PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065770

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065770

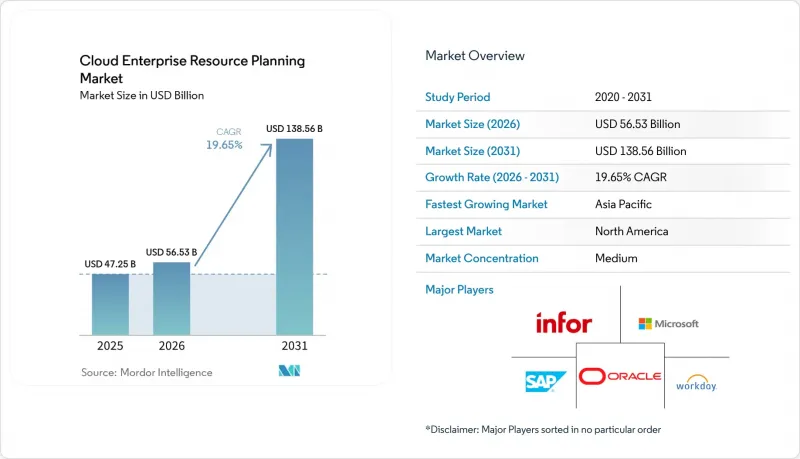

Cloud Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the cloud enterprise resource planning market size is projected to expand from USD 47.25 billion in 2025 and USD 56.53 billion in 2026 to USD 138.56 billion by 2031, registering a CAGR of 19.65% between 2026 and 2031.

This report is Segmented by Component (Solutions and Services), Deployment Model (Public Cloud and Private Cloud), End-User Enterprise Size (Large Enterprises and Small and Medium Enterprises), Business Function (Finance and Accounting, and More), End-User Industry (BFSI, IT and Telecom, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Cloud Enterprise Resource Planning Market Trends and Insights

AI-driven predictive analytics integration

Artificial Intelligence transforms cloud ERP systems from tools focused on backward-looking reporting to platforms that enable forward-looking decision-making. Organizations that have integrated AI into their ERP systems have reported significant operational improvements, including a 25% reduction in delivery times and a 15% decrease in operational costs. These improvements are achieved through real-time supply chain algorithms that optimize processes and improve efficiency. SAP revealed that AI-powered features were included in half of all ERP deals closed in Q4 2024, highlighting the growing demand for intelligent ERP solutions. Similarly, Oracle experienced a 115% sequential growth in its multicloud database services with integrated AI capabilities in Q4 2025, underscoring the company's focus on delivering intelligent workflows and advanced decision-support systems. Manufacturing firms elevate budgets to embed predictive maintenance and production planning, reinforcing AI as a competitive necessity rather than a fringe add-on.

Subscription affordability for SMEs

Subscription pricing eliminates the capital-expenditure barrier that previously prevented smaller firms from accessing enterprise-grade software. This shift has enabled companies of all sizes to adopt advanced solutions without significant upfront investments. For instance, NetSuite's customer base of 18,844 in 2024 accounted for a 10.35% share of the financial-reporting market, showcasing the growing adoption of subscription-based ERP solutions. Additionally, Vista Equity Partners' USD 2 billion acquisition of Acumatica underscores the growing importance of predictable monthly fees, which align well with the cash-flow needs of small and medium enterprises (SMEs). This model not only supports SMEs in managing their financial constraints but also provides vendors with a steady revenue stream, fostering growth opportunities. As a result, SMEs increasingly view cloud ERP as a strategic tool for efficiently scaling their operations without the need to hire extensive IT teams.

Legacy on-premise integration complexity

Enterprises with decades-old custom code face significant challenges during migration processes, often resulting in extended timelines. To address these difficulties, SAP has extended mainstream support for its systems until 2033, providing organizations with additional time to manage these transitions effectively. Manufacturing firms, in particular, experience prolonged project durations due to the complexity of their specialized production systems and the need for rigorous validation cycles. These factors frequently lead to project budgets exceeding initial estimates, as companies allocate additional resources to ensure successful implementation and compliance with operational requirements.

Other drivers and restraints analyzed in the detailed report include:

- Composable micro-service ERP architectures

- Data-sovereignty-driven sovereign-cloud roll-outs

- Multi-tenant security and compliance concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions accounted for 67.10% of the cloud enterprise resource planning market share in 2025, as enterprises favored integrated suites that streamline finance, supply chain, and HR in a single environment. The dominance stems from the appeal of a single data model that eliminates silos and simplifies governance. Services, however, post the fastest 24.95% CAGR and will deepen the market size as organizations rely on consulting partners for migration roadmaps and continual optimization. Implementation engagements are expanding because legacy landscapes require complex data cleansing and process reengineering. Managed services are gaining further traction among SMEs that prefer to outsource ERP maintenance and focus on revenue-generating activities. The rise of AI features increases demand for training and change management, reinforcing service revenue resilience.

The solutions segment is also buoyed by vendor investments in preconfigured industry templates that shrink deployment timelines. Vendors bundle analytics and robotic process automation add-ons to increase subscription value. As AI adoption widens, solution roadmaps increasingly emphasize embedded machine learning for anomaly detection. These innovations keep solution revenue dominant while allowing services partners to monetize lifecycle support. Overall, platform consolidation continues to shape purchasing behavior and sustains the broader cloud ERP market.

Public cloud captured 63.78% of the market share in 2025, supported by consumption pricing, automated upgrades, and globally distributed data centers. Standardized configurations reduce implementation costs and enable rapid access to new features, resonating with firms seeking speed over heavy customization. The private cloud model, posting a 22.10% CAGR, reflects rising regulatory scrutiny that requires isolated environments without sacrificing cloud elasticity. Industries such as banking and healthcare require greater control over encryption, audit trails, and localization.

Hybrid strategies emerge as a pragmatic middle ground. Firms keep sensitive workloads within private instances while pushing less-regulated modules to public regions, thereby controlling risk and optimizing costs. This flexibility aligns with sovereign-cloud mandates that demand in-country data residency. Vendor roadmaps now include automated workload shuttling and consistent policy engines across public and private footprints. Collectively, deployment diversity reduces vendor lock-in fears and enlarges the cloud ERP market size by broadening buyer segments.

Geography Analysis

North America accounted for 35.10% of global revenue in 2025, driven by mature cloud infrastructure and a deep ecosystem of implementation partners. Enterprises use the cloud enterprise resource planning market to refresh legacy suites, consolidate data silos, and align with evolving compliance regimes such as the US SEC modernization rules. The presence of major hyperscalers ensures low-latency access and continuous feature delivery. In addition, cross-border entities appreciate region-wide data-privacy frameworks that simplify multinational rollouts.

Asia-Pacific delivers the fastest CAGR of 27.10%, driven by government digitalization programs and accelerated economic growth. China's USD 9.2 billion cloud infrastructure spend in 2023, with Alibaba Cloud at 39%, Huawei at 19%, and Tencent at 15%, frames the scale of regional investment. Southeast Asian countries tap this infrastructure through strategic alliances, while Japan emphasizes modernizing manufacturing supply chains. The cloud ERP market gains additional lift from local software champions that package industry-specific solutions for export-oriented SMEs.

Europe shows stable expansion, rooted in GDPR compliance and sovereign cloud roadmaps. Enterprises adopt hybrid models that keep sensitive data within EU borders while harnessing foreign regions for less-regulated workflows. Hyperscalers partner with local telecom firms to build trusted cloud zones, enabling public-sector projects that require local control. Meanwhile, Middle East and Africa observe emerging deployments as governments launch e-government programs and diversify economies away from hydrocarbons. These dynamics together enlarge the market size and deepen vendor localization efforts.

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor Global Solutions, Inc.

- Workday, Inc.

- NetSuite Inc.

- Acumatica, Inc.

- Epicor Software Corporation

- Sage Group plc

- Certinia Inc.

- IFS AB

- Unit4 NV

- Deltek, Inc.

- Ramco Systems Ltd.

- Plex Systems, Inc.

- Odoo SA

- Sage Intacct, Inc.

- QAD Inc.

- SYSPRO (Pty) Ltd.

- Kingdee International Software Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-Driven Predictive Analytics Integration

- 4.2.2 Subscription Affordability for SMEs

- 4.2.3 Composable Micro-Service ERP Architectures

- 4.2.4 Data-Sovereignty-Driven Sovereign-Cloud Roll-Outs

- 4.2.5 Marketplace-Embedded ERP APIs for Micro-Enterprises

- 4.3 Market Restraints

- 4.3.1 Legacy On-Premise Integration Complexity

- 4.3.2 Multi-Tenant Security and Compliance Concerns

- 4.3.3 Hyperscaler Egress-Fee Inflation of TCO

- 4.3.4 Low-Code ERP-Extension Talent Shortage

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Model

- 5.2.1 Public Cloud

- 5.2.2 Private Cloud

- 5.3 By End-user Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Business Function

- 5.4.1 Finance and Accounting

- 5.4.2 Human Resources

- 5.4.3 Sales and Marketing

- 5.4.4 Supply Chain and Operations

- 5.4.5 Other Business Functions

- 5.5 By End-User Industry

- 5.5.1 BFSI

- 5.5.2 IT and Telecom

- 5.5.3 Manufacturing

- 5.5.4 Government

- 5.5.5 Retail and E-commerce

- 5.5.6 Healthcare

- 5.5.7 Other End-User Industries

- 5.6 By Region

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Infor Global Solutions, Inc.

- 6.4.5 Workday, Inc.

- 6.4.6 NetSuite Inc.

- 6.4.7 Acumatica, Inc.

- 6.4.8 Epicor Software Corporation

- 6.4.9 Sage Group plc

- 6.4.10 Certinia Inc.

- 6.4.11 IFS AB

- 6.4.12 Unit4 NV

- 6.4.13 Deltek, Inc.

- 6.4.14 Ramco Systems Ltd.

- 6.4.15 Plex Systems, Inc.

- 6.4.16 Odoo SA

- 6.4.17 Sage Intacct, Inc.

- 6.4.18 QAD Inc.

- 6.4.19 SYSPRO (Pty) Ltd.

- 6.4.20 Kingdee International Software Group

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment