PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066451

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066451

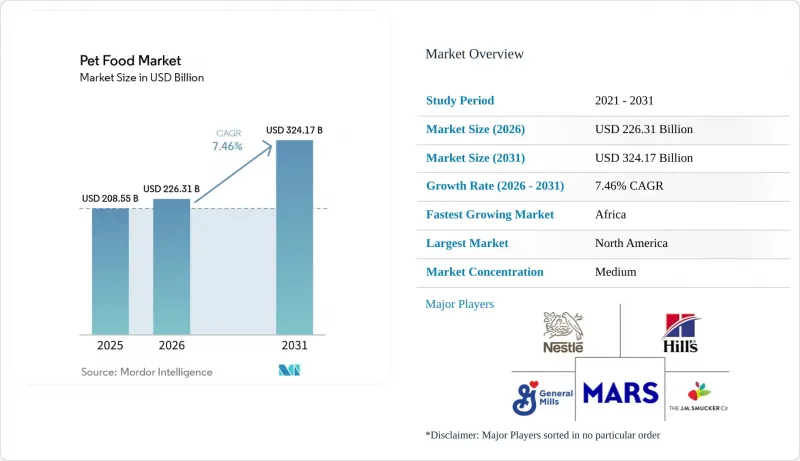

Pet Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the pet food market size is anticipated to increase from USD 208.55 billion in 2025 to USD 226.31 billion in 2026 and reach USD 324.17 billion by 2031, growing at a CAGR of 7.46% over 2026-2031.

This report is Segmented by Pet Food Product (Food, Pet Nutraceuticals/Supplements, and More), by Pets (Cats, Dogs, and Other Pets), by Distribution Channel (Convenience Stores, Online Channel, Specialty Stores, and More), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Global Pet Food Market Trends and Insights

Pet Humanization Sustaining Premium and Functional Nutrition Demand

Pet humanization remains a significant driver of demand in the pet food market across both mature and emerging regions. In mature markets, the trend has evolved beyond a shift from value to premium products, focusing instead on targeted nutrition with clearer ingredient and health positioning. General Mills reported in 2025 that the fresh pet food category was valued at USD 3 billion and projected to grow to USD 10 billion over the next decade, reflecting a shift in consumer spending toward products resembling household food choices. Similarly, Nestle S.A. stated in 2026 that cat nutrition was its strongest growth driver within PetCare, with wet cat food contributing to market-share gains in Europe and growth in the Americas. As pet owners increasingly scrutinize product labels and demand greater ingredient transparency, the pet food market is aligning with higher standards for sourcing, transparency, and product claims.

Veterinary Health Focus Lifting Therapeutic and Condition-Specific Diets

Veterinary nutrition is emerging as a significant growth driver in the pet food market, driven by increasing owner concerns about obesity, mobility, digestive health, and age-related issues in pets. Hill's Pet Nutrition expanded its offerings in this segment in January 2025 by introducing new and improved Prescription Diet and Science Diet products, utilizing ActivBiome+ platforms developed through over a decade of microbiome research. In April 2026, Hill's launched Prescription Diet Metabolic + j/d for cats, a product designed to support both weight management and mobility. According to the company, 88% of cats experienced weight loss within two months when fed Metabolic Nutrition alone. This product is notable for addressing two distinct needs, weight management and mobility, in a single formula, potentially improving compliance and increasing basket value. As clinical nutrition products gain wider commercial visibility beyond veterinary channels, the pet food market is attracting a broader base of consumers willing to invest in targeted nutritional solutions.

Raw Material and Packaging Cost Volatility Constraining Margins

Cost pressures remain a significant short-term constraint on profit growth in the pet food market. Freshpet reported in Q1 2026 that it was closely monitoring logistics, packaging, and input costs, highlighting increased fuel expenses and other cost-related impacts. Larger companies can address these challenges through pricing adjustments, formula modifications, and economies-of-scale leveraging. However, smaller manufacturers face limited options when costs rise rapidly. For instance, Purina's new Vargeao facility in Brazil incorporates automation and digital controls and operates entirely on renewable energy, showcasing how major companies are mitigating cost pressures through operational efficiencies. Despite such measures, fluctuations in raw material, packaging, and freight costs continue to hinder margin improvements across the pet food market.

Other drivers and restraints analyzed in the detailed report include:

- Online Auto-Ship and Omnichannel Access Widening Category Reach

- Novel-Protein Approvals Expanding Formulation Innovation

- Mycotoxin and Contamination Recall Exposure Increasing Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Food was the largest segment, and accounted 67.5% of the pet food market size in 2025, reflecting its role as the daily nutritional base for most companion animals. Wet food is gaining ground in this segment as companies add capacity to meet demand for more premium, palatable formats. Purina invested USD 470 million (BRL 2.5 billion) in its Vargeao wet pet food facility in Brazil in 2026, adding 30,000 metric tons of annual wet capacity and doubling the company's production capacity in the country. Mars, Incorporated also invested USD 72.7 million (AUD 112.5 million) in its Wodonga site in Australia to build a new wet-pouch facility, scheduled to open in June 2026. These moves show that companies still see strong value in staple food formats, but they are shifting that value toward wet, premium, and more specialized nutrition within the pet food industry.

Pet veterinary diets is the fastest-growing product segment, with a 8.7% CAGR for 2026-2031, supported by rising clinical needs and greater owner willingness to pay for targeted outcomes. Hill's Pet Nutrition expanded this space in 2025 with ActivBiome+ product upgrades and the Prescription Diet Metabolic + j/d launch for cats in 2026, which linked mobility and weight support in one formula. Fresh and minimally processed products are also changing the mix, with Freshpet reaching USD 1.10 billion in net sales in 2025 and Royal Canin and ORIJEN entering or expanding in fresh formats in 2025 and 2026 respectively. Pet treats and supplements remain important add-on categories, and the Food and Drug Administration (FDA) and Association of American Feed Control Officials (AAFCO) introduced new animal food ingredient review pathways during 2025 following the expiration of their longstanding memorandum of understanding, creating a more structured route for companies developing novel-protein and functional pet food ingredients.

Geography Analysis

North America was the largest region, with a 44.1% share of the pet food market in 2025, and it remains the center of premium spending and large-scale manufacturing investment. Purina started operations at its USD 550 million Batavia, Ohio, facility in March 2026, and the site is designed to feed 8 million animals annually. Mars, Incorporated opened its USD 450 million Royal Canin facility in Lewisburg, Ohio, in May 2025, and the company stated that it was part of more than USD 6 billion in investment in United States manufacturing over the past 5 years. Mexico is also gaining weight in the regional supply base, with Nestle committing USD 455 million to Mexican facilities through 2027, while South America continues to offer medium-term growth led by Brazil's lower commercial feeding penetration. Brazil remains the standout South American opportunity because only 45% of pets consume commercial food in 2025, leaving room for long-term conversion into the pet food market.

Europe remains a significant region in the pet food market, but growth is slower because the base is more mature and private-label capacity is already deep. The region still matters because it shapes ingredient rules and product quality expectations, and it continues to influence how novel proteins are reviewed and commercialized. Europe also remains active on consolidation and capability building, with The Nutriment Company completing 10 acquisitions in 2025 and Trouw Nutrition opening its second pet-dedicated premix plant in Europe, this time in Spain, in March 2026. The Asia-Pacific pet food market is expanding, supported by urbanization, first-generation pet ownership, and capacity investments such as Mars's USD 72.7 million (AUD 112.5 million) Wodonga expansion in Australia in 2026.

Africa was the fastest-growing region, with a CAGR of 8.1% for 2026-2031, although it is growing from a smaller base than North America or Europe. The main driver is low current penetration of commercial pet food, leaving room for long-term conversion as urban incomes and companion animal ownership rise. The Middle East also shows strong momentum, especially in Gulf Cooperation Council markets, where premium imported brands have a visible shelf presence and veterinary care is becoming more common in major cities. South Africa remains the most developed African market, and RCL FOODS agreed in March 2026 to acquire Martin & Martin for USD 36 million (ZAR 695 million) to expand beyond dry food and build a stronger position in wet food and pet care. Saudi Arabia, the United Arab Emirates, and Egypt are continuing to emerge as longer-term growth opportunities in the Middle East, supported by rising pet ownership, increasing demand for premium pet food, expanding modern retail distribution, and growing consumer awareness of specialized nutrition products.

- Purina PetCare (Nestle S.A.)

- Mars, Incorporated

- Hill's Pet Nutrition, Inc. (Colgate-Palmolive Company)

- General Mills, Inc.

- The J.M. Smucker Company

- Affinity Petcare S.A. (Agrolimen S.A.)

- Freshpet, Inc.

- i-Tail Corporation Public Company Limited (Thai Union Group Public Company Limited)

- VAFO Group a.s.

- heristo aktiengesellschaft

- United Petfood NV

- Unicharm Corporation

- Wellness Pet Company, Inc. (Clearlake Capital Group, L.P.)

- Diamond Pet Foods (Schell & Kampeter, Inc.)

- Sunshine Mills, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.1.1 Cats

- 4.1.2 Dogs

- 4.1.3 Other Pets

- 4.2 Pet Expenditure

- 4.3 Consumer Trends

5 SUPPLY AND PRODUCTION DYNAMICS

- 5.1 Trade Analysis

- 5.2 Ingredient Trends

- 5.3 Distribution Channel Analysis

- 5.4 Regulatory Framework

- 5.5 Market Drivers

- 5.5.1 Pet humanization sustaining premium and functional nutrition demand

- 5.5.2 Veterinary health focus lifting therapeutic and condition-specific diets

- 5.5.3 Online auto-ship and omnichannel access widening category reach

- 5.5.4 Fresh, minimally processed, and high-protein formats upgrading spending

- 5.5.5 AI-guided personalization and diagnostic-linked feeding programs

- 5.5.6 Novel-protein approvals expanding formulation innovation

- 5.6 Market Restraints

- 5.6.1 Raw material and packaging cost volatility constraining margins

- 5.6.2 Price-sensitive trade-down limiting premium basket expansion

- 5.6.3 Ultra-processed food scrutiny pressuring kibble-centric portfolios

- 5.6.4 Mycotoxin and contamination recall exposure increasing compliance costs

6 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 6.1 By Pet Food Product

- 6.1.1 Food

- 6.1.1.1 Dry Pet Food

- 6.1.1.1.1 Kibbles

- 6.1.1.1.2 Other Dry Pet Food

- 6.1.1.2 Wet Pet Food

- 6.1.1.1 Dry Pet Food

- 6.1.2 Pet Nutraceuticals/Supplements

- 6.1.2.1 Milk Bioactives

- 6.1.2.2 Omega-3 Fatty Acids

- 6.1.2.3 Probiotics

- 6.1.2.4 Proteins and Peptides

- 6.1.2.5 Vitamins and Minerals

- 6.1.2.6 Other Nutraceuticals

- 6.1.3 Pet Treats

- 6.1.3.1 Crunchy Treats

- 6.1.3.2 Dental Treats

- 6.1.3.3 Freeze-dried and Jerky Treats

- 6.1.3.4 Soft and Chewy Treats

- 6.1.3.5 Other Treats

- 6.1.4 Pet Veterinary Diets

- 6.1.4.1 Derma Diets

- 6.1.4.2 Diabetes

- 6.1.4.3 Digestive Sensitivity

- 6.1.4.4 Obesity Diets

- 6.1.4.5 Oral Care Diets

- 6.1.4.6 Renal

- 6.1.4.7 Urinary Tract Disease

- 6.1.4.8 Other Veterinary Diets

- 6.1.1 Food

- 6.2 By Pets

- 6.2.1 Cats

- 6.2.2 Dogs

- 6.2.3 Other Pets

- 6.3 By Distribution Channel

- 6.3.1 Convenience Stores

- 6.3.2 Online Channel

- 6.3.3 Specialty Stores

- 6.3.4 Supermarkets/Hypermarkets

- 6.3.5 Other Channels

- 6.4 By Region

- 6.4.1 North America

- 6.4.1.1 Canada

- 6.4.1.2 Mexico

- 6.4.1.3 United States

- 6.4.1.4 Rest of North America

- 6.4.2 South America

- 6.4.2.1 Argentina

- 6.4.2.2 Brazil

- 6.4.2.3 Rest of South America

- 6.4.3 Europe

- 6.4.3.1 France

- 6.4.3.2 Germany

- 6.4.3.3 Italy

- 6.4.3.4 Netherlands

- 6.4.3.5 Poland

- 6.4.3.6 Russia

- 6.4.3.7 Spain

- 6.4.3.8 United Kingdom

- 6.4.3.9 Rest of Europe

- 6.4.4 Asia-Pacific

- 6.4.4.1 Australia

- 6.4.4.2 China

- 6.4.4.3 India

- 6.4.4.4 Indonesia

- 6.4.4.5 Japan

- 6.4.4.6 Malaysia

- 6.4.4.7 Philippines

- 6.4.4.8 Taiwan

- 6.4.4.9 Thailand

- 6.4.4.10 Vietnam

- 6.4.4.11 Rest of Asia-Pacific

- 6.4.5 Middle East

- 6.4.5.1 Saudi Arabia

- 6.4.5.2 United Arab Emirates

- 6.4.5.3 Rest of Middle East

- 6.4.6 Africa

- 6.4.6.1 Egypt

- 6.4.6.2 South Africa

- 6.4.6.3 Rest of Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Key Strategic Moves

- 7.2 Market Share Analysis

- 7.3 Brand Positioning Matrix

- 7.4 Market Claim Analysis

- 7.5 Company Landscape

- 7.6 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments)

- 7.6.1 Purina PetCare (Nestle S.A.)

- 7.6.2 Mars, Incorporated

- 7.6.3 Hill's Pet Nutrition, Inc. (Colgate-Palmolive Company)

- 7.6.4 General Mills, Inc.

- 7.6.5 The J.M. Smucker Company

- 7.6.6 Affinity Petcare S.A. (Agrolimen S.A.)

- 7.6.7 Freshpet, Inc.

- 7.6.8 i-Tail Corporation Public Company Limited (Thai Union Group Public Company Limited)

- 7.6.9 VAFO Group a.s.

- 7.6.10 heristo aktiengesellschaft

- 7.6.11 United Petfood NV

- 7.6.12 Unicharm Corporation

- 7.6.13 Wellness Pet Company, Inc. (Clearlake Capital Group, L.P.)

- 7.6.14 Diamond Pet Foods (Schell & Kampeter, Inc.)

- 7.6.15 Sunshine Mills, Inc.

8 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS