PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065583

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065583

North America Integrated GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

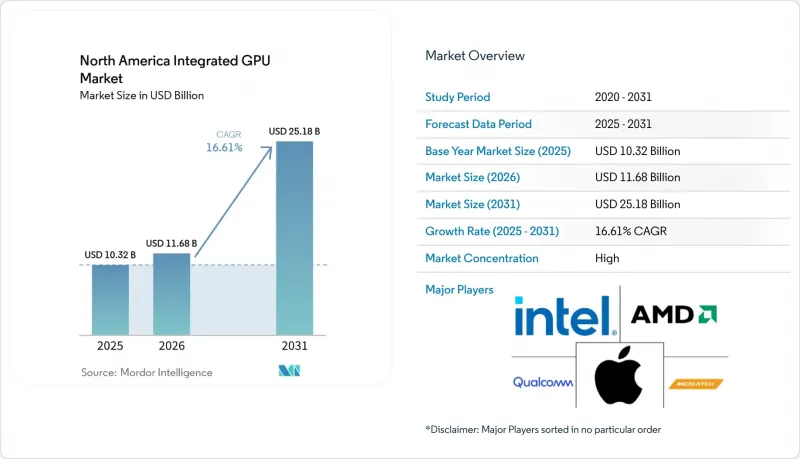

According to Mordor Intelligence, the north america integrated GPU market size was USD 10.32 billion in 2025 and is projected to reach USD 25.18 billion by 2031 at a CAGR of 16.61% during 2026-2031.

This report is Segmented by Device Category (Desktop and Laptop Processors, Mobile SoCs (Smartphones and Tablets), Embedded and Industrial SoCs, and Server and Data Center Processors With Integrated Graphics), Performance Tier (Entry-Level (less Than USD 50), Mainstream (USD 50 - USD 150), Performance (USD 150 - USD 300), and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

North America Integrated GPU Market Trends and Insights

AI PC Refresh Cycle After Windows 10 End of Support

Windows 10 reached end of support on October 14, 2025, which removed regular security and feature updates for systems that were still widely used across enterprise and SMB fleets. In North America, that change turned PC replacement into a more urgent decision for IT teams working under security and compliance requirements. Intel's Core Ultra Series 3 Panther Lake processors entered commercial availability at CES in January 2026 as the first client chips built on Intel 18A, with up to 180 Platform TOPS and an Xe3 Arc GPU that moved performance well above the prior generation. Microsoft's Copilot+ PC threshold of 40 dedicated NPU TOPS also placed many older systems outside the preferred hardware pool for on-device AI work. This pairing of a firm support deadline and a clear hardware step-up is pulling refresh budgets forward instead of letting companies delay purchases. It is also supporting near-term expansion in the North America integrated GPU market because buyers are paying for AI readiness rather than only replacing aging PCs.

Rising GenAI Workloads on Premium Smartphone and Tablet SoCs

Apple's M5, released on October 15, 2025, used third-generation 3-nanometer technology, a 10-core GPU, dedicated Neural Accelerators in each GPU core, and 153 GB/s of unified memory bandwidth. Apple said the chip delivered more than 4x peak GPU AI compute versus M4, which raised the performance standard for premium notebooks, tablets, and spatial devices sold in the region. Qualcomm's heterogeneous design pairs the Adreno GPU with the Hexagon NPU on the same die, which improves on-device token generation by avoiding off-chip data movement and reducing memory latency. This matters in the North America integrated GPU market because premium users increasingly expect voice, vision, translation, and assistant features to run locally with better responsiveness and privacy. Micron's 1-gamma LPDDR5X, shipped in June 2025 at 10.7 Gbps, cut power use by 20% and improved AI voice-translation response times by more than 50% in the company's Llama 2 testing. Higher memory throughput is therefore improving sustained iGPU usability in flagship smartphones and tablets rather than only lifting headline benchmark scores.

Performance Ceiling Versus Discrete GPUs in Gaming and Workstations

Integrated graphics still share system memory with the CPU, which keeps available bandwidth well below discrete cards that use GDDR6X or HBM. Intel said Panther Lake with Xe3 graphics moved closer to entry-level discrete mobile performance, but that still leaves a large gap to higher-end gaming and workstation cards. In North America, that gap matters because gaming, 3D content creation, architectural visualization, and simulation remain concentrated in professional segments that pay the highest per-unit prices. These workloads also require sustained memory bandwidth and VRAM pools that can exceed 24 GB, which current iGPU platforms do not match in multi-user or multi-model settings. The issue for vendors is less about total shipment volumes and more about revenue density, because the premium end of graphics spending still sits in discrete hardware. As a result, the North America integrated GPU market can grow rapidly without fully displacing the most profitable workstation and enthusiast categories.

