PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065585

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065585

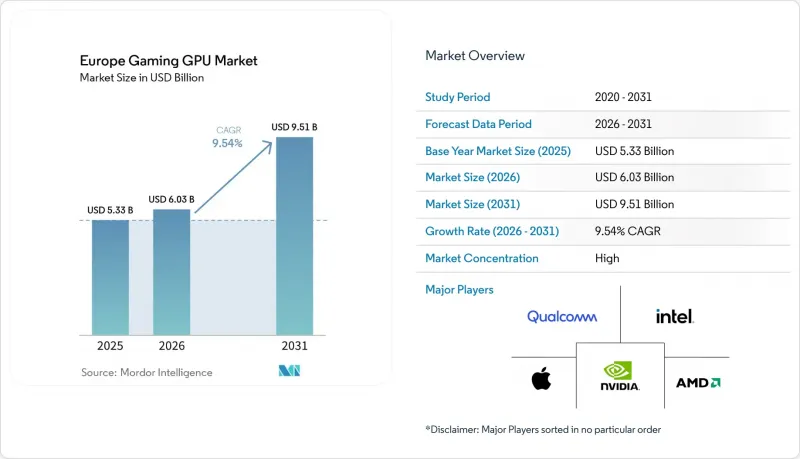

Europe Gaming GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the europe gaming GPU market size is projected to be USD 5.33 billion in 2025, USD 6.03 billion in 2026, and reach USD 9.51 billion by 2031, growing at a CAGR of 9.54% from 2026 to 2031.

This report is Segmented by GPU Type (Discrete GPUs, and Integrated GPUs), Device Type (Gaming Desktops, Gaming Laptops, and Smartphones and Tablets (Mobile Gaming)), End-User Type (Casual Gamers, and Enthusiast and Professional Gamers), Memory Type (GDDR6, GDDR6X, Legacy Graphics Memory, and Unified Memory), and Country. The Market Forecasts are Provided in Terms of Value (USD).

Europe Gaming GPU Market Trends and Insights

Rising Esports And Competitive PC Gaming Participation

Competitive gaming demand in Europe rests on a very large player base that continues to feed more performance-focused hardware purchases over time. Video Games Europe and the European Games Developer Federation stated that 54% of Europeans aged 6-64 played video games in 2024, which kept the addressable hardware base broad across the region. That broad participation supports a steady funnel from casual play into organized and performance-led gaming, where refresh rate, responsiveness, and visual stability matter more. Germany's games hardware and accessories segment grew 12% in 2025 to EUR 3.40 billion (USD 3.71 billion), showing that players were still willing to spend on gaming equipment even in a higher-cost environment. Gaming PC accessories rose 13% to EUR 1.37 billion (USD 1.49 billion), which points to healthy component demand in one of the region's most important hardware markets. This keeps the Europe gaming GPU market tied to repeated performance-led upgrades rather than to a single purchase cycle.

Demand for Real-Time Ray Tracing and AI-Upscaling

AI-upscaling is now a standard purchase factor in the Europe gaming GPU market rather than an optional premium feature. NVIDIA said DLSS 4, introduced with the GeForce RTX 5000 generation, had reached more than 980 games and applications by May 2026. AMD also positioned AI-assisted rendering as a core feature when it launched the Radeon RX 9000 series and RDNA 4 architecture with FSR 4 in February 2025.NVIDIA further stated that Multi Frame Generation on GeForce RTX 50 Series hardware can increase effective frame output by up to 8x in supported workloads. These technologies are pushing more buyers to look beyond basic 1080p performance and target cards that can sustain higher visual settings over a longer ownership period. That change is lifting the baseline specification that vendors must meet across the Europe gaming GPU market.

High Upfront Cost of Gaming GPUs and Systems

The current upgrade cycle still carries a high upfront cost burden for many buyers in the Europe gaming GPU market. AMD launched the Radeon RX 9070 at USD 549 and the RX 9070 XT at USD 599 in 2025, while Intel positioned the Arc B580 at USD 249 in late 2024. Even before taxes, partner premiums, and the cost of a full system are added, those levels keep current-generation hardware far from impulse-purchase territory for mainstream households. That pressure narrows the active buyer base for higher-VRAM and higher-ray-tracing tiers, even when long-term performance value is clear. It also pushes some users toward longer retention of existing systems or toward streamed gaming services instead of direct replacement. The result is a market where spending remains healthier than unit turnover because enthusiasts continue to buy sooner than mass-market users.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption of Gaming Laptops and Portable High-Performance PCs

- Mobile Gaming Monetization Moving Toward Higher-Fidelity Titles

- Mature Installed Base Lengthening Replacement Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Discrete GPUs commanded a 74.44% share of the Europe gaming GPU market in 2025 and are projected to expand at a 9.90% CAGR through 2031. Dedicated graphics hardware remains central because gaming performance still depends on sustained compute, stronger thermal headroom, and direct support for advanced visual workloads. NVIDIA's DLSS 4 footprint across more than 980 games and applications shows why feature-rich discrete cards continue to hold the strongest performance position. AMD reinforced that position in 2025 when it launched the Radeon RX 9000 series with RDNA 4, 16 GB GDDR6 configurations, and FSR 4 support for current-generation gaming. In practical terms, the largest slice of the Europe gaming GPU market continues to sit with cards designed for direct gaming load rather than for shared system use.

Integrated GPUs account for the remaining segment share and remain more relevant for casual play, thin devices, and cloud gaming access points. Intel's Arc B-series launch showed that the company still wants a role in value-oriented graphics, even though the strongest gaming demand remains concentrated in discrete categories. Cloud services from NVIDIA and Deutsche Telekom also reduce the need for a powerful local GPU in lighter gaming scenarios, which helps integrated and hybrid setups stay viable at the lower end. Even so, the Europe gaming GPU industry still draws most of its revenue and product attention from discrete silicon because premium gaming features are advancing fastest there.

Gaming desktops held 44.31% share of the Europe gaming GPU market size in 2025, which kept towers as the largest device category. Their lead reflects stronger upgrade flexibility, better cooling, and the ability to replace a graphics card without changing the full system. In enthusiast-led markets, desktops remain the clearest route to stepwise GPU upgrades rather than full hardware replacement. Germany's 2025 growth in gaming hardware and accessories supports that pattern because component spending remained active in one of the region's most important gaming hardware markets. That keeps the Europe gaming GPU market closely linked to desktop component demand, even as other device types expand.

Gaming laptops are projected to grow at a 10.12% CAGR through 2031, making them the fastest-growing device type in the Europe gaming GPU market. ASUS highlighted this shift in 2026 with Zephyrus G14 and G16 systems that carried up to RTX 5080 Laptop GPU and RTX 5090 Laptop GPU options in Nordic markets. NVIDIA's GeForce NOW Blackwell upgrade also increased the appeal of portable systems by enabling high-resolution streaming on devices that do not carry the same local GPU headroom. Smartphones and tablets add a third route because 5G cloud gaming services expose mobile users to premium GPU rendering without changing the device form factor.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Qualcomm Incorporated

- Apple Inc.

- MediaTek Inc.

- Samsung Electronics Co., Ltd.

- ASUSTeK Computer Inc.

- Micro-Star International Co., Ltd.

- GIGA-BYTE Technology Co., Ltd.

- Acer Inc.

- Dell Technologies Inc.

- HP Inc.

- Lenovo Group Limited

- Razer Inc.

- SAPPHIRE Technology Limited

- ASRock Inc.

- ZOTAC Technology Limited

- Palit Microsystems Ltd.

- TUL Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Rising Esports and Competitive PC Gaming Participation

- 4.3.2 Demand for Real-Time Ray Tracing and AI-Upscaling

- 4.3.3 Rising Adoption of Gaming Laptops and Portable High-Performance PCs

- 4.3.4 Mobile Gaming Monetization Moving Toward Higher-Fidelity Titles

- 4.3.5 5G Standalone Cloud Gaming Bundles Expanding Premium GPU Exposure

- 4.3.6 16 GB VRAM Expectations Reshaping Upgrade Decisions

- 4.4 Market Restraints

- 4.4.1 High Upfront Cost of Gaming GPUs and Systems

- 4.4.2 Mature Installed Base Lengthening Replacement Cycles

- 4.4.3 GDDR6 and GDDR6X Supply Tightness Inflating Midrange GPU Prices

- 4.4.4 EU Energy and Standby Compliance Pressure on High-TDP Hardware

- 4.5 Industry Value Chain Analysis

- 4.6 Supply Chain Analysis

- 4.7 Regulatory Landscape

- 4.8 Technological Outlook

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By GPU Type

- 5.1.1 Discrete GPUs

- 5.1.2 Integrated GPUs

- 5.2 By Device Type

- 5.2.1 Gaming Desktops

- 5.2.2 Gaming Laptops

- 5.2.3 Smartphones and Tablets (Mobile Gaming)

- 5.3 By End-User Type

- 5.3.1 Casual Gamers

- 5.3.2 Enthusiast and Professional Gamers

- 5.4 By Memory Type

- 5.4.1 GDDR6

- 5.4.2 GDDR6X

- 5.4.3 Legacy Graphics Memory

- 5.4.4 Unified Memory

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Qualcomm Incorporated

- 6.4.5 Apple Inc.

- 6.4.6 MediaTek Inc.

- 6.4.7 Samsung Electronics Co., Ltd.

- 6.4.8 ASUSTeK Computer Inc.

- 6.4.9 Micro-Star International Co., Ltd.

- 6.4.10 GIGA-BYTE Technology Co., Ltd.

- 6.4.11 Acer Inc.

- 6.4.12 Dell Technologies Inc.

- 6.4.13 HP Inc.

- 6.4.14 Lenovo Group Limited

- 6.4.15 Razer Inc.

- 6.4.16 SAPPHIRE Technology Limited

- 6.4.17 ASRock Inc.

- 6.4.18 ZOTAC Technology Limited

- 6.4.19 Palit Microsystems Ltd.

- 6.4.20 TUL Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment