PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066452

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066452

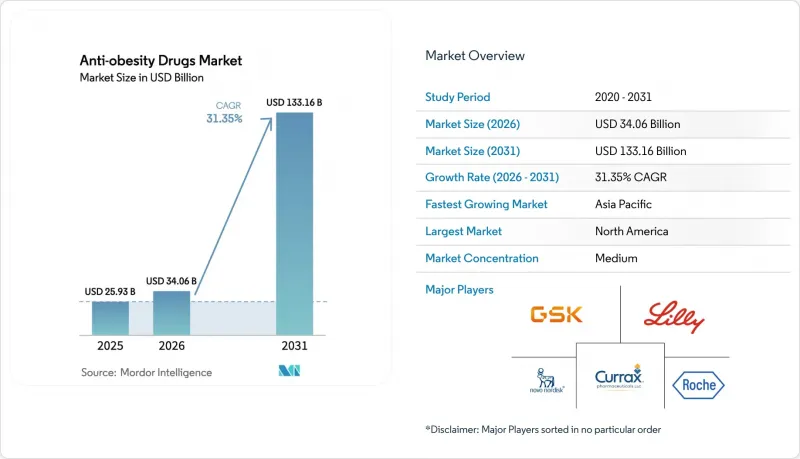

Anti-obesity Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the anti-obesity drugs market size is projected to be USD 25.93 billion in 2025, USD 34.06 billion in 2026, and reach USD 133.16 billion by 2031, growing at a CAGR of 31.35% from 2026 to 2031.

This report is Segmented by Mechanism of Action (Peripherally Acting Lipase Inhibitors, Centrally Acting Sympathomimetics, and More), Drug Type (Prescription Drugs and OTC Drugs), Route of Administration (Oral Daily Pills and Injectable), Distribution Channel (Hospital Pharmacies, and More), and Geography (North America, Europe, and More). The Market and Forecasts are Provided in Terms of Value (USD).

Global Anti-obesity Drugs Market Trends and Insights

Escalating Cardiometabolic Complications Driving Early Pharmacologic Intervention

Cardiologists and primary-care physicians now regard obesity as a cardiovascular risk factor comparable to smoking, following the American Heart Association's 2024 statement that reclassified the condition. Semaglutide's FLOW trial subsequently showed a 24% reduction in kidney-disease progression, prompting payers to waive prior authorizations for diabetic nephropathy cases. As 41.9% of U.S. adults were living with obesity in 2024, clinical guidelines began recommending GLP-1 initiation within six months of diagnosis rather than after lifestyle failure. Employer health plans quickly aligned benefit designs with these guidelines, fueling a surge in first-line prescriptions. This compressed treatment pathway is now mirrored in Europe and Japan, shrinking the time from diagnosis to pharmacologic therapy and expanding the eligible population at scale.

Rapid Employer Adoption of GLP-1 Coverage as a Hedge Against Long-Term Healthcare Costs

A 2024 Employee Benefit Research Institute analysis found that self-insured employers covering semaglutide or tirzepatide cut diabetes-related claims by 12% and cardiovascular hospitalizations by 9% within 18 months, offsetting annual drug costs in the USD 12,000-16,000 range. As a result, 44% of large U.S. employers added GLP-1s to formularies in 2024 versus 25% in 2023. Outcomes-based contracts that peg rebates to sustained weight loss or HbA1c reduction are spreading, shifting risk to manufacturers and motivating adherence programs. Digital coaching bundled with prescriptions improved 12-month persistence rates from 40% to 65%, demonstrating that integrated models can blunt overall cost growth. Parallel moves in Canada and Australia indicate that employers worldwide are replicating the value-based blueprint to manage chronic-disease liability.

Manufacturing-Capacity Bottlenecks for Complex Peptide APIs

Solid-phase peptide synthesis, HPLC purification, and lyophilization create long cycle times that cap throughput. Novo Nordisk's USD 6 billion capacity build announced in 2024 and Lilly's USD 5.3 billion Indiana plant will not reach full output until 2027, keeping supply constrained. Only eight FDA-approved facilities worldwide can produce GLP-1 peptides at scale, so any disruption, such as the 2024 fire at a Danish supplier, quickly triggers global shortages. The European Medicines Agency responded to recurring deficits by advising prescribers to prioritize cardiovascular patients, effectively rationing therapy. CDMO expansions are underway, but regulatory qualification for complex peptides averages 18-24 months, ensuring that tightness persists in the near term.

Other drivers and restraints analyzed in the detailed report include:

- Breakthrough Cardiovascular-Outcome Data Expanding Prescriber Comfort and Payer Mandates

- Next-Generation Oral Small-Molecule GLP-1s Unlocking Primary-Care and Emerging-Market Volume

- Escalating Payer Budget-Impact Controls and Step-Therapy Barriers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The segment generated USD 13.1 billion in 2025, when GLP-1 monotherapies held 38.55% share. Retatrutide's 24.2% weight-loss profile, disclosed in December 2024, underscores why triple-agonists are expected to expand at a 32.25% CAGR through 2031. Over the next five years, dual GIP/GLP-1 agents should migrate from second-line to first-line therapy as clinicians aim to avert tolerability limits seen with higher-dose GLP-1 monotherapy. The addition of glucagon-receptor activity promises incremental fat-mass reduction and metabolic flexibility, broadening appeal to endocrine, cardiology, and hepatology specialists. Meanwhile, centrally acting sympathomimetics and lipase inhibitors are sliding toward low-volume niches, constrained by modest efficacy and safety trade-offs.

Payers are signaling willingness to reimburse premium-priced multi-agonists if cardiovascular or renal benefits materialize, a possibility under investigation in ongoing SURMOUNT-5 and TRIUMPH-2 outcome studies. Given superior weight loss and comorbidity impact, analysts expect multi-agonists to exceed 45% of the anti-obesity drugs market by 2031. New entrants such as Amgen's MariTide and Viking Therapeutics' VK2735 target differentiated dosing intervals or improved GI tolerability to carve share. The escalation in mechanism complexity heightens manufacturing cost but also raises efficacy and, by extension, value-based price ceilings.

Prescription products represented 64.53% of the anti-obesity drugs market in 2025, and the cohort is on track for a 32.85% CAGR through 2031. Over-the-counter alternatives like orlistat delivered only 2-3% incremental weight loss in 2024 meta-analyses, reinforcing prescriber reliance on higher-efficacy options. Payer formularies absorb up to 90% of prescription costs for eligible patients, whereas OTC products are fully out-of-pocket, limiting their reach to affluent self-payers. FDA guidance in 2024 also tightened the path for Rx-to-OTC switches by requiring biomarkers for chronic-disease self-selection, effectively closing the door to consumerized GLP-1s.

Going forward, prescription status will likely remain the default for any agent demonstrating double-digit weight loss or cardiometabolic endpoints. Rhythm Pharmaceuticals' setmelanotide, gated by a REMS and genetic testing, signals how regulators may handle next-generation therapies with complex safety profiles. For OTC players, the viable economic niche is slimming down to adjunctive products such as fiber-based appetite suppressants, which do not threaten branded franchises.

Geography Analysis

North America dominated with 39.53% of the anti-obesity drugs market in 2025, buoyed by obesity prevalence surpassing 41% of adults and expanding Medicare Part D coverage that raised the eligible pool by 15 million beneficiaries. Still, payer cost pressures remain acute; the Institute for Clinical and Economic Review deemed current GLP-1 prices cost-effective only below USD 7,000 annually, prompting insurers to demand steep rebates. Canada lags the United States, as public plans in only three provinces reimburse obesity drugs, creating reliance on private pay or employer coverage. Mexico's market is limited by out-of-pocket spend, but Novo Nordisk's lower-dose semaglutide at 40% below U.S. pricing began expanding access in 2024. Overall, North American growth will hinge on balancing clinical demand with payer affordability thresholds.

Asia-Pacific is forecast to post a 35.21% CAGR through 2031, the fastest among all regions, aided by regulatory approvals in China, Japan, and India alongside rapid middle-class expansion. China's 180 million adults with obesity constitute a massive addressable population, though reimbursement is confined to tier-1 cities and private plans. Japan's six-month reimbursement cap mandates demonstrable 5% weight loss for continuation, incentivizing high-adherence regimens. In India, a generic tablet priced 60% below the branded injectable quickly captured share, signaling cost-sensitive adoption pathways. South Korea and Australia approved local or imported GLP-1s but apply stringent BMI thresholds for publicly funded access, tempering early uptake. Oral formulations and forthcoming biosimilars are essential to unlocking second- and third-tier city penetration across the region.

Europe controlled roughly 25% of the anti-obesity drugs market in 2025, yet reimbursement gatekeeping restrains volume growth. NICE restricts semaglutide to BMI >= 35 kg/m2, shrinking the eligible population by 60% relative to FDA criteria. Germany enforces a 12-month reimbursement cap, requiring self-pay thereafter, while France approves coverage only for diabetic obesity. Shortages prompted an EMA alert in March 2024, leading to rationing protocols prioritizing cardiovascular co-morbid patients. Middle East and Africa remain nascent but show pockets of private-pay demand in Gulf Cooperation Council states. Latin America is led by Brazil, where private insurance, covering 25% of residents, funds semaglutide, but public systems have not prioritized coverage. Overall regional variability highlights how health-technology assessments and budget constraints filter clinical enthusiasm into disparate adoption curves.

- Altimmune Inc.

- Amgen

- AstraZeneca

- Bayer

- Boehringer Ingelheim Intl. GmbH

- Eli Lilly and Company

- Roche

- GlaxoSmithKline

- Hanmi Pharm. Co., Ltd.

- Innovent Biologics Inc.

- Merck

- Novo Nordisk

- Pfizer

- Rhythm Pharmaceuticals, Inc.

- Structure Therapeutics Inc.

- Takeda Pharmaceuticals

- Teva Pharmaceutical Industries

- Viking Therapeutics Inc.

- Zealand Pharma

- Zydus Lifesciences Ltd.

- Currax Pharmaceuticals

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating cardiometabolic complications driving early pharmacologic intervention

- 4.2.2 Rapid employer adoption of GLP-1 coverage as a hedge against long-term healthcare costs

- 4.2.3 Breakthrough cardiovascular-outcome data expanding prescriber comfort and payer mandates

- 4.2.4 Next-generation oral small-molecule GLP-1s unlocking primary-care and emerging-market volume

- 4.2.5 Chronic kidney-disease risk-reduction labeling creating multi-specialty pull-through

- 4.2.6 AI-enabled drug-discovery platforms accelerating multi-agonist pipeline productivity

- 4.3 Market Restraints

- 4.3.1 Manufacturing-capacity bottlenecks for complex peptide APIs

- 4.3.2 Regulatory safety surveillance around rare ophthalmic adverse events

- 4.3.3 Escalating payer budget-impact controls and step-therapy barriers

- 4.3.4 Grey-market compounding eroding branded-drug economics

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Mechanism of Action

- 5.1.1 GLP-1 Receptor Agonists

- 5.1.2 Dual GIP/GLP-1 Agonists

- 5.1.3 Triple or Multi-Receptor Agonists

- 5.1.4 Centrally Acting Sympathomimetics

- 5.1.5 Peripherally Acting Lipase Inhibitors

- 5.2 By Drug Type

- 5.2.1 Prescription Drugs

- 5.2.2 OTC Drugs

- 5.3 By Route of Administration

- 5.3.1 Injectable (Weekly / Monthly)

- 5.3.2 Oral Daily Pills

- 5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 Online Pharmacies & Tele-health Platforms

- 5.4.4 Weight-Loss Clinics

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Altimmune Inc.

- 6.3.2 Amgen Inc.

- 6.3.3 AstraZeneca plc

- 6.3.4 Bayer AG

- 6.3.5 Boehringer Ingelheim Intl. GmbH

- 6.3.6 Eli Lilly and Company

- 6.3.7 F. Hoffmann-La Roche AG

- 6.3.8 GSK plc

- 6.3.9 Hanmi Pharm. Co., Ltd.

- 6.3.10 Innovent Biologics Inc.

- 6.3.11 Merck & Co., Inc.

- 6.3.12 Novo Nordisk A/S

- 6.3.13 Pfizer Inc.

- 6.3.14 Rhythm Pharmaceuticals, Inc.

- 6.3.15 Structure Therapeutics Inc.

- 6.3.16 Takeda Pharmaceutical Co. Ltd

- 6.3.17 Teva Pharmaceutical Industries Ltd.

- 6.3.18 Viking Therapeutics Inc.

- 6.3.19 Zealand Pharma A/S

- 6.3.20 Zydus Lifesciences Ltd.

- 6.3.21 Currax Pharmaceuticals LLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment