PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066441

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066441

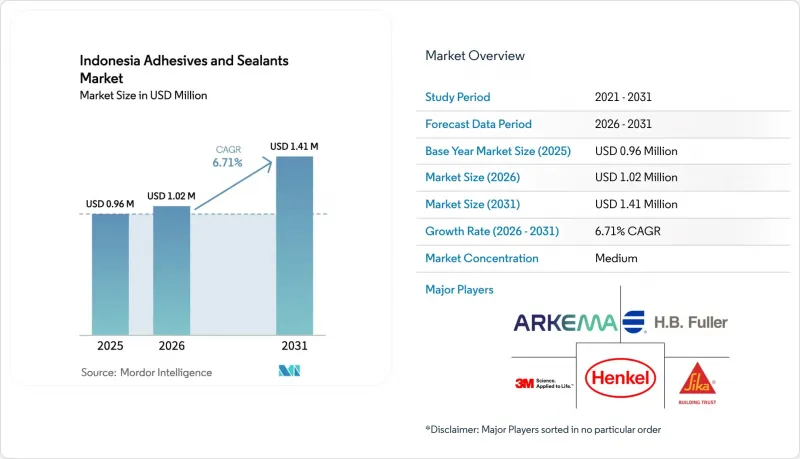

Indonesia Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the indonesia adhesives and Sealants Market size is projected to be USD 0.96 million in 2025, USD 1.02 million in 2026, and reach USD 1.41 million by 2031, growing at a CAGR of 6.71% from 2026 to 2031.

This report is Segmented by Adhesives by Resin (Acrylic, Cyanoacrylate, Epoxy, Polyurethane, Silicone, and More), Adhesives by Technology (Hot Melt, Reactive, Solvent-Borne, UV Cured, and More), Sealants by Resin (Polyurethane, Epoxy, and More), and End-User Industry (Aerospace, Automotive, Building and Construction, and More). The Market Forecasts are Provided in Terms of Value (USD).

Indonesia Adhesives And Sealants Market Trends and Insights

Robust Growth in Indonesia's FMCG Flexible-Packaging Sector

Flexible packaging output rose to 159.2 billion units in 2024, up from 141.3 billion in 2019, and brand-owner circularity pledges compel laminating and pressure-sensitive adhesive suppliers to guarantee food contact, recycling compatibility, and higher heat-resistance thresholds. Multinationals respond with rapid-cure hot melts optimized for automated case-forming lines, while smaller converters struggle to certify formulations under evolving EU and ASEAN regulations. The volume surge is therefore widening the technology gap and consolidating demand around suppliers that run regional pilot labs, food-contact testing, and digital traceability platforms.

Ongoing Mega-Infrastructure Projects Accelerating Construction Adhesives Demand

Government infrastructure approvals totaling CHF 25 billion (USD 27.84 billion) in 2023 and an overall construction wallet valued at CHF 240 billion (USD 272.69 billion) in 2024 continue to drive tile-adhesive, grout, and structural bonding demand at above-GDP rates. Revised SNI performance norms aligned with ISO 13007 now influence public tenders, shifting volume toward ISO-compliant brands that can guarantee long-term durability in humid coastal and seismic zones. Mega-bridges, new airports, and high-rise residential towers thus anchor a long-tail pull for mortar, sealant, and concrete-repair chemistries.

Volatility in Imported Petrochemical Feedstock Prices

Indonesia imports about 42% of polyethylene and 57% of polypropylene, so adhesive grade EVA, VAE, and SB latex prices move with naphtha and exchange fluctuations. Multinationals with captive resin plants hedge risk through multiyear offtake contracts, while small batch blenders rely on spot cargoes, amplifying cost swings. Upcoming domestic cracker expansions may ease shortages after 2027, but near-term exposure remains a working-capital constraint.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Domestic Footwear Manufacturing for Export Markets

- Rapid Adoption of Hot-Melt Technologies in E-Commerce Logistics Packaging Lines

- Fragmented Inter-Island Logistics Inflating Distribution Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Acrylic maintained a 29.00% share in 2025 of the Indonesia Adhesives and Sealants market. The market size for polyurethane products is projected to expand at a 7.02% CAGR as athletic-shoe exporters specify higher heat resistance and peel strength. Research on palm-oil-derived polyols and lignin-based non-isocyanate routes demonstrated 26.2 MPa shear strength, validating a future shift toward safer, renewable feedstocks.

Indonesia Adhesives and Sealants market gains from acrylic emulsions remain anchored in tapes, labels, and low-cost woodworking glues, but escalating EU VOC ceilings push converters toward water-borne PU grades. Epoxies, cyanoacrylates, and phenol-formaldehyde occupy niche positions in electronics, MRO, and plywood. The widening performance-price spectrum allows multinationals to segment portfolios across chemistry families, while local formulators focus on acrylic or animal-glue lines that require lower capital intensity.

Water-borne products held 38.4% share in 2025 and dominate furniture, footwear, and graphic-arts lamination lines. Hybrid polyurethane-acrylic dispersions improve early green strength, reducing press time. Indonesia Adhesives and Sealants market share for reactive hot-melt technology is set to climb at a CAGR of 6.97% during the forecast period (2026-2031) because e-commerce carton makers value instant green strength and high final bond without ovens.

Solvent-borne lines remain essential for specialty footwear requiring the highest peel, while UV-curable and anaerobic systems serve electronics and maintenance niches. Suppliers now run dual pilot lines, water-borne for training SME users in Central Java and moisture-cure hot melts for Jakarta logistics hubs, to demonstrate line-speed economics before buyers commit.

List of Companies Covered in this Report:

- 3M

- Alteco Chemical Pte Ltd.

- Arkema

- Avery Dennison Corporation.

- BASF

- Dextone Indonesia

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Hexcel Corporation

- Hilti Indonesia

- Huntsman International LLC

- Jowat SE

- MAPEI S.p.A.

- PT. Pamolite Adhesive Industry

- Pidilite Industries Ltd.

- Sika AG

- Soudal

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Robust growth in Indonesia's FMCG flexible-packaging sector

- 4.2.2 Ongoing mega-infrastructure projects accelerating construction adhesives demand

- 4.2.3 Expansion of domestic footwear manufacturing for export markets

- 4.2.4 Rapid adoption of hot-melt technologies in e-commerce logistics packaging lines

- 4.2.5 Emergence of local furniture SMEs upgrading to water-based systems for EU export compliance

- 4.3 Market Restraints

- 4.3.1 Volatility in imported petro-chemical feedstock prices

- 4.3.2 Persistent rupiah depreciation inflating raw-material costs

- 4.3.3 Fragmented inter-island logistics inflating distribution costs

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 Adhesives by Resin

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE / EVA

- 5.1.7 Other Resins

- 5.2 Adhesives by Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Solvent-borne

- 5.2.4 UV Cured

- 5.2.5 Water-borne

- 5.3 Sealants by Resin

- 5.3.1 Polyurethane

- 5.3.2 Epoxy

- 5.3.3 Acrylic

- 5.3.4 Silicone

- 5.3.5 Other Resins

- 5.4 By End-user Industry

- 5.4.1 Aerospace

- 5.4.2 Automotive

- 5.4.3 Building and Construction

- 5.4.4 Footwear and Leather

- 5.4.5 Healthcare

- 5.4.6 Packaging

- 5.4.7 Electronics and Appliances

- 5.4.8 Woodworking and Joinery

- 5.4.9 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Alteco Chemical Pte Ltd.

- 6.4.3 Arkema

- 6.4.4 Avery Dennison Corporation.

- 6.4.5 BASF

- 6.4.6 Dextone Indonesia

- 6.4.7 Dow

- 6.4.8 H.B. Fuller Company

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Hexcel Corporation

- 6.4.11 Hilti Indonesia

- 6.4.12 Huntsman International LLC

- 6.4.13 Jowat SE

- 6.4.14 MAPEI S.p.A.

- 6.4.15 PT. Pamolite Adhesive Industry

- 6.4.16 Pidilite Industries Ltd.

- 6.4.17 Sika AG

- 6.4.18 Soudal

7 Market Opportunities and Future Outlook

- 7.1 Innovation in bio-based, palm-oil-derivative adhesives

- 7.2 White-space and Unmet-need Assessment