Other drivers and restraints analyzed in the detailed report include:

- Cost and Power Advantage Versus Discrete Graphics in Mainstream Systems

- Growth in Edge AI and Industrial HMI SoCs

- Shared Memory Bandwidth and Capacity Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mobile SoCs held 49.55% of device-category revenue in 2025, the largest slice of the North America integrated GPU market share within this segmentation. Apple's strength in premium smartphones and tablets helped sustain that lead, while Qualcomm continued to build its role in higher-value Windows-on-ARM systems and premium mobile computing. Desktop and laptop processors remain central to the North America integrated GPU market because enterprise refresh demand is now tied to AI-ready client hardware rather than only routine replacement. AMD said its mobile processor unit share rose to 26.0% in Q4 2025, reflecting stronger Ryzen AI uptake in enterprise and premium consumer systems. Embedded and industrial SoCs stayed smaller in revenue terms, but they remained widely distributed across factory automation, energy, and retail equipment deployments.

Server and Data Center Processors with Integrated Graphics are projected to expand at a 16.98% CAGR through 2031, making them the fastest-growing device category. That growth reflects a practical need at the rack edge, where inference, visualization, media handling, and local display output often need to run together without the cost of a discrete add-in card. Intel highlighted this direction with Crescent Island, an Xe3P-based data center GPU announced with 160 GB of LPDDR5X memory for air-cooled enterprise inference workloads. AMD also said in November 2025 that it expected very rapid expansion in data center AI revenue, which supports wider use of embedded graphics IP across edge-oriented server platforms. Across the North America integrated GPU industry, this category is gaining from lower idle power, simpler deployment, and branch and factory use cases that do not justify a separate accelerator card.

List of Companies Covered in this Report:

- Intel Corporation

- Advanced Micro Devices, Inc.

- Apple Inc.

- Qualcomm Incorporated

- MediaTek Inc.

- NVIDIA Corporation

- Samsung Electronics Co., Ltd.

- NXP Semiconductors N.V.

- Renesas Electronics Corporation

- Texas Instruments Incorporated

- Arm Holdings plc

- Imagination Technologies Group plc

- Google LLC

- STMicroelectronics N.V.

- Synaptics Incorporated

- Socionext Inc.

- Telechips Inc.

- Amlogic, Inc.

- Rockchip Electronics Co., Ltd.

- Microchip Technology Incorporated

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 AI PC Refresh Cycle After Windows 10 End of Support

- 4.3.2 Rising GenAI Workloads on Premium Smartphone and Tablet SoCs

- 4.3.3 Cost and Power Advantage Versus Discrete Graphics in Mainstream Systems

- 4.3.4 Growth in Edge AI and Industrial HMI SoCs

- 4.3.5 LPDDR5X and Unified Memory Bandwidth Lifting iGPU Usability

- 4.3.6 Single-Chip Platform Optimization Under Tariff Pressure

- 4.4 Market Restraints

- 4.4.1 Performance Ceiling Versus Discrete GPUs in Gaming and Workstations

- 4.4.2 Shared Memory Bandwidth and Capacity Constraints

- 4.4.3 Tariffs and Memory Inflation Raising System Prices

- 4.4.4 Limited Fit for Integrated Graphics in Server and Data Center Deployments

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Category

- 5.1.1 Desktop and Laptop Processors

- 5.1.2 Mobile SoCs (Smartphones and Tablets)

- 5.1.3 Embedded and Industrial SoCs

- 5.1.4 Server and Data Center Processors with Integrated Graphics

- 5.2 By Performance Tier

- 5.2.1 Entry-Level (Less than USD 50)

- 5.2.2 Mainstream (USD 50 - USD 150)

- 5.2.3 Performance (USD 150 - USD 300)

- 5.2.4 High-Performance (Greater than USD 300)

- 5.3 By Country

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Intel Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Apple Inc.

- 6.4.4 Qualcomm Incorporated

- 6.4.5 MediaTek Inc.

- 6.4.6 NVIDIA Corporation

- 6.4.7 Samsung Electronics Co., Ltd.

- 6.4.8 NXP Semiconductors N.V.

- 6.4.9 Renesas Electronics Corporation

- 6.4.10 Texas Instruments Incorporated

- 6.4.11 Arm Holdings plc

- 6.4.12 Imagination Technologies Group plc

- 6.4.13 Google LLC

- 6.4.14 STMicroelectronics N.V.

- 6.4.15 Synaptics Incorporated

- 6.4.16 Socionext Inc.

- 6.4.17 Telechips Inc.

- 6.4.18 Amlogic, Inc.

- 6.4.19 Rockchip Electronics Co., Ltd.

- 6.4.20 Microchip Technology Incorporated

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment