PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065775

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065775

Network Function Virtualization (NFV) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

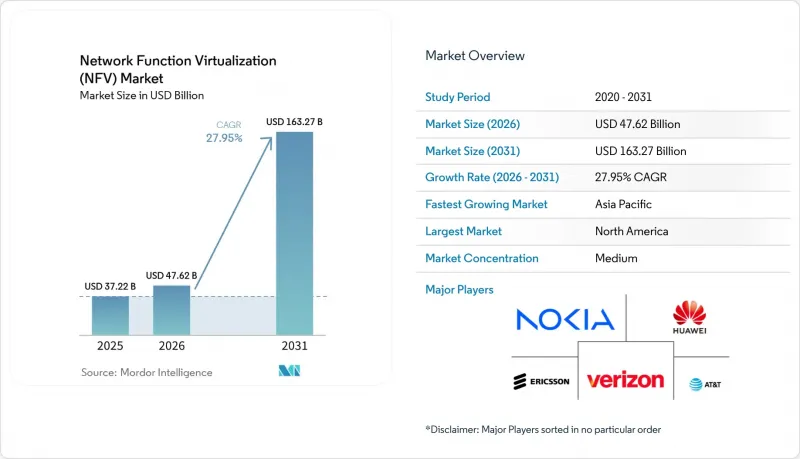

According to Mordor Intelligence, the network function virtualization market size is expected to grow from USD 37.22 billion in 2025 to USD 47.62 billion in 2026 and is forecast to reach USD 163.27 billion by 2031 at 27.95% CAGR over 2026-2031.

This report is Segmented by Component (Hardware, Software, and More), Application (Virtual Appliances, Core Network Virtualization, and More), End User (Telecom Service Providers, Enterprise, and More), Deployment Mode (On-Premise, Public Cloud, and More), Virtualized Network Function (Compute, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Network Function Virtualization (NFV) Market Trends and Insights

Rising demand for 5G and network slicing

Network slicing lets operators create multiple isolated virtual networks on common infrastructure, each optimized for specific performance targets. By pairing software-defined networking with NFV, carriers dynamically allocate compute, storage, and transport resources to run new services in minutes rather than months. Early commercial slices span autonomous vehicle telemetry, robotic process automation, and smart-city sensor backhaul. The model supports differentiated pricing linked to latency or reliability, repositioning operators from bandwidth resellers to service enablers.

Telco CAPEX-to-OPEX shift via cloud-native NFV infrastructure

Containerized network functions and microservices allow operators to decompose monolithic network elements, spin them up rapidly, and pay only for the resources consumed. Dish's public commitment to spend USD 10 billion on an all-cloud 5G network showcases the financial appeal of shifting fixed hardware cycles toward elastic software lifecycles. Cost savings emerge not merely from cheaper hardware but from zero-touch provisioning and automated life-cycle management that cut field-engineering visits and manual configuration errors.

Open-Source ecosystems lowering vendor lock-in

The O-RAN specification disaggregates radio access networks into interoperable components, while ONAP delivers an open-source platform for end-to-end service orchestration. Carriers using open interfaces reduce single-vendor dependence and accelerate multivendor innovation cycles. Europe's regulatory agenda actively promotes open architectures to strengthen digital sovereignty and curb concentration risk.

Other drivers and restraints analyzed in the detailed report include:

- Edge-cloud deployments for URLLC and mMTC use-cases

- AI-Driven MANO and service assurance

- Private-5G adoption in Industry 4.0 driving on-prem NFV

- Integration with legacy OSS/BSS stacks

- Multi-vendor VNF interoperability gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware still underpins 64.30% of the 2025 network function virtualization market size because carrier-grade compute and acceleration cards guarantee predictable throughput during early 5G traffic spikes. Yet software revenues, propelled by container network functions and AI orchestration suites, are set to grow at 29.2% CAGR through 2031. A surge in hyper-converged edge platforms illustrates how operators bundle compute, storage, and switching in a single appliance optimized for cloud-native packets.

Software's momentum is reinforced by open-source ecosystems that shorten development cycles and encourage community-driven innovation. As operators adopt GitOps and CI/CD pipelines, release cadences mirror cloud disciplines rather than hardware refresh timelines. This transition displaces bespoke appliances with programmable services deployable in minutes, reshaping vendor economics across the network function virtualization market.

In 2025 virtual appliances-firewalls, vCPE, and vRAN-occupied 44.65% share of the network function virtualization market size. Orchestration and automation, however, will outpace all other categories at a 28.2% CAGR because service agility depends on intent-driven provisioning engines that coordinate thousands of distributed VNFs. Operators view automated closed-loop control as indispensable to monetizing network slices and maintaining quality of service amid exponential traffic growth.

Containerization is catalyzing application diversity. Edge Kubernetes clusters now host lightweight UPFs and user plane accelerators, enabling industrial IoT and immersive media workloads. Vendors integrate analytics and policy enforcement directly inside orchestrators, collapsing traditional boundaries between assurance and control domains. These innovations keep the network function virtualization market firmly on a software-first trajectory.

Geography Analysis

North America's 37.60% network function virtualization market share in 2025 stems from early virtualization initiatives by operators such as AT&T and the United States' strategic push for secure, domestic 5G infrastructure leadership. Federal incentives for open-RAN research, coupled with ample capital access, accelerate commercial deployments. Canadian carriers follow similar trajectories, modernizing packet cores to increase agility and satisfy aggressive service-quality mandates.

Europe registers steady adoption as regulators prioritize digital sovereignty, sustainability, and competition. BEREC's cloud-edge framework encourages open interfaces and federated cloud models that align naturally with NFV. Operators like Deutsche Telekom and Telefonica pilot AI-native orchestration and GitOps pipelines, demonstrating potential 5% greenhouse-gas reductions from dynamic workload consolidation. Fragmented national rules, however, prolong cross-border harmonization.

Asia-Pacific's 29.3% CAGR makes it the powerhouse of future growth. China's sweeping 5G rollout embeds virtualization from the radio to the core, while India's modernization drive embraces software-defined architectures to meet exploding mobile-data demand. Japan and South Korea already run private 5G-enabled factories, validating low-latency edge clouds. Emerging ASEAN economies, unencumbered by legacy networks, jump straight to cloud-native deployments, broadening supplier opportunities across the network function virtualization market.

- Cisco Systems Inc.

- Huawei Technologies Co. Ltd.

- Ericsson AB

- Nokia Corp.

- VMware Inc.

- Juniper Networks Inc.

- Hewlett Packard Enterprise (HPE)

- Dell Technologies Inc.

- Intel Corp.

- ATandT Inc.

- Verizon Communications Inc.

- ZTE Corp.

- Ribbon Communications

- NEC Corp.

- IBM Corp.

- Samsung Electronics

- Radisys Corp.

- Affirmed Networks (Microsoft)

- Mavenir Systems

- F5 Networks

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for 5G and network slicing

- 4.2.2 Telco CAPEX-to-OPEX shift via cloud-native NFV Infrastructure

- 4.2.3 Edge-cloud deployments for URLLC and mMTC use-cases

- 4.2.4 AI-driven MANO and service assurance

- 4.2.5 Open-source ecosystems (O-RAN, ONAP) lowering vendor lock-in

- 4.2.6 Private-5G adoption in Industry 4.0 driving on-prem NFV

- 4.3 Market Restraints

- 4.3.1 Integration with legacy OSS/BSS stacks

- 4.3.2 Multi-vendor VNF interoperability gaps

- 4.3.3 Telco skill-set shortage for cloud-native operations

- 4.3.4 Security and compliance risks in disaggregated supply chain

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Industry Ecosystem and Partnerships

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Application

- 5.2.1 Virtual Appliances (vCPE, vFW, vRAN)

- 5.2.2 Core Network Virtualization (vEPC, vIMS, vSR)

- 5.2.3 Orchestration and Automation

- 5.3 By End User

- 5.3.1 Telecom Service Providers

- 5.3.2 Cloud Service Providers

- 5.3.3 Enterprises

- 5.3.3.1 Banking, Financial Services, and Insurance (BFSI)

- 5.3.3.2 Retail and e-Commerce

- 5.3.3.3 Healthcare and Life Sciences

- 5.3.3.4 Manufacturing and Industrial

- 5.3.3.5 Government and Defense

- 5.4 By Deployment Mode

- 5.4.1 On-premise

- 5.4.2 Public Cloud

- 5.4.3 Hybrid / Multi-cloud

- 5.5 By Virtualized Network Function

- 5.5.1 Compute (vRouter, vSwitch)

- 5.5.2 Storage

- 5.5.3 Network (vLoad Balancer, vSR)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cisco Systems Inc.

- 6.4.2 Huawei Technologies Co. Ltd.

- 6.4.3 Ericsson AB

- 6.4.4 Nokia Corp.

- 6.4.5 VMware Inc.

- 6.4.6 Juniper Networks Inc.

- 6.4.7 Hewlett Packard Enterprise (HPE)

- 6.4.8 Dell Technologies Inc.

- 6.4.9 Intel Corp.

- 6.4.10 ATandT Inc.

- 6.4.11 Verizon Communications Inc.

- 6.4.12 ZTE Corp.

- 6.4.13 Ribbon Communications

- 6.4.14 NEC Corp.

- 6.4.15 IBM Corp.

- 6.4.16 Samsung Electronics

- 6.4.17 Radisys Corp.

- 6.4.18 Affirmed Networks (Microsoft)

- 6.4.19 Mavenir Systems

- 6.4.20 F5 Networks

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet Need Analysis