PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066449

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066449

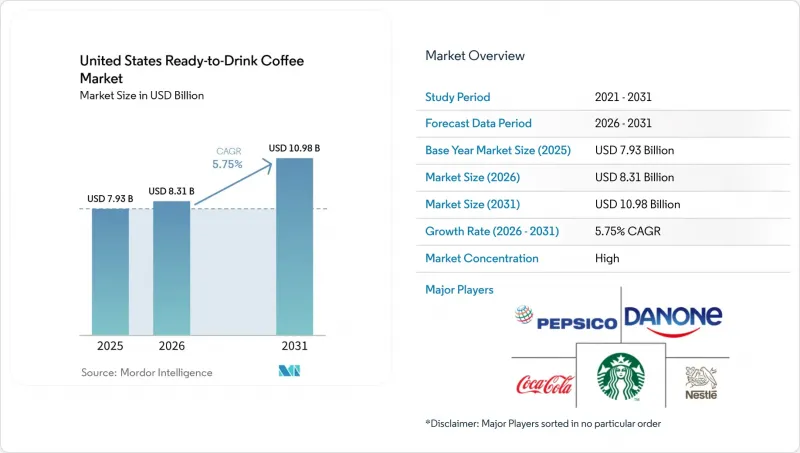

United States Ready-to-Drink Coffee - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states ready-to-drink Coffee Market size is expected to grow from USD 7.93 billion in 2025 to USD 8.31 billion in 2026 and is forecast to reach USD 10.98 billion by 2031 at 5.75% compound annual growth rate (CAGR) over 2026-2031.

This report is Segmented by Type (Cold Brew Coffee, Iced Coffee, and Other RTD Coffee), Packaging Type (PET Bottles, Glass Bottles, Metal Can, and More), Functionality (Protein-Enriched, Energy-Infused, and Other), and Distribution Channel (On-Trade, and Off-Trade). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

United States Ready-to-Drink Coffee Market Trends and Insights

Rising adoption of grab-and-go coffee culture among Gen Z and millennial consumers

Generation Z and millennial consumers together make up over 50% of ready-to-drink (RTD) coffee purchases, driven by lifestyle choices that prioritize convenience and portability over traditional cafe visits. The National Coffee Association's 2024 National Coffee Data Trends report highlighted that 63% of consumers aged 18 to 34 purchased RTD coffee at least once per week, reflecting a 12 percentage-point increase since 2020 . This shift is further influenced by urbanization and longer commute times, which compress morning routines and increase the demand for shelf-stable, single-serve options. Starbucks responded to this trend by partnering with Gopuff in 2024 to offer 15-minute delivery of its bottled Frappuccino and cold brew products across 650 U.S. cities, directly addressing the immediacy expectations of younger consumers. Furthermore, the grab-and-go segment benefits from social media exposure, as visually appealing packaging and limited-edition flavors encourage organic promotion through user-generated content on platforms such as Instagram and TikTok.

Increasing health consciousness and demand for low-sugar and functional RTD coffee

Health-conscious consumers are paying closer attention to ingredient labels, leading to significant reformulations in the ready-to-drink (RTD) coffee market. The United States Food and Drug Administration (FDA) updated its "healthy" claim criteria in December 2024, setting a limit on added sugars at 5% of the daily value per serving and requiring minimum contributions from food groups such as dairy or whole grains . Brands that meet these criteria can use the "healthy" descriptor on front-of-pack labeling, offering a competitive advantage in the crowded retail environment. For example, Danone's Silk NextMilk coffee creamers, introduced in 2024, align with this trend by reducing sugar content by 50% compared to traditional creamers while maintaining a creamy texture through proprietary plant-protein blends. Additionally, functional RTD coffee products are incorporating ingredients such as prebiotic fibers, medium-chain triglyceride (MCT) oil, and collagen peptides to cater to consumer preferences for gut health, ketogenic diets, and skin wellness. A study published in the Journal of Functional Foods in 2024 revealed that cold brew coffee fortified with inulin increased satiety scores by 18% compared to standard formulations, highlighting the potential of fiber-enriched RTD coffee as a meal-replacement option.

Stringent FDA regulations on functional beverage claims and health substantiation requirements

The United States Food and Drug Administration has increased its enforcement of structure-function claims and nutrient content descriptors since 2024. Manufacturers are now required to back health-related marketing claims with randomized controlled trials or epidemiological evidence. In 2024, the FDA issued 14 warning letters to beverage companies for making unsubstantiated claims about immune support, cognitive enhancement, and metabolic health. The cost of compliance for clinical validation can exceed USD 500,000 per ingredient, creating a significant challenge for emerging brands with limited research and development budgets. Additionally, the updated "healthy" claim rule, which takes effect in December 2024, introduces stricter limits on added sugar and sodium content. This has led to reformulation cycles that delay product launches and reduce first-mover advantages. Despite these challenges, brands that successfully meet these regulatory requirements can achieve credible differentiation in a market filled with vague wellness claims. The FDA's Generally Recognized as Safe (GRAS) notification database, which lists over 800 affirmed ingredients, serves as a valuable resource for formulators seeking pre-approved functional additives. However, novel botanicals and nootropics still require extensive safety documentation.

