10 Brightpearl Limited

- 6.4.11 Lightspeed Commerce Inc.

- 6.4.12 IFS AB

- 6.4.13 Blue Yonder Group, Inc.

- 6.4.14 Aptos, LLC

- 6.4.15 Cegid Group SA

- 6.4.16 Retail Pro International, LLC

- 6.4.17 CitiXsys India Private Limited

- 6.4.18 Marg ERP Limited

- 6.4.19 Logic ERP Solutions Private Limited

- 6.4.20 Erply Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment