PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066428

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066428

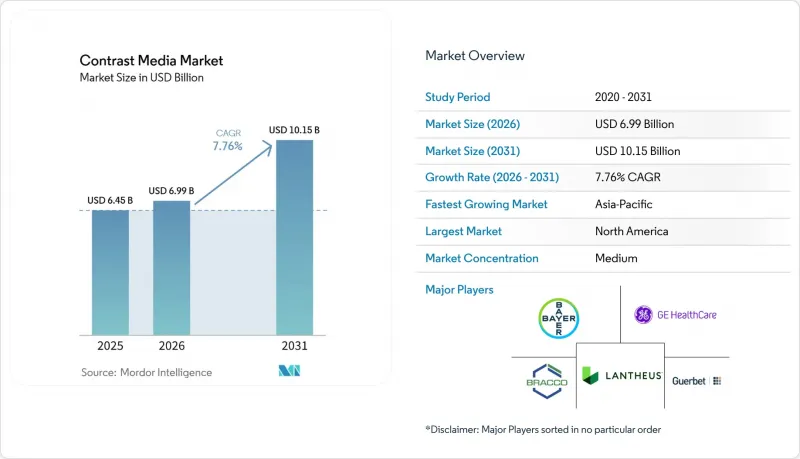

Contrast Media - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the contrast media market size is expected to grow from USD 6.45 billion in 2025 to USD 6.99 billion in 2026 and is forecast to reach USD 10.15 billion by 2031 at 7.76% CAGR over 2026-2031.

This report is Segmented by Product Type (Iodinated, Barium-Based, Gadolinium-Based, Microbubble & Emerging Agents), Modality (X-ray/CT, MRI, Ultrasound), Route of Administration (Intravascular, Oral, Rectal), Application (Cardiovascular, Oncology, and More), End User (Hospitals, Diagnostic Imaging Centers and More), and Geography (North America and More). Market Forecasts are Provided in Terms of Value (USD).

Global Contrast Media Market Trends and Insights

Rising Prevalence of Chronic Diseases Drives Imaging Demand

Global cancer incidence reached 20 million new cases in 2024, while cardiovascular disease caused 18.6 million deaths.Serial contrast-enhanced imaging is now embedded in oncology and cardiology guidelines, resulting in multiple scans per patient each year. Coronary CT angiography replaces invasive catheterization in 40% of stable angina cases, consuming 80-120 milliliters of iodinated agent per study. Populations in Japan and Germany each have more than one-fifth of citizens over age 65, which boosts procedure volumes. Even when per-scan volumes decline, total milliliter demand rises because the number of examinations grows faster than dose reductions.

Growing Global Diagnostic Imaging Procedure Volumes

Radiology departments performed 5.2 billion imaging examinations worldwide in 2024, up from 4.8 billion one year earlier. China extended reimbursement for contrast-enhanced ultrasound, opening access for 300 million rural residents, and India added 15,000 imaging centers through Ayushman Bharat by 2025. Medicare Advantage plans in the United States cover annual lung CT screening for 14 million high-risk smokers, while Gulf Cooperation Council nations increased contrast imports by 22% in 2024 to meet medical-tourism demand.

Gadolinium Deposition and Contrast-Induced Nephropathy Concerns

Autopsy findings published in 2024 revealed gadolinium deposits in brain tissue, prompting the FDA to demand label changes. Utilization of gadolinium-based agents fell 12% for non-critical cases. Iodinated agents trigger acute kidney injury in up to 5% of high-risk patients, leading to mandatory renal screening that delays or cancels 8% of procedures. European guidelines now recommend prophylactic hydration, adding USD 80-150 per case and discouraging borderline orders. U.S. malpractice insurers raised premiums for radiologists with above-average adverse events, further tightening use.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advances in High-Resolution CT and MRI Scanners

- Regulatory Approvals of Safer Low- or Iso-Osmolar Agents

- High Capital Cost of Advanced Imaging Equipment and Agents

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Iodinated agents represented 71.52% of the contrast media market in 2025, confirming their primacy across CT angiography, urography, and gastrointestinal studies. Non-ionic formulations command the segment because low osmolality limits injection discomfort and adverse reactions. Barium compounds remain useful in fluoroscopic esophageal and colon exams, yet their share erodes as CT colonography adoption rises. Gadolinium agents remain indispensable for brain and spine imaging, though deposition concerns suppress discretionary use. The fastest expansion belongs to microbubble and emerging agents, which post a 10.23% CAGR through 2031 as ultrasound gains favoritism in resource-constrained settings.

Microbubble agents thrive in point-of-care echocardiography, where portable ultrasound detects wall-motion abnormalities without radiation. Lantheus's Definity enjoyed broader adoption in 2024 when stress echocardiography started rivaling nuclear perfusion imaging in accuracy. Ionic iodinated products are being phased out in high-income nations but still cover 12% of demand in price-sensitive areas. Nanoparticle iron-oxide agents could reshape MRI economics by serving the 15 million renal-impaired patients currently left without safe options, although scale-up challenges persist.

X-ray and CT accounted for 58.35% of the contrast media market in 2025, grounded in an installed base of 70,000 CT scanners worldwide. MRI holds roughly 30% share, and ultrasound is growing at a 9.14% CAGR. Portable ultrasound devices now sell for less than USD 5,000, making contrast-enhanced ultrasound feasible in outpatient and rural clinics. Ultrasound's rise in hepatology parallels new guidelines that endorse it for liver lesion characterization, reducing costs and removing nephrotoxicity risk.

Cardiology benefits as stress echocardiography with microbubbles reaches 89% diagnostic accuracy for coronary disease. MRI growth faces safety questions but remains vital where soft-tissue contrast is critical. Fluoroscopic volumes shrink as cross-sectional imaging supersedes projection radiography. Vendors with portfolios spanning all three modalities are better insulated against shifts in use patterns, while single-modality suppliers experience margin pressure.

Geography Analysis

North America accounted for 38.66% of revenue in 2025, supported by the highest per-capita imaging rates and reimbursement policies that classify contrast as a pass-through expense. The United States alone conducts an average of 1.2 contrast-enhanced studies per resident each year, while Canada's single-payer system constrains usage through formulary limits. Mexico, though smaller, is rising as private insurance spreads and new hospitals open in major cities.

Asia-Pacific is set to post a 9.38% CAGR through 2031, reflecting large-scale government investments. China allocated USD 4.2 billion in 2024 to install CT and MRI in county hospitals, targeting 90% coverage by 2027. India's public scheme expanded reimbursements for CT angiography, unlocking a massive population base previously limited to invasive tests. Japan's mature market stays stable, but high per-capita consumption endures due to cultural preference for comprehensive checkups. Australia and South Korea embrace photon-counting CT and AI injectors, raising efficiency and keeping adoption at the forefront.

Europe shows mixed dynamics. Germany pairs high volumes with strict safety standards favoring macrocyclic gadolinium despite its price premium. France pushed through a 12% price cut for iodinated agents, squeezing supplier margins. The UK National Health Service restricts gadolinium to oncology and neurology, leading to 30% lower per-capita use than Germany. Italy and Spain broadened outpatient capacity by adding 140 centers in 2024. Middle East and Africa enjoy above-average growth as Gulf nations build medical-tourism hubs, while South America wrestles with affordability even as cancer-screening initiatives raise iodinated contrast volumes.

- Bayer

- Bracco Imaging S.p.A.

- Canon

- CMC Contrast AB

- Daiichi Sankyo

- Fujifilm Holdings Corp.

- GE Healthcare

- Guerbet Group

- Hengrui Medicine

- iMAX Diagnostic Imaging

- Koninklijke Philips

- Lantheus

- Nanopet Pharma GmbH

- Nemoto Kyorindo Co. Ltd.

- Siemens Healthineers

- Spago Nanomedical

- Taejoon Pharm

- Trivitron Healthcare

- Ulrich GmbH & Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Chronic Diseases (Cancer & CVD)

- 4.2.2 Growing Global Diagnostic Imaging Procedure Volumes

- 4.2.3 Technological Advances in High-Resolution CT & MRI Scanners

- 4.2.4 Regulatory Approvals of Safer Low-/Iso-Osmolar Agents

- 4.2.5 AI-Guided Injector Protocols Boosting Dose Optimization

- 4.2.6 Emergence of Renal-Safe Iron-Oxide Nanoparticle Agents

- 4.3 Market Restraints

- 4.3.1 Gadolinium Deposition & Contrast-Induced Nephropathy Concerns

- 4.3.2 High Capital Cost of Advanced Imaging Equipment & Agents

- 4.3.3 Iodine Feedstock Price Volatility & Supply Disruptions

- 4.3.4 Rise of Non-Contrast Imaging Modalities (Spectral CT, DL-Recon)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Iodinated Contrast Media

- 5.1.1.1 Ionic Iodinated

- 5.1.1.2 Non-ionic Iodinated

- 5.1.2 Barium-based Contrast Media

- 5.1.3 Gadolinium-based Contrast Media

- 5.1.4 Microbubble & Emerging Agents

- 5.1.1 Iodinated Contrast Media

- 5.2 By Modality

- 5.2.1 X-ray / CT

- 5.2.2 MRI

- 5.2.3 Ultrasound

- 5.3 By Route of Administration

- 5.3.1 Intravascular

- 5.3.2 Oral

- 5.3.3 Rectal

- 5.4 By Application / Indication

- 5.4.1 Cardiovascular Disorders

- 5.4.2 Oncology

- 5.4.3 Neurological Disorders

- 5.4.4 Gastrointestinal Disorders

- 5.4.5 Musculoskeletal Disorders

- 5.4.6 Nephrological Disorders

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Diagnostic Imaging Centers

- 5.5.3 Clinics & Ambulatory Surgery Centers

- 5.5.4 Research & Academic Institutes

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 France

- 5.6.2.3 United Kingdom

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Bayer AG

- 6.3.2 Bracco Imaging S.p.A.

- 6.3.3 Canon Medical Systems

- 6.3.4 CMC Contrast AB

- 6.3.5 Daiichi Sankyo Company

- 6.3.6 Fujifilm Holdings Corp.

- 6.3.7 GE Healthcare

- 6.3.8 Guerbet Group

- 6.3.9 Hengrui Medicine

- 6.3.10 iMAX Diagnostic Imaging

- 6.3.11 Koninklijke Philips N.V.

- 6.3.12 Lantheus Medical Imaging

- 6.3.13 Nanopet Pharma GmbH

- 6.3.14 Nemoto Kyorindo Co. Ltd.

- 6.3.15 Siemens Healthineers

- 6.3.16 Spago Nanomedical AB

- 6.3.17 Taejoon Pharm

- 6.3.18 Trivitron Healthcare

- 6.3.19 Ulrich GmbH & Co. KG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment