PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065733

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065733

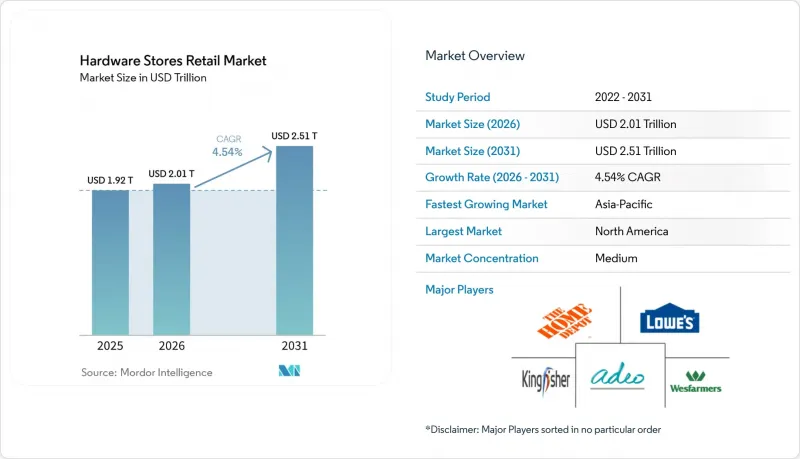

Hardware Stores Retail - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the hardware stores retail market size is projected to be USD 1.92 trillion in 2025, USD 2.01 trillion in 2026, and reach USD 2.51 trillion by 2031, growing at a CAGR of 4.54% from 2026 to 2031.

This report is Segmented by Product Category (Tools & Hardware, Building Materials, Plumbing & Electrical, Paint & Adhesives, and More), by Customer Type (DIY, Professional Contractors, Institutional & MRO), by Store Format (Big-Box, Traditional Hardware, and More), and by Geography (North America, South America, Europe, Asia-Pacific, and MEA). The Market Forecasts are Provided in Terms of Value (USD).

Global Hardware Stores Retail Market Trends and Insights

Rising Renovation Over Relocation Trend

The renovation-over-relocation pattern remains the clearest demand base for the hardware retail market in 2026. U.S. existing home sales were running at a 3.91 million annual rate in January 2026, while single-family permits fell to a seven-year low in 2025, prompting more households to improve their current homes rather than move. HIRI reported that professional market sales are projected to grow faster than consumer market sales in 2025, pointing to larger and more technical projects moving toward skilled execution. This mix is lifting average ticket values in the hardware retail market, even when store visit frequency becomes less predictable. Retailers with deeper project assortments, stronger installed-sales links, and contractor-ready inventory are better placed to capture spending. At the same time, the housing lock-in effect stays in place through the forecast period.

Social Media Driven DIY Learning Adoption

Social media is lowering the confidence barrier to first-time project work, giving the hardware retail market a wider entry funnel for smaller repair and improvement jobs. Short-form project demonstrations are helping consumers understand tool selection, material needs, and sequencing before they visit a store or place an online order. That behavior matters most in categories such as paint, adhesives, storage, garden products, and entry-level tools, where product discovery often starts with simple project ideas rather than planned replacement cycles. The hardware retail market is therefore benefiting from a broader set of inspiration-led purchases that can be converted through search, digital merchandising, and same-day pickup. The effect is strongest in the short term because it encourages participation and product trial, even if more advanced work still shifts toward professional execution.

Shift From DIY to DIFM Services

The shift from do-it-yourself to do-it-for-me activity is narrowing the direct consumer opportunity in parts of the hardware retail market. HIRI reported that professional market sales are projected to grow faster than consumer market sales in 2025, which shows that more project volume is moving toward skilled execution. Wickes also reported that TradePro membership reached 643,000 in FY2025, up 10.7% from 581,000 in 2024, highlighting retailers' efforts to retain this spend through trade-focused loyalty systems. For the hardware retail market, the issue is less about demand disappearance and more about who controls procurement at the point of sale. Retailers that fail to serve both consumer and contractor missions in the same ecosystem risk losing volume to trade distributors and specialist merchant channels.

Other drivers and restraints analyzed in the detailed report include:

- Growing Omnichannel Click-and-Collect Demand

- Increasing Energy Efficiency Retrofit Upgrades

- Housing Affordability Limiting Projects

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Building Materials accounted for 28.73% of the total value in 2025, making it the largest product segment in the hardware retail market. Its scale is tied to steady renovation demand for sheathing, insulation, framing lumber, and roofing products, especially when households choose to improve existing homes rather than relocate. This category continues to benefit from repair, rehabilitation, and structural retrofit work in aging housing markets, where project depth matters more than new-home turnover. Plumbing & Electrical is projected to grow at a 5.46% CAGR through 2031, making it the fastest-growing product line in the hardware retail market under the current forecast. That trajectory reflects stronger demand for electrical panels, wiring, controls, and heat pump components as electrification programs and efficiency upgrades expand.

The product mix shift matters because the hardware retail industry is no longer driven only by low-ticket tools and routine consumables. Plumbing & Electrical is gaining strategic weight as a higher-value category with more configuration needs, better attachment opportunities, and stronger links to licensed installation work. Building Materials still anchors volume because it captures both essential repair spend and structural renovation outlays, which gives it a broad role across consumer and contractor demand. The NHPA's 2026 survey found that 48% of hardware retailers were investing in paint and sundries, while 43% were investing in lawn and garden, which shows that merchants are actively widening category balance around the traditional core. Paint, adhesives, outdoor products, and premium kitchen and bath lines remain important because they support repeat purchases, seasonal traffic, and margin expansion even as large project work becomes more selective.

Geography Analysis

North America accounted for 37.95% of the global value in 2025, making it the largest regional market in hardware retail. The region benefits from a large home-improvement base, widespread organized retail networks, and a durable culture of household investment in repair and renovation. HIRI reported that single-family permits fell to 909,600 in 2025, yet nearly 80% of U.S. homeowners were still planning maintenance or improvement work in Q1 2026, which shows why renovation demand remains the main support line. North America also remains the main test bed for omnichannel execution, contractor account development, and digitally supported fulfillment models. State-level electrification rebates and wildfire-hardening requirements add another layer of local demand variation, which makes regional inventory planning more important across the hardware retail market.

Asia-Pacific is projected to grow at a 5.69% CAGR through 2031, which makes it the fastest-expanding geography in the hardware retail market. Growth is being supported by rapid urbanization, rising homeownership, and the continued development of organized hardware retail structures in India and Southeast Asia. The opportunity is especially notable in markets where fragmented local trade still dominates procurement and modern chain penetration remains limited. That underpenetration gives large-format chains, local networks, and hybrid retail models room to expand store count, service coverage, and category sophistication over time. In more mature parts of the region, energy-efficiency upgrades, smart-home integration, and aging-home renovation offer a different growth path, less dependent on network expansion and more on product mix.

Europe sits between mature demand conditions and uneven country-level performance in the hardware retail market. The region shows that the same macro pressure does not yield identical outcomes because housing policy, consumer sentiment, and channel structure differ widely across countries. Store-based players in Europe are under pressure to improve digital access, pickup speed, and trade-customer service as project demand becomes more selective and online research becomes more important. South America, the Middle East, and Africa remain smaller in absolute terms, but they still offer incremental demand through urban development, repair activity, and the gradual formalization of hardware buying. Across all these regions, the hardware retail market is being shaped by the balance between local store density, renovation demand, and the pace at which organized retail can improve convenience and product access.

- The Home Depot, Inc.

- Lowe's Companies, Inc.

- Ace Hardware Corporation

- Menard, Inc.

- Do it Best Group

- True Value Company

- Wesfarmers Limited (Bunnings Group)

- ADEO

- Kingfisher plc

- OBI Group Holding SE & Co. KGaA

- HORNBACH Holding AG & Co. KGaA

- BAUHAUS AG

- hagebau Handelsgesellschaft fur Baustoffe mbH & Co. KG

- Travis Perkins plc

- Wickes Group plc

- Grafton Group plc

- Kesko Corporation

- Mr. D.I.Y. Group (M) Berhad

- Canadian Tire Corporation, Limited

- Metcash Limited (Mitre 10 / Total Tools)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.1.1 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising renovation over relocation trend

- 4.2.2 Social media driven DIY learning adoption

- 4.2.3 Growing omnichannel click-and-collect demand

- 4.2.4 Increasing energy efficiency retrofit upgrades

- 4.2.5 Expansion of state rebate electrification programs

- 4.2.6 Rising wildfire hardening retrofit initiatives

- 4.3 Market Restraints

- 4.3.1 Shift from DIY to DIFM services

- 4.3.2 Housing affordability limiting projects

- 4.3.3 Rising organized retail crime incidents

- 4.3.4 Policy volatility in rebates and tariffs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Category

- 5.1.1 Tools & Hardware

- 5.1.2 Building Materials

- 5.1.3 Plumbing & Electrical

- 5.1.4 Paint, Adhesives & Home Improvement Consumables

- 5.1.5 Outdoor & Garden

- 5.1.6 Kitchen, Bath & Storage

- 5.2 By Customer Type

- 5.2.1 DIY Consumers

- 5.2.2 Professional Contractors & Tradespeople

- 5.2.3 Institutional & MRO Buyers

- 5.3 By Store Format

- 5.3.1 Big-Box Home Centers

- 5.3.2 Traditional Hardware Stores

- 5.3.3 Lumber & Building Material Yards

- 5.3.4 Farm & Ranch Supply Stores

- 5.3.5 Online-Only Platforms

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Peru

- 5.4.2.3 Chile

- 5.4.2.4 Argentina

- 5.4.2.5 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.4.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.4.3.8 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 India

- 5.4.4.2 China

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 South Korea

- 5.4.4.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East And Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East And Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 The Home Depot, Inc.

- 6.4.2 Lowe's Companies, Inc.

- 6.4.3 Ace Hardware Corporation

- 6.4.4 Menard, Inc.

- 6.4.5 Do it Best Group

- 6.4.6 True Value Company

- 6.4.7 Wesfarmers Limited (Bunnings Group)

- 6.4.8 ADEO

- 6.4.9 Kingfisher plc

- 6.4.10 OBI Group Holding SE & Co. KGaA

- 6.4.11 HORNBACH Holding AG & Co. KGaA

- 6.4.12 BAUHAUS AG

- 6.4.13 hagebau Handelsgesellschaft fur Baustoffe mbH & Co. KG

- 6.4.14 Travis Perkins plc

- 6.4.15 Wickes Group plc

- 6.4.16 Grafton Group plc

- 6.4.17 Kesko Corporation

- 6.4.18 Mr. D.I.Y. Group (M) Berhad

- 6.4.19 Canadian Tire Corporation, Limited

- 6.4.20 Metcash Limited (Mitre 10 / Total Tools)

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment

- 7.2 Expansion of Smart Home and Energy-Efficient Retrofit Products

- 7.3 Growth of Pro-Contractor Loyalty and Omnichannel Retail Platforms