Other drivers and restraints analyzed in the detailed report include:

- Growing demand for plant-based and dairy-free RTD coffee formulations

- Flavor diversification and premiumization supporting consumer preference for unique taste experiences

- Shelf-life limitations and quality degradation of refrigerated RTD coffee products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Iced coffee accounted for 50.96% of type-based sales in 2025, emphasizing its established role as the preferred ready-to-drink (RTD) format for mainstream consumers who prioritize affordability and familiar taste profiles. On the other hand, cold brew coffee is projected to grow at an annual rate of 6.71% through 2031, surpassing the growth rate of iced coffee. This growth is driven by its lower acidity, smoother texture, and premium positioning, which appeal to a broader range of consumers.

The cold brew production process involves steeping coarsely ground coffee beans in cold water for 12 to 24 hours. This method extracts fewer bitter compounds and oxidized oils compared to hot-brewed iced coffee, resulting in a naturally sweeter flavor that requires less added sugar. This characteristic aligns with the preferences of health-conscious consumers and enables brands to market cold brew as a cleaner and more refined option. Starbucks' cold brew line, which includes nitro-infused variants, achieved over USD 1 billion in retail sales in 2024, showcasing the format's strong commercial potential.

PET bottles accounted for 35.82% of packaging-based sales in 2025 and are projected to grow at a rate of 6.50% through 2031. This growth is driven by their lightweight design, shatter resistance, and recyclability, and according to the American Chemistry Council, PET bottle recycling rates reached 29.1% in 2024, a slight increase from 27.9% in 2023, though still lower compared to glass and aluminum. In response to environmental concerns, brands are incorporating post-consumer recycled content. For example, Coca-Cola has committed to using 50% recycled PET (rPET) in its ready-to-drink (RTD) coffee bottles by 2027, while PepsiCo aims for 25% rPET by 2025.

Glass bottles, valued for their premium aesthetic and inert material properties, hold a smaller market share but command higher price points in specialty retail channels. Metal cans, particularly aluminum, are becoming more popular due to their superior recyclability and ability to preserve flavor by blocking light and oxygen. La Colombe's draft latte cans are a notable example of this trend. Aseptic packaging, including Tetra Pak cartons and flexible pouches, offers extended shelf life without refrigeration, enabling broader distribution to rural areas and international markets. Tetra Pak's six-layer laminate structure effectively protects against oxygen and light ingress, extending shelf life to 12 months while maintaining flavor integrity.

List of Companies Covered in this Report:

- Starbucks Corp.

- PepsiCo Inc.

- Danone S.A.

- Nestle S.A.

- The Coca-Cola Company

- Keurig Dr Pepper Inc.

- Califia Farms LLC

- La Colombe Coffee Roasters

- Luigi Lavazza S.p.A.

- J.M. Smucker Co.

- Chobani LLC

- High Brew Coffee Inc.

- Bulletproof 360 Inc.

- Chamberlain Coffee Inc.

- Stok

- International Delight

- Death Wish Coffee Co.

- BRC Inc.

- Costco Wholesale Corp.

- Peak Rock Capital LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising adoption of grab-and-go coffee culture among Gen Z and millennial consumers

- 4.2.2 Increasing health consciousness and demand for low-sugar and functional RTD coffee

- 4.2.3 Growing demand for plant-based and dairy-free RTD coffee formulations

- 4.2.4 Flavor diversification and premiumization supporting consumer preference for unique taste experiences

- 4.2.5 Robust e-commerce and online delivery channel growth enhancing product accessibility and convenience

- 4.2.6 Integration of functional ingredients such as adaptogens, nootropics, and plant-based proteins

- 4.3 Market Restraints

- 4.3.1 Stringent FDA regulations on functional beverage claims and health substantiation requirements

- 4.3.2 Shelf-life limitations and quality degradation of refrigerated RTD coffee products

- 4.3.3 Complex nutritional labeling and disclosure requirements limiting marketing flexibility and consumer appeal

- 4.3.4 Volatility and price fluctuations in coffee bean commodity markets

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Type

- 5.1.1 Cold Brew Coffee

- 5.1.2 Iced Coffee

- 5.1.3 Other RTD Coffee

- 5.2 By Packaging Type

- 5.2.1 PET Bottles

- 5.2.2 Glass Bottles

- 5.2.3 Metal Can

- 5.2.4 Aseptic packages (tetra pak, cartons, pouches)

- 5.2.5 Disposable Cups

- 5.3 By Functionality

- 5.3.1 Protein-Enriched

- 5.3.2 Energy-Infused

- 5.3.3 Other

- 5.4 By Distribution Channel

- 5.4.1 On-Trade

- 5.4.2 Off-Trade

- 5.4.2.1 Supermarket/Hypermarket

- 5.4.2.2 Convenience Stores

- 5.4.2.3 Specialty Stores

- 5.4.2.4 Online Retail

- 5.4.2.5 Other Distribution Channels

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Starbucks Corp.

- 6.4.2 PepsiCo Inc.

- 6.4.3 Danone S.A.

- 6.4.4 Nestle S.A.

- 6.4.5 The Coca-Cola Company

- 6.4.6 Keurig Dr Pepper Inc.

- 6.4.7 Califia Farms LLC

- 6.4.8 La Colombe Coffee Roasters

- 6.4.9 Luigi Lavazza S.p.A.

- 6.4.10 J.M. Smucker Co.

- 6.4.11 Chobani LLC

- 6.4.12 High Brew Coffee Inc.

- 6.4.13 Bulletproof 360 Inc.

- 6.4.14 Chamberlain Coffee Inc.

- 6.4.15 Stok

- 6.4.16 International Delight

- 6.4.17 Death Wish Coffee Co.

- 6.4.18 BRC Inc.

- 6.4.19 Costco Wholesale Corp.

- 6.4.20 Peak Rock Capital LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK