PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065598

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065598

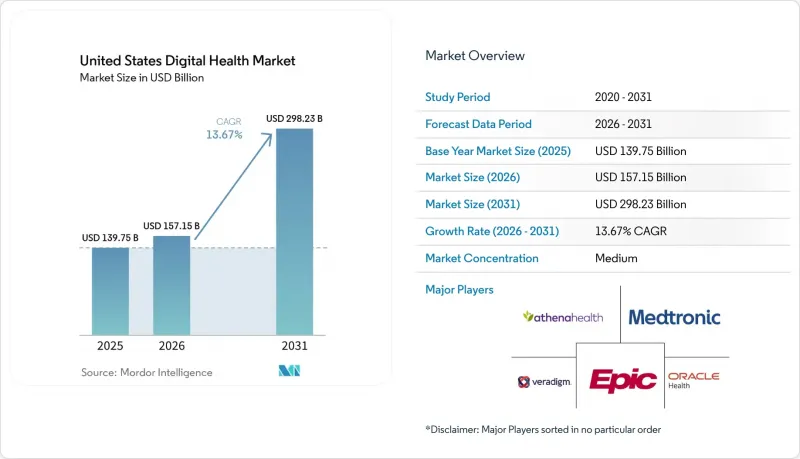

United States Digital Health - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states digital health market size is expected to increase from USD 139.75 billion in 2025 to USD 157.15 billion in 2026 and reach USD 298.23 billion by 2031, growing at a CAGR of 13.67% over 2026-2031.

This report is Segmented by Solution Type (Tele-Healthcare, Mhealth, Digital Health Systems, Healthcare Analytics and Clinical AI, Digital Therapeutics), Component (Software, Hardware, Services), Application (Diabetes Management, and More), and End User (Healthcare Providers, Payers, Patients and Consumers, Employers and Plan Sponsors). Market Forecasts are in Value (USD).

United States Digital Health Market Trends and Insights

Telehealth Normalization Across Care Pathways

The United States digital health market continues to benefit from stronger policy support for virtual care across routine care settings. Congress extended Medicare telehealth flexibilities through December 31, 2027, which removed a major near-term policy risk for providers and vendors building care models around virtual access. The 2026 Medicare Physician Fee Schedule also made virtual direct supervision and unlimited subsequent inpatient telehealth visits a permanent part of Medicare coverage, which moved key provisions out of the temporary extension cycle. Evidence from the American Telemedicine Association showed a 74% substitution rate for virtual visits across 1.7 million beneficiaries in 25 states, which supports the view that telehealth is replacing a large share of physical visits rather than creating excess use. Teladoc Health's 2025 benchmark survey also found that hospitals are redesigning virtual care around ongoing engagement instead of one-time access, which supports longer-duration payer contracts and recurring revenue models. Virtual behavioral health remains the clearest near-term use case because the 2026 rule preserved important care delivery flexibility for federally qualified and rural clinics.

Chronic Disease and Aging-Driven Remote Management Demand

The United States digital health market is also being pulled forward by the rising burden of chronic disease and by an aging population that will need more support outside traditional care settings. The Population Reference Bureau reported that the caregiver ratio for Americans aged 80 and older is expected to fall to 3 to 1 by 2040 from 6 to 1 in 2025, which points to a widening service gap that remote management tools can help fill. CMS launched the ACCESS model on July 5, 2026, and tied it to conditions that affect more than two-thirds of Medicare beneficiaries, including hypertension, diabetes, chronic musculoskeletal pain, and depression. That payment design pushes digital health vendors to show outcomes early, because reimbursement is linked to measurable results rather than simple enrollment or engagement volume. Virta Health reached a USD 200 million annualized revenue run rate in 2026 after several years of clinical evidence building, and its nutrition-based metabolic care model showed improvements in 19 of 21 inflammatory markers in peer-reviewed research. Dexcom also reported 15% year-on-year revenue growth in Q1 2026 after launching the G7 15 Day CGM in the United States, which shows how device innovation and clinical validation can reinforce each other in chronic care programs.

Cybersecurity and Health-Data Breach Exposure

Cybersecurity remains a major drag on adoption because buyers treat health data risk as both a financial and a clinical issue. The American Hospital Association reported in 2025 that more than 80% of stolen protected health information records came from third-party vendors and business associates rather than the core EHR, which shifts attention toward external integrations and vendor controls. That pattern is important in the United States digital health market because many solutions depend on multiple data exchanges across software vendors, monitoring devices, claims systems, and care delivery partners. It also means procurement cycles are becoming more security heavy, especially when health systems are evaluating smaller vendors without long operating histories. The practical effect is slower onboarding, more contract review, and higher implementation cost. Vendors that cannot support enterprise-grade security expectations are likely to face added friction even when their clinical use case is compelling.

Other drivers and restraints analyzed in the detailed report include:

- AI-Enabled Workflow Automation and Ambient Documentation Adoption

- CMS Reimbursement Expansion for RPM, RTM, and Digital Mental Health Tools

- Point-Solution Sprawl and EHR Integration Bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tele-Healthcare held 56.76% of the United States digital health market in 2025, which kept it as the largest solution segment by revenue. That position reflects long-standing investment in virtual urgent care, primary care, specialty care, and behavioral care delivery. The segment is now supported by policy continuity, because Medicare telehealth flexibilities have been extended and key virtual supervision and inpatient visit provisions have been made permanent. The United States digital health market size for Tele-Healthcare remained anchored by the depth of payer and employer benefit integration already built around virtual access in 2025. Teladoc's BetterHelp transition toward an insurance-covered model and its targeted run rate of at least USD 125 million in insurance revenue by Q4 2026 show that behavioral telehealth is moving toward closer payer alignment. Virtual specialty care is also gaining room because it can help address shortages in endocrinology, cardiology, and psychiatry without requiring new physical capacity.

mHealth is the fastest-growing solution segment, with the United States digital health market size for mHealth projected to expand at 14.49% CAGR through 2031. Demand is being led by CGM adoption, wearable cardiac monitoring, and mobile applications that support continuous engagement instead of episodic intervention. Dexcom raised its 2026 revenue outlook to USD 5.2 billion to USD 5.3 billion after the US launch of G7 15 Day and the FDA clearance of Smart Basal, which shows continued strength in connected metabolic care. The Stelo over-the-counter platform is also broadening the addressable base beyond insulin users, and Prime Therapeutics will begin covering CGM for all people with diabetes from summer 2026, including more than 7 million type 2 non-insulin lives. In the US digital health industry, this shifts value toward solutions that can stay with patients between visits and generate usable data for both consumers and clinicians.

Services accounted for 45.73% of the United States digital health market in 2025, which made it the largest component segment. This reflects the reality that implementation, workflow redesign, training, and managed support remain necessary for digital tools to deliver lasting clinical and financial value. Many provider organizations still face internal capacity limits, so service layers continue to act as the practical bridge between software purchase and real-world use. The US digital health market share in this segment stayed high because technology alone rarely solves integration, operational change, or care coordination challenges. This also explains why enterprise buyers often favor vendors that can combine product capability with deployment support.

Software is the fastest-growing component segment at 15.49% CAGR through 2031, and it is benefiting most from ambient documentation, analytics, revenue cycle automation, and patient engagement use cases. Oracle's AI-native ambulatory EHR received ASTP/ONC certification in 2025, and the company expanded its Clinical AI Agent into inpatient and emergency settings in 2026, which shows how quickly AI is being built into core systems. Amazon One Medical also set a new benchmark for patient-facing digital engagement when it launched Health AI and later extended it to all US Amazon customers in 2026. Hardware remains supported by monitoring device volumes, but price pressure on sensors is limiting differentiation at the commodity end. In the US digital health industry, software is capturing more value because it can connect clinical evidence, workflow efficiency, and patient engagement in a single layer.

List of Companies Covered in this Report:

- American Well

- Amazon One Medical

- athenahealth

- Dexcom

- Doximity

- Epic Systems

- Headspace Health

- HealthTap

- Hims & Hers Health

- Hinge Health

- Included Health

- MDLIVE

- Medtronic

- Omada Health

- Oracle Health

- Talkspace

- Teladoc Health

- Veradigm

- Virta Health

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Telehealth Normalization Across Care Pathways

- 4.2.2 Chronic Disease and Aging-Driven Remote Management Demand

- 4.2.3 AI-Enabled Workflow Automation and Ambient Documentation Adoption

- 4.2.4 CMS Reimbursement Expansion for RPM, RTM, And Digital Mental Health Tools

- 4.2.5 TEFCA-Scale Interoperability and Real-Time Prior Authorization Enablement

- 4.2.6 ACCESS Model and TEMPO Pilot Open Outcome-Based Commercialization Paths

- 4.3 Market Restraints

- 4.3.1 Cybersecurity And Health-Data Breach Exposure

- 4.3.2 Reimbursement Variability and Proof-Of-ROI Pressure

- 4.3.3 State-By-State Privacy and Consumer Health Data Compliance Patchwork

- 4.3.4 Point-Solution Sprawl and EHR Integration Bottlenecks

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Solution Type

- 5.1.1 Tele-Healthcare

- 5.1.1.1 Telemedicine

- 5.1.1.2 Virtual Urgent Care

- 5.1.1.3 Virtual Primary Care

- 5.1.1.4 Virtual Specialty Care

- 5.1.1.5 Virtual Behavioral Health

- 5.1.2 mhealth

- 5.1.2.1 Wearables and Connected Medical Devices

- 5.1.2.2 Mobile Health Applications

- 5.1.2.3 Medication Adherence and Care-Navigation Apps

- 5.1.3 Digital Health Systems

- 5.1.3.1 EHR / EMR Platforms

- 5.1.3.2 E-Prescribing Systems

- 5.1.3.3 Health Information Exchange

- 5.1.3.4 Patient Portals and Personal Health Records

- 5.1.4 Healthcare Analytics and Clinical AI

- 5.1.4.1 Clinical Decision Support

- 5.1.4.2 Population Health and Risk Analytics

- 5.1.4.3 Revenue Cycle and Administrative AI

- 5.1.4.4 Ambient Documentation and Coding AI

- 5.1.5 Digital Therapeutics

- 5.1.5.1 Mental and Behavioral Health Therapeutics

- 5.1.5.2 ADHD and Neurobehavioral Therapeutics

- 5.1.5.3 Sleep and Insomnia Therapeutics

- 5.1.5.4 Metabolic And Lifestyle Therapeutics

- 5.1.1 Tele-Healthcare

- 5.2 By Component

- 5.2.1 Software

- 5.2.1.1 Clinical Platforms

- 5.2.1.2 Patient Engagement Software

- 5.2.1.3 Analytics and AI Software

- 5.2.2 Hardware

- 5.2.2.1 Wearables

- 5.2.2.2 Connected Monitoring Devices

- 5.2.2.3 Edge Devices and Gateways

- 5.2.3 Services

- 5.2.3.1 Implementation And Integration

- 5.2.3.2 Managed Clinical Services

- 5.2.3.3 Support And Optimization Services

- 5.2.1 Software

- 5.3 By Application

- 5.3.1 Diabetes Management

- 5.3.2 Cardiometabolic and Obesity Management

- 5.3.3 Cardiovascular Monitoring and Management

- 5.3.4 Mental and Behavioral Health Management

- 5.3.5 Respiratory Care Management

- 5.3.6 Preventive Wellness and Fitness

- 5.3.7 Women's Health

- 5.3.8 Medication Management and Adherence

- 5.4 By End User

- 5.4.1 Healthcare Providers

- 5.4.2 Payers

- 5.4.3 Patients and Consumers

- 5.4.4 Employers and Plan Sponsors

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 American Well Corporation

- 6.3.2 Amazon One Medical

- 6.3.3 athenahealth

- 6.3.4 Dexcom

- 6.3.5 Doximity

- 6.3.6 Epic Systems Corporation

- 6.3.7 Headspace Health

- 6.3.8 HealthTap

- 6.3.9 Hims & Hers Health

- 6.3.10 Hinge Health

- 6.3.11 Included Health

- 6.3.12 MDLIVE

- 6.3.13 Medtronic

- 6.3.14 Omada Health

- 6.3.15 Oracle Health

- 6.3.16 Talkspace

- 6.3.17 Teladoc Health

- 6.3.18 Veradigm

- 6.3.19 Virta Health

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment