PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065579

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065579

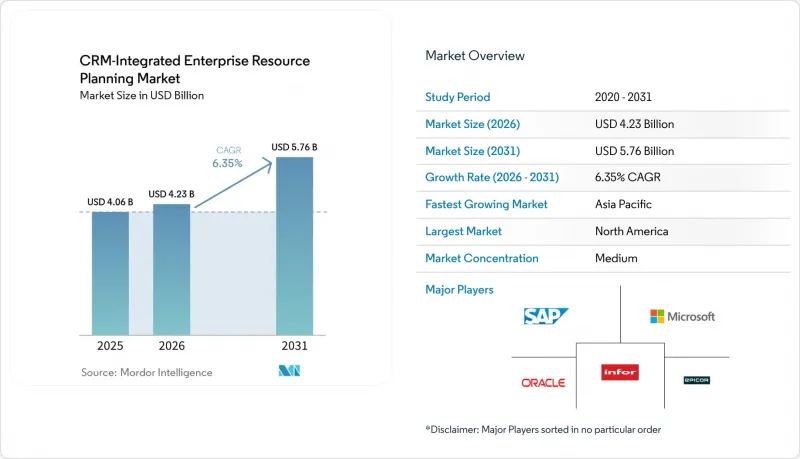

CRM-Integrated Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the cRM-Integrated eRP market size is expected to grow from USD 4.23 billion in 2026 to USD 5.76 billion by 2031 at a CAGR of 6.35% over 2026-2031.

This report is Segmented by Deployment Mode (On-Premises, Cloud, and Hybrid), Organization Size (Small and Medium Enterprises, and Large Enterprises), Component (Software and Services), Industry Vertical (Manufacturing, Retail and E-Commerce, Healthcare, Banking, Financial Services and Insurance, IT and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global CRM-Integrated Enterprise Resource Planning Market Trends and Insights

Cloud-First Digital Transformation Mandates

Cloud deployments are growing at a 14.20% CAGR through 2031, more than double the overall CRM-Integrated ERP market rate, as enterprises retire on-premises hardware in favor of scalable platforms that synchronize customer and transactional data in real time. Middle Eastern e-invoicing deadlines for 2026 and 2027, together with Japan's subsidy program that funds up to 50% of migration costs for SMEs, are accelerating this movement. Microsoft Dynamics 365 users have already cut average order-to-cash cycles by 30% after consolidating finance, inventory, and customer modules. Vendors are responding by embedding tax engines and localization packs that update automatically, removing the manual patching burden that plagued on-premises systems.

Need for Unified Customer and Operational Data

Fragmented databases inflate hidden costs that integrated suites eliminate. Enterprises with unified CRM-ERP platforms reported 40% fewer quote errors and 25% better on-time delivery because customer credit, inventory, and logistics data are validated before order confirmation. BFSI adopters are harnessing 360-degree customer views to recommend cross-sell offers in real time, while retailers synchronize online and store inventory to avert costly stock-outs. An API-first design underpins these gains, exposing event-driven endpoints that third-party apps consume without brittle batch interfaces.

High Total Cost of Ownership for Complex Deployments

Software licenses account for just 20%-30% of project spend, with the rest consumed by data migration, customization, and change management that can triple budgets. Consultants bill USD 200-350 per hour, while regulated industries face extra validation steps, such as FDA 21 CFR Part 11 testing, which adds another 25%-40%. Underfunded training often leads to user resistance, pushing failure rates above 60% when less than 15% of budgets go to change programs. Even cloud customers must guard against subscription sprawl, as unused SaaS seats can inflate recurring costs.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of AI-Driven Process Automation

- Rising Subscription-Based Licensing Models

- Cyber-Security and Data-Sovereignty Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployments secured 49.80% of 2025 revenue and are forecast to grow at 14.20% CAGR, more than twice the CRM-Integrated ERP market benchmark. Enterprises are routing capital away from servers toward analytics and innovation, while vendors reinforce regional capacity, such as Oracle's USD 8 billion Tokyo build-out. The EU Data Act eases provider switching by mandating data portability, yet China's localization rules temper public cloud adoption. Hybrid architectures act as a compromise, but integration latency and security management can erode savings if poorly engineered.

Hybrid and on-premises options persist where intellectual-property concerns or defense regulations prohibit external hosting. Pharmaceutical firms still maintain validated manufacturing modules on-site, even as they place HR and procurement in the cloud. Consequently, the CRM-Integrated ERP market continues to support multiple deployment models, though the usage tilt clearly favors SaaS.

Small and medium enterprises are advancing at a 15.90% CAGR, nearly triple the overall CRM-Integrated ERP market growth rate. Government programs such as India's INR 2,925.39 crore (USD 350 million) PACS ERP initiative subsidize rural cooperatives, while European Union Digital Decade grants aim to achieve 90% digitization of SMEs by 2030. Large enterprises, which still held 54.10% market share in 2025, face slower growth due to longer refresh cycles and entrenched custom code. Yet they are consolidating disparate stacks into unified suites to minimize integration overhead.

SMEs often skip on-premises footprints entirely, adopting modular cloud bundles that expand as business needs grow. The risk is subscription fatigue, as incremental add-ons can escalate monthly spend from USD 500 to USD 5,000, converging with perpetual ownership costs over time. Nevertheless, accessibility to AI features and real-time analytics is narrowing the capability gap between small firms and global incumbents.

Geography Analysis

North America led with 38.20% revenue in 2025. Mature penetration limits new-logo growth, steering vendors toward replacements, AI add-ons, and vertical expansions. Cross-border trade under USMCA is stimulating demand for suites that automate tariff and origin documentation in real time.

Asia-Pacific is the fastest-growing region, with a 13.80% CAGR. China's cybersecurity statutes obligate domestic hosting, giving local suppliers an edge and compelling multinationals to build in-country data centers. India's national PACS rollout, Japan's USD 660 million SME subsidy, and Oracle's Tokyo capacity expansion are powering rapid SaaS uptake. Diverse languages and regulations inflate localization costs but create openings for regional niche players.

Europe's growth is moderated by dual compliance with the EU Data Act and the U.K.'s post-Brexit data regime, which forces parallel governance frameworks for cross-border deployments. Germany, the United Kingdom, and France account for a significant share of regional spend, with Germany favoring on-premises control of proprietary scheduling algorithms. The Middle East is accelerating under mandatory e-invoicing laws, while Africa and South America remain emerging but demonstrate strong cloud adoption where legacy IT debt is minimal.

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor Inc.

- Epicor Software Corporation

- Workday Inc.

- Sage Group plc

- IFS AB

- Syspro (Pty) Ltd.

- Unit4 N.V.

- Acumatica, Inc.

- Plex Systems, Inc.

- QAD Inc.

- Deltek, Inc.

- Ramco Systems Limited

- Odoo SA

- Zoho Corporation Pvt. Ltd.

- Priority Software Ltd.

- TOTVS S.A.

- Epicor Kinetic (Epicor rebrand)

- Infor M3 (Infor solution)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-First Digital Transformation Mandates

- 4.2.2 Need for Unified Customer and Operational Data

- 4.2.3 Rapid Adoption of AI-Driven Process Automation

- 4.2.4 Rising Subscription-Based Licensing Models

- 4.2.5 Growing Demand for Vertical-Specific ERP Suites

- 4.2.6 Government Incentives for SME Digitalization

- 4.3 Market Restraints

- 4.3.1 High Total Cost of Ownership for Complex Deployments

- 4.3.2 Cyber-Security and Data-Sovereignty Concerns

- 4.3.3 Limited Qualified Implementation Talent Pool

- 4.3.4 Interoperability Challenges with Legacy Systems

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 On-Premises

- 5.1.2 Cloud

- 5.1.3 Hybrid

- 5.2 By Organization Size

- 5.2.1 Small and Medium Enterprises

- 5.2.2 Large Enterprises

- 5.3 By Component

- 5.3.1 Software

- 5.3.2 Services

- 5.4 By Industry Vertical

- 5.4.1 Manufacturing

- 5.4.2 Retail and E-Commerce

- 5.4.3 Healthcare

- 5.4.4 Banking, Financial Services and Insurance

- 5.4.5 Information Technology and Telecommunications

- 5.4.6 Government

- 5.4.7 Other Industry Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Infor Inc.

- 6.4.5 Epicor Software Corporation

- 6.4.6 Workday Inc.

- 6.4.7 Sage Group plc

- 6.4.8 IFS AB

- 6.4.9 Syspro (Pty) Ltd.

- 6.4.10 Unit4 N.V.

- 6.4.11 Acumatica, Inc.

- 6.4.12 Plex Systems, Inc.

- 6.4.13 QAD Inc.

- 6.4.14 Deltek, Inc.

- 6.4.15 Ramco Systems Limited

- 6.4.16 Odoo SA

- 6.4.17 Zoho Corporation Pvt. Ltd.

- 6.4.18 Priority Software Ltd.

- 6.4.19 TOTVS S.A.

- 6.4.20 Epicor Kinetic (Epicor rebrand)

- 6.4.21 Infor M3 (Infor solution)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment