PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065612

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065612

Wireless Power Transmission - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

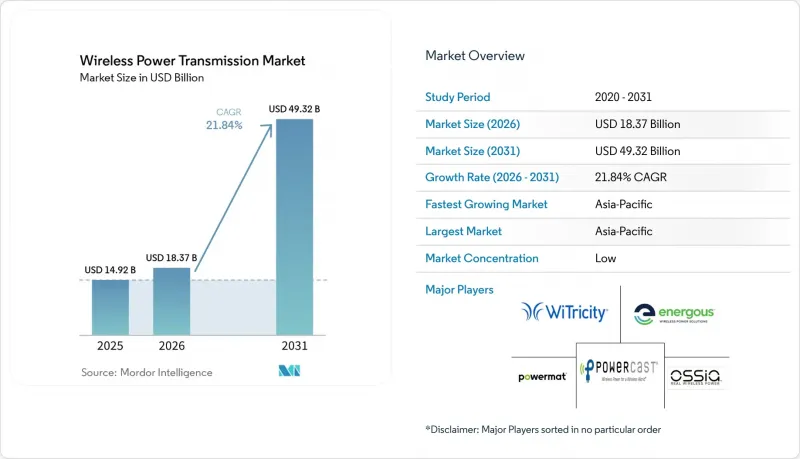

According to Mordor Intelligence, the wireless power transmission market size was valued at USD 14.92 billion in 2025 and estimated to grow from USD 18.37 billion in 2026 to reach USD 49.32 billion by 2031, at a CAGR of 21.84% during the forecast period (2026-2031).

This report is Segmented by Technology (Inductive Coupling, and More), Transmission Range (Short Range, Medium Range, and Long Range), Application (Smartphones and Tablets, Wearable Electronics, and More), Component (Transmitters, Receivers, Power Management and Control ICs, Magnetic Materials and Shielding, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Wireless Power Transmission Market Trends and Insights

Expanding Wireless Charging Adoption in Smartphones and Wearables

The wireless power transmission market is gaining direct support from faster wireless charging in mainstream smartphones and wearables. Qi2 v2.2.1 raised charging capability to 25 W in July 2025, narrowing the gap with wired fast charging and removing a major purchase barrier for many buyers. The same update strengthened the case for magnetic alignment by improving performance while keeping interoperability at the center of the consumer charging tier. The Wireless Power Consortium also said 1.5 billion Qi2-capable devices entered circulation within the standard's first year, which shows how quickly the installed base expanded. The wireless power transmission market also benefits from the accessory effect, because consumers who buy magnetic chargers, wallets, stands, and battery packs are more likely to stay inside the same compatibility path when replacing handsets.

Accelerating Wireless EV Charging Deployment and Fleet Electrification

The wireless power transmission market is also being boosted by the transition from EV pilots to visible commercial deployment. Electreon activated the A10 project in France in October 2025 and demonstrated 300 kW of inductive power under live traffic conditions, providing road operators and vehicle makers with a real infrastructure reference point rather than a laboratory result. In March 2026, Electreon completed its acquisition of InductEV and brought together dynamic and stationary charging intellectual property under a single company, with roughly 400 combined patents. Purdue University also demonstrated 190 kW charging of a Class 8 truck at 65 mph in December 2025 on a public U.S. test segment, which showed that heavy-duty use cases are moving into serious validation. The wireless power transmission market gains further momentum because depot operators can reduce plug handling, labor time, and connector wear in high-cycle logistics environments even before comparing energy transfer costs.

Efficiency Losses from Coil Misalignment and Thermal Load

The wireless power transmission market still faces a practical efficiency problem when real-world alignment differs from ideal test conditions. IEEE ISSCC research published in February 2025 showed 60.2% end-to-end efficiency for an enhanced frequency-splitting architecture in miniaturized wireless power delivery, which is meaningful progress but still well below optimized wired charging performance at similar power levels. Heat concentration at the receiver side adds another layer of difficulty, especially in consumer devices above 15 W, where thermal limits can trigger power reduction. In automotive deployments, higher-power systems also need cooling and control infrastructure that offsets part of the simplicity argument usually made for wireless charging. Electreon and Infineon highlighted this high-power challenge in December 2025 when they demonstrated 300 kW inductive charging using silicon carbide devices, because thermal management remained central to achieving that power density.

Other drivers and restraints analyzed in the detailed report include:

- Growing Wireless Power Use In Factory Automation and Mobile Robotics

- Rising Qi2 Ecosystem Standardization and Magnetic Accessory Integration

- High System and Infrastructure Cost Premiums Versus Wired Charging

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Inductive coupling accounted for 42.61% of revenue in 2025, making it the largest technology block in the wireless power transmission market, as Qi-certified consumer hardware already had a deep global supply chain. That leadership came from compatibility, production scale, and a large installed base of chargers and receiving devices. The wireless power transmission industry still relies heavily on inductive coupling in phones, tablets, and many everyday accessories because it is well established and understood. Even so, the short transfer distance and tighter alignment requirements limit its suitability for applications where users cannot position equipment with high precision. The wireless power transmission market is now seeing resonant inductive coupling gain ground because it tolerates greater coil offset and supports higher power transfer across wider gaps. Resonant inductive coupling is projected to grow at a 22.84% CAGR through 2031, making it the fastest-growing technology path in the wireless power transmission market. Electreon's October 2025 A10 motorway deployment provided a commercial proof point for this architecture at 300 kW peak power under live traffic conditions. Product qualification also continues to favor solutions with clearer compliance history under IEC 63028 and SAE J2954 frameworks.

Capacitive coupling remains a narrower option in sealed, non-ferrous, and specialized environments where magnetic field considerations matter more than raw power throughput. The wireless power transmission market includes radio frequency and microwave transmission in battery-free sensing and ambient IoT use cases, where far-field harvesting matters more than charger-pad alignment. Powercast remains a visible reference in this part of the wireless power transmission market because its patent depth and sensor deployments show that niche commercial demand already exists. Laser and infrared transmission is still the earliest commercial category, focused on long-distance or line-of-sight settings rather than broad installed-base adoption. IEEE ISSCC work on miniaturized resonant systems also matters because it gives device makers a benchmark for compact implantable and wearable designs. As a result, the technology mix in the wireless power transmission market is widening even while inductive and resonant systems remain the main revenue engines. That spread matters because it creates separate supply chains, design rules, and qualification paths inside the same wireless power transmission market. The wireless power transmission market size for inductive platforms remained the largest in 2025, but the growth curve is shifting toward resonant architectures in higher-power and less precisely aligned environments.

Short-range systems accounted for 55.39% of the wireless power transmission market size in 2025, reflecting the maturity of smartphone and wearable charging ecosystems built around Qi and Qi2. This range remained dominant because millions of users already use short-distance charging pads at home, at work, and in public settings. The wireless power transmission market still depends on this installed base for volume, component scale, and supplier learning effects. Even so, short-term share concentration is expected to ease through 2031 as faster growth now comes from systems serving vehicles, factory equipment, and more distributed wireless energy use cases. Long-range is projected to expand at a 22.39% CAGR through 2031, making it the fastest-growing transmission category in the wireless power transmission market. That growth is tied to dynamic vehicle charging, ambient RF harvesting, and directed energy concepts that sit outside the traditional ferrite-pad ecosystem. Medium-range systems, usually spanning 10 cm to 1 m, are also finding space in industrial robotics and furniture charging because they offer greater tolerance without requiring fully long-range architectures. Companies such as GuRu Wireless and Ossia are pushing room-scale delivery concepts, which show how the transmission-range landscape is broadening beyond simple pad-based charging.

The supply chain picture changes meaningfully as transmission distance increases. Short-range products draw on ferrites, coils, shielding, and receiver ICs, while long-range systems require a different stack that includes antenna arrays, beam steering, and higher-value RF electronics. The wireless power transmission market, therefore, creates white space for specialists who were never strong in phone charging components. This difference means cost leadership in short-range hardware does not automatically translate into leadership in long-range wireless power. It also changes the buyer set, because infrastructure planners, logistics operators, and enterprise IoT integrators evaluate these systems with different return thresholds than consumer device makers. The wireless power transmission market will likely see clearer separation between short-range incumbents and long-range specialists as road and ambient power projects produce more field data. That separation matters because it reduces the risk that a single product architecture dominates every use case. The wireless power transmission industry is increasingly split by range logic, not just by end-use sector. Short range remains the anchor, but long-range opportunity is where much of the next competitive repositioning in the wireless power transmission market is taking shape.

Geography Analysis

Asia-Pacific held 36.78% of the wireless power transmission market share in 2025 and is projected to expand at a 22.81% CAGR through 2031. The region led the wireless power transmission market because it combined dense smartphone demand, deep electronics manufacturing, and rising automation investment within the same geographic base. China remained central to the regional supply chain because it supports large-scale production of ferrites, Litz wire, receiver ICs, and device assembly for the wireless power transmission market. South Korea also strengthened its position in 2025 through expanded wireless power certification for commercial and industrial robots and through Qi v2.2.1 certification activity that reinforced its role as a compliance hub for consumer devices.

North America and Europe formed the second-largest geographic cluster in the wireless power transmission market and remained the most active regions for dynamic EV charging projects. The United States was the leading North American market because it combined high smartphone wireless charging penetration with rising interest in EV fleets and visible infrastructure testing. Purdue University's December 2025 heavy-duty truck demonstration gave the region a strong public benchmark for in-motion charging at highway speeds. The FCC's January 2026 geofenced 6 GHz variable-power device rules also helped define a more workable path for higher-power ambient wireless devices, which matters for enterprise and industrial use cases in the wireless power transmission market. Europe remained the most advanced region for road electrification in the wireless power transmission market, led by France and Italy. Electreon's A10 motorway deployment in France validated 300 kW peak dynamic charging under real traffic conditions in October 2025. Iveco's March 2026 announcement of the eDaily on Italy's A35 motorway then showed that vehicle-side integration was moving closer to commercial use. Together, these developments showed that European road operators and OEMs are treating dynamic wireless charging as near-term infrastructure rather than a distant concept.

South America, the Middle East, and Africa remained early-stage markets for wireless power transmission through 2026. Brazil and Argentina continued to present the clearest South American opportunities, though adoption still leaned toward consumer device charging rather than advanced EV or industrial systems. The Middle East is emerging as a selective investment destination in the wireless power transmission market, especially where mobility programs are linked to wider decarbonization and smart-city targets. Beam Global and HEVO launched an autonomous, wireless EV charging platform in February 2026 for operators in the United States and the UAE, demonstrating that the Gulf is attracting advanced mobility solutions earlier than many other emerging regions. Africa remained at an early adoption stage, with consumer electronics as the main entry point, while broader EV and industrial deployment still face infrastructure gaps and import pressures. Even so, the wireless power transmission market is likely to expand its geographic reach over 2026-2031 as lower-power consumer applications gain familiarity before higher-value automotive and automation projects follow.

- WiTricity Corporation

- Energous Corporation

- Ossia Inc.

- Powercast Corporation

- Powermat Technologies Ltd.

- Wi-Charge Ltd.

- NuCurrent, Inc.

- ConvenientPower HK Limited

- Mojo Mobility, Inc.

- GuRu Wireless, Inc.

- Electreon Wireless Ltd.

- HEVO Inc.

- Evatran, LLC

- Resonant Link Medical, LLC

- PowerLight Technologies, Inc.

- Emrod Limited

- Aeterlink Corporation

- Solace Power Inc.

- Reach Power Inc.

- Etherdyne Technologies, Inc.

- Yank Technologies, Inc.

- Aira, Inc.

- Aircharge Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Wireless Charging Adoption in Smartphones and Wearables

- 4.2.2 Accelerating Wireless EV Charging Deployment and Fleet Electrification

- 4.2.3 Growing Wireless Power Use in Factory Automation and Mobile Robotics

- 4.2.4 Increasing Adoption of Wireless Power in Sealed and Implantable Medical Devices

- 4.2.5 Rising Qi2 Ecosystem Standardization and Magnetic Accessory Integration

- 4.2.6 Scaling Battery-Free Retail and Logistics IoT Networks

- 4.3 Market Restraints

- 4.3.1 Efficiency Losses From Coil Misalignment and Thermal Load

- 4.3.2 High System and Infrastructure Cost Premiums Versus Wired Charging

- 4.3.3 Fragmented RF Exposure and EMC Compliance Regimes

- 4.3.4 Concentrated Supply of Ferrites and Litz Wire Components

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Inductive Coupling

- 5.1.2 Resonant Inductive Coupling

- 5.1.3 Capacitive Coupling

- 5.1.4 Radio Frequency and Microwave Power Transmission

- 5.1.5 Laser and Infrared Power Transmission

- 5.2 By Transmission Range

- 5.2.1 Short Range

- 5.2.2 Medium Range

- 5.2.3 Long Range

- 5.3 By Application

- 5.3.1 Smartphones and Tablets

- 5.3.2 Wearable Electronics

- 5.3.3 Electric Vehicle Charging

- 5.3.4 Industrial Equipment and Robotics

- 5.3.5 Medical Devices

- 5.3.6 Public Infrastructure and Furniture

- 5.4 By Component

- 5.4.1 Transmitters

- 5.4.2 Receivers

- 5.4.3 Power Management and Control ICs

- 5.4.4 Magnetic Materials and Shielding

- 5.4.5 Software and System Controllers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 WiTricity Corporation

- 6.4.2 Energous Corporation

- 6.4.3 Ossia Inc.

- 6.4.4 Powercast Corporation

- 6.4.5 Powermat Technologies Ltd.

- 6.4.6 Wi-Charge Ltd.

- 6.4.7 NuCurrent, Inc.

- 6.4.8 ConvenientPower HK Limited

- 6.4.9 Mojo Mobility, Inc.

- 6.4.10 GuRu Wireless, Inc.

- 6.4.11 Electreon Wireless Ltd.

- 6.4.12 HEVO Inc.

- 6.4.13 Evatran, LLC

- 6.4.14 Resonant Link Medical, LLC

- 6.4.15 PowerLight Technologies, Inc.

- 6.4.16 Emrod Limited

- 6.4.17 Aeterlink Corporation

- 6.4.18 Solace Power Inc.

- 6.4.19 Reach Power Inc.

- 6.4.20 Etherdyne Technologies, Inc.

- 6.4.21 Yank Technologies, Inc.

- 6.4.22 Aira, Inc.

- 6.4.23 Aircharge Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment