PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066426

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066426

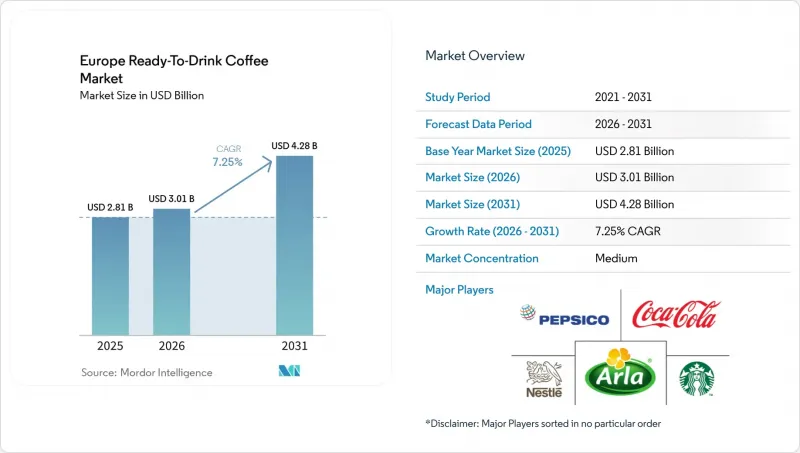

Europe Ready-To-Drink Coffee - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the europe ready-To-Drink coffee market size is expected to grow from USD 2.81 billion in 2025 to USD 3.01 billion in 2026 and is forecast to reach USD 4.28 billion by 2031 at 7.25% CAGR over 2026-2031.

This report is Segmented by Soft Drink Type (Cold Brew Coffee, Iced Coffee, and More), Packaging Type (PET Bottles, Glass Bottles, Metal Can, and More), Functionality (Protein-Enriched, Energy-Infused, and More), Distribution Channel (On-Trade and Off-Trade (Supermarket/Hypermarket, Convenience Stores, Specialty Stores, and More)), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe Ready-To-Drink Coffee Market Trends and Insights

On-the-go consumption trend among gen Z and millennials

Gen Z and Millennials, driven by fast-paced urban lifestyles and a preference for convenience, are fueling the European Ready-To-Drink (RTD) coffee market. These demographics view RTD coffee as a time-saving caffeine fix, with Gen Z favoring experimental, flavored, and iced varieties over traditional hot coffee. Government initiatives, such as Germany's focus on diabetes management, have increased demand for low-sugar products, prompting manufacturers to innovate with healthier formulations. In January 2024, Nestle's Nescafe launched plant-based RTD coffee in Europe, targeting health-conscious consumers. By July 2024, Starbucks introduced RTD protein coffee drinks in flavors like caffe latte and caramel hazelnut, appealing to young adults seeking functional benefits. In February 2025, Emmi released Caffe Latte Zero in the UK, a no-added-sugar line made using sustainable processes, aligning with Gen Z's eco-conscious values. Innovations like these, coupled with sustainable packaging such as recyclable aluminum cans, reinforce the on-the-go trend as a key growth driver for the European RTD coffee market.

Premiumization and cafe culture influence

In Europe, especially in Italy and Spain, consumers are increasingly associating coffee with artisanal quality and a narrative of origin. This trend is now making its way into ready-to-drink (RTD) formats. Italy, with its deep-rooted espresso culture, where most adults indulge in daily coffee rituals and cafe prices have steadily climbed over the past three years, has cultivated a consumer base willing to pay a premium for authenticity. Seizing this opportunity, brands are rolling out offerings like single-origin cold brews, nitro-infused lattes, and specialty blends, closely resembling those found in third-wave cafes. In 2024, JDE Peet's capitalized on this trend, launching 'L'OR Iced Coffee', banking on the premium equity of its L'OR brand to set higher shelf prices. This push for premiumisation isn't just limited to the product but extends to packaging as well. Glass bottles and aluminum cans, adorned with high-resolution prints, exude a sense of craft, while aseptic cartons, boasting 360-degree branding, tell a story on a larger canvas. However, the appetite for premium pricing isn't universal. While Spain showcases a 43% share for private labels, hinting at a price-sensitive market in southern Europe, urban millennials in cities like Milan, Madrid, and Paris are increasingly viewing RTD coffee as a palatable luxury.

Volatile coffee-bean prices squeezing manufacturer margins

In December 2024, Arabica prices soared to USD 3.44 per pound, marking an 80% year-over-year surge. This spike was largely attributed to frost damage in Brazil, drought conditions in Vietnam, and speculative trading activities. Robusta prices mirrored this trend, hitting record highs. This surge in prices intensified input-cost pressures for manufacturers who typically blend both Arabica and Robusta to achieve a desired flavor profile while managing costs. In its October 2025 update, JDE Peet's highlighted the challenges, noting that green-coffee prices are "significantly elevated and increasingly volatile." This volatility has compelled the company to adopt disciplined pricing and productivity measures to safeguard its adjusted EBIT. Meanwhile, Nestle's coffee category in Zone Europe implemented double-digit price increases in the first half of 2025 to counteract inflationary pressures. However, despite these hikes, the real internal growth remained stagnant, underscoring the sensitivity of volumes to price adjustments. Smaller coffee brands, lacking the hedging tools and purchasing clout of their multinational counterparts, find themselves at a disadvantage. They're more susceptible to margin squeezes or compelled retail price hikes, which can diminish their competitiveness against private-label options. Given the ongoing climate volatility, this cautious approach seems set to continue. The International Coffee Organization has even forecasted persistent supply deficits extending through 2026.

Other drivers and restraints analyzed in the detailed report include:

- Flavour and format innovation

- Expansion of supermarket private label RTD portfolios

- EU deforestation free traceability compliance costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, iced coffee captured 49.35% of the market, underscoring its widespread appeal and resonance with Europe's traditional preference for milk-forward, sweetened brews. Cold brew coffee, while a smaller player, is set to grow at an 7.82% CAGR through 2031, bolstered by its specialty positioning and the smoothness attributed to its low-acidity extraction. Nestle debuted Nescafe Iced Lattes in multi-serve cartons in March 2025, aiming squarely at the at-home consumption market. Meanwhile, Lavazza rolled out a trio of iced coffee cans in June 2024, featuring a protein variant to tap into the growing functional demand. Cold brew's premium pricing, typically 20% to 30% higher than iced coffee, finds favor with urban millennials, who are willing to pay a premium for its craft credentials and reduced bitterness. Grind, a specialty roaster from the UK, broadened its cold-brew concentrate line in 2024-2025, focusing on single-origin offerings for cafes and retail.

While other ready-to-drink (RTD) coffee formats like nitro coffee, espresso shots, and flavored lattes cater to niche occasions, they collectively command a significant market share. In 2025, Emmi introduced a 230 ml decaffeinated CAFFE LATTE and a 650 ml resealable "Mr. Huge" variant, catering to late-evening consumers and those seeking multi-serve convenience. JDE Peet's inaugurated a Modular Innovation Lab in Utrecht in October 2025, equipped with dedicated RTD cold-brew production capabilities, signaling a clear intent to fast-track format innovation. The market segmentation reveals a clear divide: while mass-market iced coffee drives volume, it's the cold brew and specialty formats that are fueling value and margin growth. Brands face the challenge of balancing their portfolios, offering entry-level iced lattes to entice trials, while also featuring premium cold-brew SKUs that command higher retail prices and fend off private-label competition.

In 2025, glass bottles commanded a 35.10% market share, lauded for their premium appeal, inert nature, and perceived quality. Meanwhile, PET bottles are set to expand at a 7.65% CAGR through 2031, driven by trends like lightweighting, recyclability mandates, and consumer convenience. European Union regulations are pushing for a 30% recycled PET content by 2030 and ramping up to 65% by 2040. This has led brands to swiftly adopt food-grade rPET. Notably, Coca-Cola European Partners reached an impressive 63.2% rPET usage in Europe in 2024. Reusable PET bottles, designed for 15 to 25 cycles, are gaining traction as a circular substitute to single-use glass, boasting advantages like reduced weight and diminished transport emissions. Metal cans, though holding a smaller market share, enjoy stability thanks to Europe's impressive recycling rates, surpassing 70%. Additionally, innovations like new water-based, BPA-free coatings, as highlighted by Canmakers UK, are alleviating food-safety concerns.

Aseptic packages, predominantly Tetra Pak and SIG cartons, are revolutionizing distribution. They allow for ambient storage and extended shelf life sans preservatives, a boon for convenience stores and vending machines. Tetra Pak's 2024 foray into paper-based barriers and certified recycled polymers underscores a commitment to circularity. Their push for 360-degree printability further elevates premium branding. However, disposable cups, a staple in on-trade settings, are grappling with regulatory challenges. The EU Packaging Regulation is steering the industry: it mandates that by 2030, 10% of on-premise consumption should utilize reusable packaging, escalating to 40% by 2040. This shift is nudging cafes and restaurants towards refillable systems. As the industry pivots, PET and aseptic formats emerge as frontrunners, striking a balance between sustainability, cost, and consumer convenience. Meanwhile, glass bottles carve out a niche, remaining the go-to for specialty items and gifting occasions.

List of Companies Covered in this Report:

- Nestle SA

- Starbucks Corp.

- PepsiCo Inc.

- The Coca-Cola Company

- Arla Foods amba

- Emmi AG

- Danone SA

- Luigi Lavazza S.p.A.

- Illycaffe S.p.A.

- Suntory Beverage & Food Ltd.

- Lotte Chilsung Beverage Co. Ltd.

- Keurig Dr Pepper Inc.

- Rauch Fruchtsafte GmbH & Co OG

- Sodiaal Union

- Califia Farms LLC

- Monster Beverage Corp.

- UCC Ueshima Coffee Co.

- Muller Group

- JAB Holding

- Dean Foods

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 On-the-go consumption trend among Gen Z and Millennials

- 4.2.2 Premiumisation and cafe-culture influence

- 4.2.3 Flavour and format innovation

- 4.2.4 Expansion of supermarket private-label RTD portfolios

- 4.2.5 Sustainability-driven switch to recyclable carton formats

- 4.2.6 EU deforestation-free sourcing rules spurring traceable offerings

- 4.3 Market Restraints

- 4.3.1 Volatile coffee-bean prices squeezing manufacturer margins

- 4.3.2 Intensifying private-label and discounter competition

- 4.3.3 EU deforestation-free traceability compliance costs

- 4.3.4 Limited aseptic-filling capacity for small entrants

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Soft Drink Type

- 5.1.1 Cold Brew Coffee

- 5.1.2 Iced Coffee

- 5.1.3 Other RTD Coffee

- 5.2 Packaging Type

- 5.2.1 PET Bottles

- 5.2.2 Glass Bottles

- 5.2.3 Metal Can

- 5.2.4 Aseptic packages

- 5.2.5 Disposable Cups

- 5.3 Functionality

- 5.3.1 Protein-Enriched

- 5.3.2 Energy-Infused

- 5.3.3 Others

- 5.4 Distribution Channel

- 5.4.1 On-Trade

- 5.4.2 Off-Trade

- 5.4.2.1 Supermarket/Hypermarket

- 5.4.2.2 Convenience Stores

- 5.4.2.3 Specialty Stores

- 5.4.2.4 Online Retail

- 5.4.2.5 Other Distribution Channels

- 5.5 Geography

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Netherlands

- 5.5.7 Poland

- 5.5.8 Belgium

- 5.5.9 Sweden

- 5.5.10 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 Nestle SA

- 6.4.2 Starbucks Corp.

- 6.4.3 PepsiCo Inc.

- 6.4.4 The Coca-Cola Company

- 6.4.5 Arla Foods amba

- 6.4.6 Emmi AG

- 6.4.7 Danone SA

- 6.4.8 Luigi Lavazza S.p.A.

- 6.4.9 Illycaffe S.p.A.

- 6.4.10 Suntory Beverage & Food Ltd.

- 6.4.11 Lotte Chilsung Beverage Co. Ltd.

- 6.4.12 Keurig Dr Pepper Inc.

- 6.4.13 Rauch Fruchtsafte GmbH & Co OG

- 6.4.14 Sodiaal Union

- 6.4.15 Califia Farms LLC

- 6.4.16 Monster Beverage Corp.

- 6.4.17 UCC Ueshima Coffee Co.

- 6.4.18 Muller Group

- 6.4.19 JAB Holding

- 6.4.20 Dean Foods

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK